EUR/JPY Violates 61.8% Fibonacci Level – What’s next!

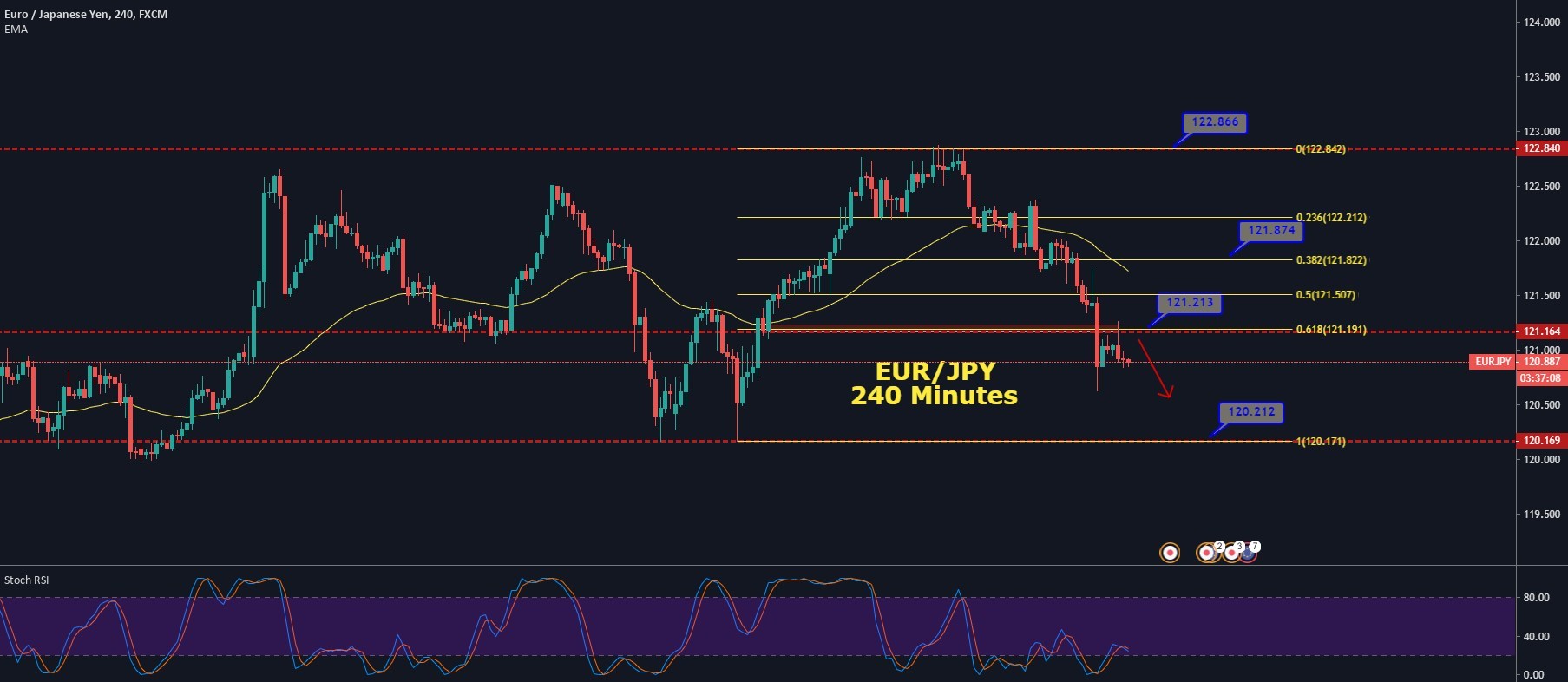

The EUR/JPY has not only completed 61.8% Fibonacci retracement at 121.191 but has also crossed below this level to trade at 120.887. The Japanese yen recently benefited from the market's risk-off sentiment in the wake of fears arising from China and trade headlines.

The market's risk tone was shaken by the news that the SARS team has returned to fight coronavirus also, whereas the World Health Organization (WHO) still needed some time to understand the cause behind the coronavirus. So it declared that the virus was not an international threat due to China's successful & strict measures to contain that virus spread.

However, there have been 17 deaths so far due to the same virus in China, and the number of people affected by it has been increasing day by day due to its contagious nature.

WHO declared that the virus was not an international threat due to China's successful & strict measures to contain that virus spread. Therefore, the World Health Organization (WHO) believed that it would be too early to term it as an international threat. As a result, the investors are moving their funds into the safe-haven assets like Japanese yen, driving the EUR/JPY down.

Technically, the EUR/JPY pair is holding in a bearish zone at 120.887, and closing of bearishly dominated candles are suggesting odds of selling trend in the pair. On the lower side, the EUR/JPY's immediate next support prevails at 120.450.

| Support | Pivot Point | Resistance |

| 121.64 | 121.83 | 122.04 |

| 121.43 | 122.23 | |

| 121.02 | 122.63 |

EUR/JPY - Trade Setup

Sell Below 120.950

Take Profit 120.450

Stop Loss 121.250

Author

EagleFX Team

EagleFX

EagleFX Team is an international group of market analysts with skills in fundamental and technical analysis, applying several methods to assess the state and likelihood of price movements on Forex, Commodities, Indices, Metals and