Equities forge ahead on Friday despite Ukraine, while Treasuries and the dollar return to status quo

- Markets remain volatile after recovery from the Ukrainian shock.

- Oil prices, Treasury rates and currencies return to pre-invasion levels.

- Federal Reserve Chair Jerome Powell testifies twice in Congress next week.

- Nonfarm Payrolls on Friday could return focus to the US economy.

Stocks had one of their best two-day runs on record, finishing a volatile week that turned on Russia’s invasion of Ukraine.

Bond traders were content to reverse Thursday’s early losses, leaving Treasury yields largely unchanged while the dollar gave up most of its risk-aversion gains and oil returned to pre-invasion pricing.

Federal Reserve Chair Jerome Powell will testify in Congress on Wednesday and Thursday, and markets will potentially rise and fall by what he says regarding the impact of the Russian-Ukrainian conflict on Fed policy.

Markets

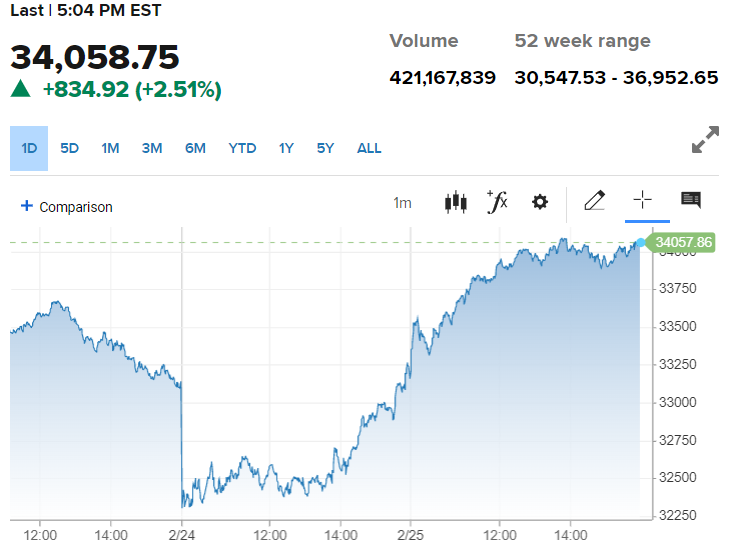

The S&P 500 rose 2.2% on Friday, 95.95 points closing at 4,384.65. It is down 8% for the year. The Nasdaq Composite added 221.04 points, 1.6% to 13,694.62, leaving this tech heavy average off 12.5% for the year. The Dow Jones Industrial Average climbed 834.92 points, 2.5%, concluding at 34,058.75. The Dow scored its best day since November 2020, improving its 2022 performance to -6.3%.

Dow

CNBC

Treasury yields were largely unchanged on Friday with the commercial benchmark 10-yield at 1.97% and the 30-year off less than a point from Thursday’s close at 2.285%. The 2-year return rose 2.4 basis points to 1.57%. At one time during Thursday’s reaction the 10-year yield was down 13 basis points, the 30-year was off 11 points and the 2-year had slipped 14 points.

10-year Treasury yield

CNBC

West Texas Intermediate (WTI) fell 1.1% on Friday closing at $91.80, essentially at par with its open on Thursday before the Ukraine attack at $91.92.

-637814330809511156.png)

The US dollar ended the week stronger in all the major pairs except the USD/CAD where it lost 40 points to 1.2700. Thursday’s sharp risk-aversion gains in all pairs were largely lost in Friday action with the USD/JPY retaining the largest edge.

-637814331557165122.png)

The week ahead

Ukraine will remain the flash point but with the initial shock worn off, markets will likely heed any reports of potential negotiations as confirmation that a conclusion is possible at whatever remove. Actual peace talks, or consultation and mediation aimed at negotiation, will restore market equanimity since once a cease fire is begun, a resumption of hostilities will be seen as unlikely.

The US and its European allies have said they will not target the Russian oil industry with sanctions, nonetheless, crude prices will remain the sensitive barometer for risk.

Fed Chair Jerome Powell, who testifies in the House on Wednesday and the Senate on Thursday, will be the spokesman for the world’s central banks. Given the comments of several regional Fed presidents on Thursday, all expressing confidence that the bank will be able to execute its rate policy, markets can expect the same opinion from Mr. Powell, with the necessary caveats for unexpected developments in Ukraine.

The US employment report for February on Friday should provide evidence that hiring continues apace. However, markets and the Fed are worried about inflation. With the Personal Consumption Expenditure Price Index rising to a new record at 6.1% in January, far ahead of its 5.5% forecast and December’s 5.8% score, and the core rate at 5.2%, a strong NFP report, especially with rising wages, will add to the pressure on the Fed governors to hike rates 0.5% on March 16.

.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.