Emerging market central banks approaching a pivot

Summary

Central banks in the emerging markets were first to tighten monetary policy; however, with inflation set to recede this year and local recessions forming, we believe developing economy central banks will also be first to initiate monetary easing cycles. But, not all central banks in the emerging markets are equal, and some institutions have accumulated more policy space to begin lowering interest rates. This report examines monetary policy space in the emerging markets and which central banks are likely to ease policy, and by what magnitude, before the end of this year. And while we believe easier monetary policy will be a trend across the developing world this year, we believe central banks will act prudently and emerging market currencies can not only absorb rate cuts, but outperform over the course of this year.

Rate cuts on the horizon in the emerging markets

Central bank activity has been the primary driver of economic trends and global financial markets over the last few years. At the start of the pandemic, central banks eased monetary policy forcefully to support activity and prevent long-lasting economic downturns. Low interest rates—coupled with loose fiscal policy and the global re-opening—resulted in a financial market rally, but also an inflation surge around the world reminiscent of the early 1980s. In response to that elevated inflation, central banks subsequently embarked on some of the most aggressive tightening cycles of the last few decades. These tightening cycles were present across the G10 and emerging markets, and included sharp interest rate hikes as well as reducing balance sheet holdings, most notably from the Federal Reserve. While G10 central bank tightening induced a global economic slowdown and financial market selloffs, central banks in the emerging markets were the first institutions to act and defend their respective economies against rising inflationary pressures. Not only did policymakers across the emerging markets act earlier, they raised interest rates at a much more aggressive pace than peer policymakers in the developed world (Figure 1). This was true for central banks across Latin America, most of EMEA (except for the South African Reserve Bank), with only institutions in emerging Asia—such as the Reserve Bank of India (RBI)—taking a more gradual approach to raising interest rates, while the People's Bank of China eased monetary policy.

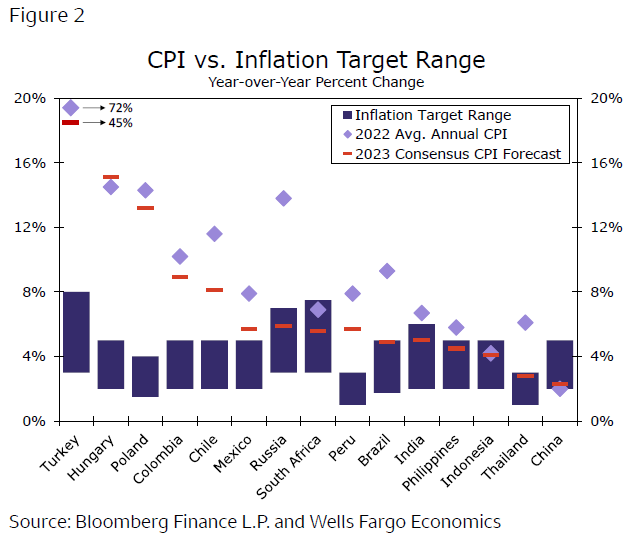

However, tighter monetary policy and the impact of high inflation are taking a toll on activity around the world. In our view, this combination should lead to a synchronized global economic downturn over the course of 2023, a forecast we have had in place since the middle of last year and have not been shy about sharing. As these recessions start to crystallize, or in some cases deepen, we believe central banks around the world will pivot on monetary policy. To that point, in select countries where recessions could be the most acute, central banks are likely to unwind interest rate hikes and begin easing monetary policy by the end of this year. In the G10, we believe central banks such as the Bank of England and Bank of Canada will cut interest rates in Q4-2023, and while we do not forecast easier Fed monetary policy this year, financial markets are priced for policy rates cuts in the United States before the end of 2023. But, similar to how emerging market policymakers acted ahead of the Fed and major central banks to raise interest rates, we believe central banks in the emerging markets will move ahead of the Fed and G10 counterparts to lower interest rates. This space to lower interest rates primarily comes from the idea that inflation will recede across the EM complex, and enter or approach central bank target ranges in 2023 (Figure 2). In order to do a more thorough assessment of whether emerging market policymakers indeed have room to start lowering interest rates, we updated—and modified—our monetary policy space framework we previously developed.

Author

Wells Fargo Research Team

Wells Fargo