Egypt: Deepening of external imbalances

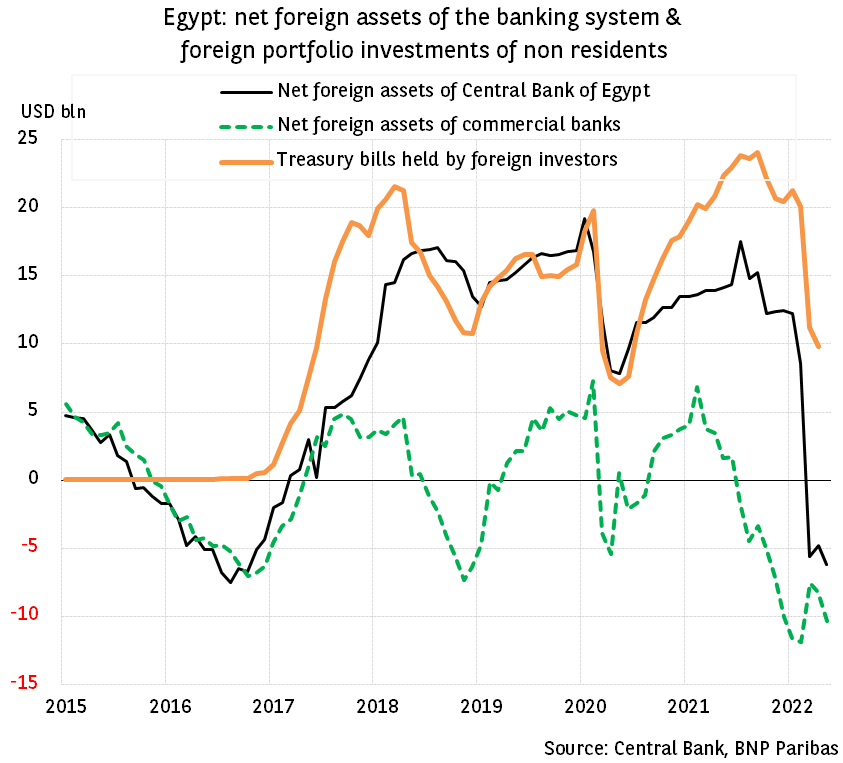

Currency liquidity in Egypt continues to deteriorate at a rapid pace. The banking sector’s net foreign assets (commercial banks and the central bank) are deeply negative (USD -16.6 billion in May 2022) and significantly exceed the lowest level reached during the 2016 crisis (USD -13.8 billion in October 2016). This deterioration comes as no surprise and the effects of the war in Ukraine on commodity prices have only exacerbated a pre-existing trend. Given a large recurring current account deficit (at least USD 20 billion this year) and significant external debt repayments (around USD 9 billion over a whole year), the Egyptian economy relies heavily on volatile portfolio investments.

Since the third quarter of 2021, foreign investors have become more averse to Egyptian risk owing to the deterioration of the current account. It has resulted in a sharp rise in the cost of foreign currency debt and a fall in foreign investment in the local debt market. The start of the conflict in Ukraine has sharply increased the price of certain commodities (such as grain) of which Egypt is a major importer and has riggered a sell-off from foreign investors.

Against this backdrop, the financial support from Gulf countries in the form of deposits with the central bank (USD 5 billion from Saudi Arabia) and the investment in local companies (USD 1.8 billion from an Abu Dhabi sovereign fund), as well as the depreciation of the Egyptian pound by around 15% last March have not stopped the deterioration of external liquidity. While the situation remains sustainable in the short term (the central bank’s gross foreign exchange reserves remain equivalent to around five months of goods and services imports), further external support is essential to avoid uncontrolled depreciation of the pound. Negotiations are currently under way with the IMF for a new financing programme (as the country did in 2016 and 2020). Gulf countries have committed to renewing their support, but in the form of direct or portfolio investments, and the timing of which remains to be confirmed.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.