Economic growth and inflation remain in a slowing trend

The Good:

- The S&P 500, Nasdaq, and Dow Jones Industrial averages have not broken below key moving averages or support levels.

- Several sectors remain in positive trends.

- Retail sales and inflation surprised to the positive last week.

The Bad:

- Economic growth and inflation remain in a slowing trend.

- The Dollar remains in a positive trend.

- Market sentiment is negative, as the risk-free asset is outperforming both international and domestic equities as well as high yield bonds in a majority of time frames.

The Ugly:

- The 4-week moving average of the ECRI WLI is negative -1.5% year-over-year.

- High yield is collapsing against Treasuries.

- Defensive factors and sectors are leading the market.

- The U.S. 10-year yield dropped 19 basis points and suggest slower growth.

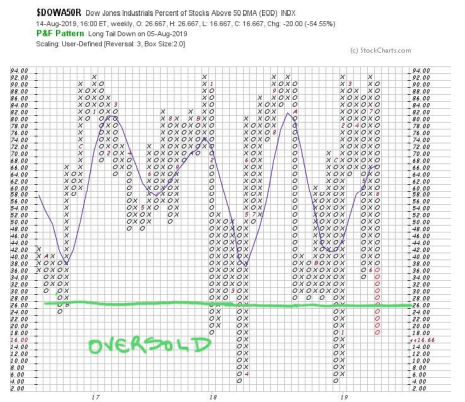

Market internals suggest that U.S. equity markets are oversold in the short-term. Long-term measures of market internals are not oversold however. Interestingly, most defensive assets are short-term overbought. The Fed is meeting in Jackson Hole this week, so we could see some volatility around this major event given that it probably wouldn’t require much fuel to ignite a short-covering rally. In this type of environment we recommend sticking to high quality, cash-flow producing assets, as well as diversification strategies for risk mitigation.

Economic Activity

- The ECRI Weekly leading index declined -1.6 from the prior week.

- Inflation came in at 1.8% year-over-year. This was up from 1.6% previous.

- Retail sales surprised to the upside, gaining 0.7% month-over-month. Expectations were for a 0.3% increase.

- Industrial production came in at 0.5% year-over-year. This is down from 1.1% previous.

Equity Markets

- Equities markets were down for the week again. The S&P 500 (IVV) dropped. -0.95%. The Total World Stock Market ETF (VT) dropped -1.02%.

- Transports were the clear laggards last week (IYT). This segment of the broad equities market fell -2.21%.

- The low volatility factor was the top performer, finishing the week flat.

- Consumer staples were the top sector, gaining over 1.50%.

Intermarket

- Lumber gained 2.98% against Gold last week.

- Stocks lost over -2% against both bonds and gold. (VT/IEF and VT/GLD)

- High yield bonds dropped over -4% against long-term Treasuries (JNK/TLT)

Fixed Income, Commodities, Currencies

- Long-term Treasuries were up over 4% last week.

- The U.S. 10-year Treasury note yield dropped another 19 basis points.

- Precious metals led other commodity segments, gaining over 1%.

- Copper was up on the week, despite the fall in equity markets.

- The U.S. Dollar gained 0.70% for the week.

- The Australian Dollar finally rebounded against the Japanese Yen.

Chart of the Week: Short-term market internals are oversold

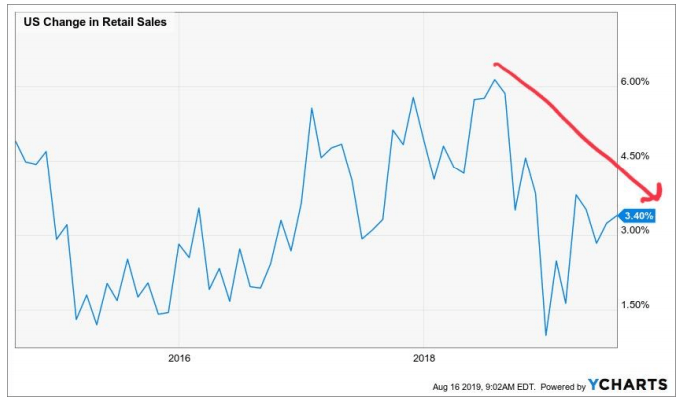

Chart 2: US Change in Retail Sales

Retail sales came in better than expected, rising 0.7% month-over-month. However, on a year-over-year basis, we can still see a slowing trend.

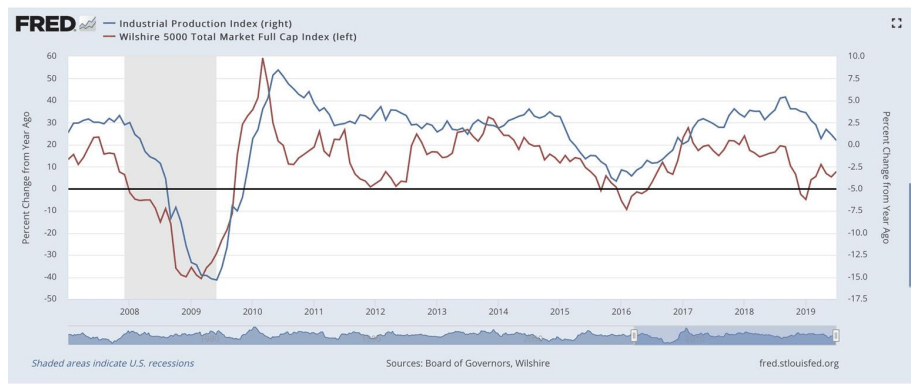

Chart 3: Industrial production (blue) dropped to 0.5% year-over-year

This indicator of broad economic growth is close to contracting for the first time since 2015. Industrial production has demonstrated a strong correlation with equity market growth in the past (red).

Author

Clint Sorenson, CFA, CMT

WealthShield