Economic data under the microscope, but surveys may be skewed by pol

Markets

U.S. stocks took a hiatus from record highs as the financial markets hit the pause button ahead of Friday’s big inflation data drop. The initial euphoria from the Fed’s jumbo rate cut is fading, and all eyes are now on the economy, with every macro tidbit under a microscope. Investors are weighing whether the Fed's move is enough to keep things humming.

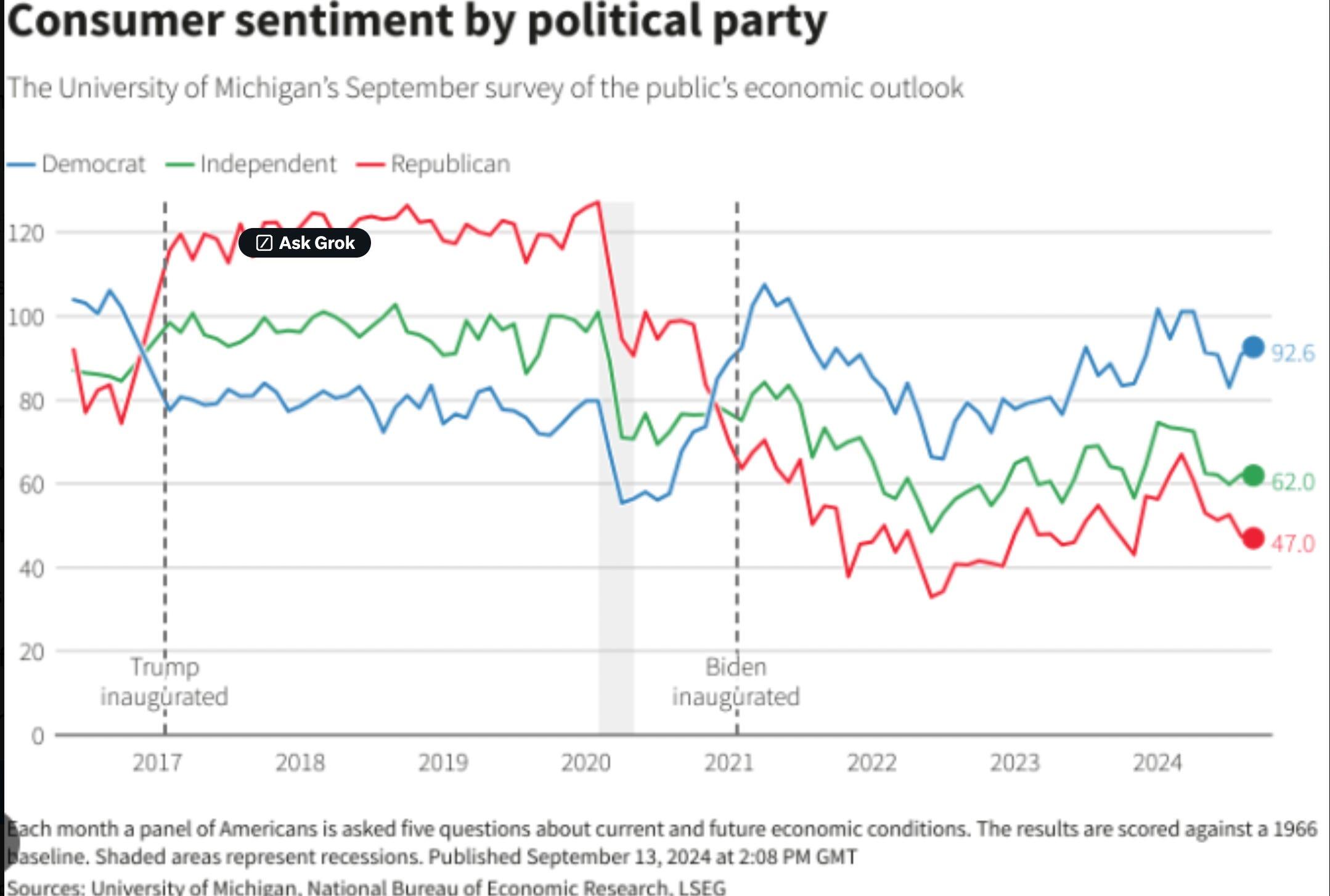

Ironically, Treasury yields ticked up after sinking on a surprisingly weak U.S. consumer confidence report the day before. The worst drop in three years stirred up fresh fears about the U.S. economy’s resilience. The big talk is about the “jobs plentiful” vs. “jobs hard to get” gauge, which slid to lows not seen since early 2017. This kind of data has people questioning the economy's strength, but the markets are always ready to flip the narrative. As yields rose, the U.S. dollar regained some ground, especially against the yen, with the Bank of Japan showing no urgency to hike rates.

Here’s the twist: in an election year, surveys like this tend to get coloured by political bias. Think about it—it’s in the opposition’s interest to make the economy look like a train wreck while those in power want to paint a rosy picture.

So, how much should we trust these numbers? Especially when they don’t align with what the hard macro data is telling us. After the Fed’s aggressive cuts and a clearer path to lower rates, economists have been revising U.S. consumer spending and upward GDP growth forecasts. Retail sales data looks solid, which could keep the economic engine running, even if the labour market cools off a bit. The recession signals baked into the confidence data might just be overblown.

With Friday’s key inflation reading around the corner, the market is leaning toward a cooler, sub-trend print. But here’s the nagging question: is there enough slack in the economy for inflation to slide down to the Fed’s 2.0% target, or will this growth surge send inflation spiralling back into the spotlight? The Fed has thrown the economy a lifeline, but we’ll see if it comes with some inflationary baggage down the road.

In short, after 36 hours of digesting the confidence data, maybe the takeaway is this: take all household surveys with a grain of salt, especially this close to an election. Stick to the hard data. After all, this isn’t the first time soft surveys have painted a doom-and-gloom picture, only for the real economic numbers to tell a completely different story. The economy’s not as bad as the surveys might suggest.

Of course, a strong economy is the real litmus test for stock market valuations, but there’s a balancing act going on. Markets are pricing in way more rate cuts than the Fed’s hinting at, and that could be where the risk lies—stocks riding high on extreme rate-cut fever.

Oil markets

Meanwhile, oil prices are cooling off as traders question China’s demand. The debate between OPEC and the IEA is heating up, with OPEC betting that China will need way more oil than the IEA thinks. But there’s natural skepticism about whether the PBoC's magic wand can cure China’s housing market funk. History tells us housing downturns take years, if not decades, to bounce back.

And let’s not forget that OPEC’s problem might be structural, too. In July, for the first time, sales of electric and hybrid vehicles in China overtook those of internal combustion engines, and more industrial trucks are running on LNG rather than diesel. These shifts in China’s energy consumption are a big deal for the oil market—pumping the brakes on demand.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.