ECB will cut rates in June and probably the BoE, too

Outlook

Initial jobless claims rose 22,000 to 231,000 in the latest week, more than 215,000 forecast. Yesterday we wrote “ho hum” because a weekly number and jobless claims hardly ever move the market, but this time the anti-dollar gang was waiting in the bushes to jump on it.

A hot tailwind was San Francisco Fed Daly: "We've had three stubborn months of data, but I still see monetary policy is working ... I do think that we're seeing, in a really positive way, disinflation."

We dismissed the claims-inspired move as ridiculous wishful thinking but could end up eating crow by the end of the day. In reality, we won’t know if this tiny number means labor market softening until we get CPI and retail sales next week. We say tiny because the workforce is 161.99 million persons, making 22,000 new claims less than 1% of 1%.

Something else ridiculous—the UK economy getting “the fastest growth in three years!” ING calls it a “surge.” For heaven’s sake, it was 1.4% three years ago and now it’s 0.6%. Talk about inflating the meaning of data.

Today the interesting news will be the minutes of the last ECB policy meeting. Expectations are still running high that the ECB will cut rates in June and probably the BoE, too.

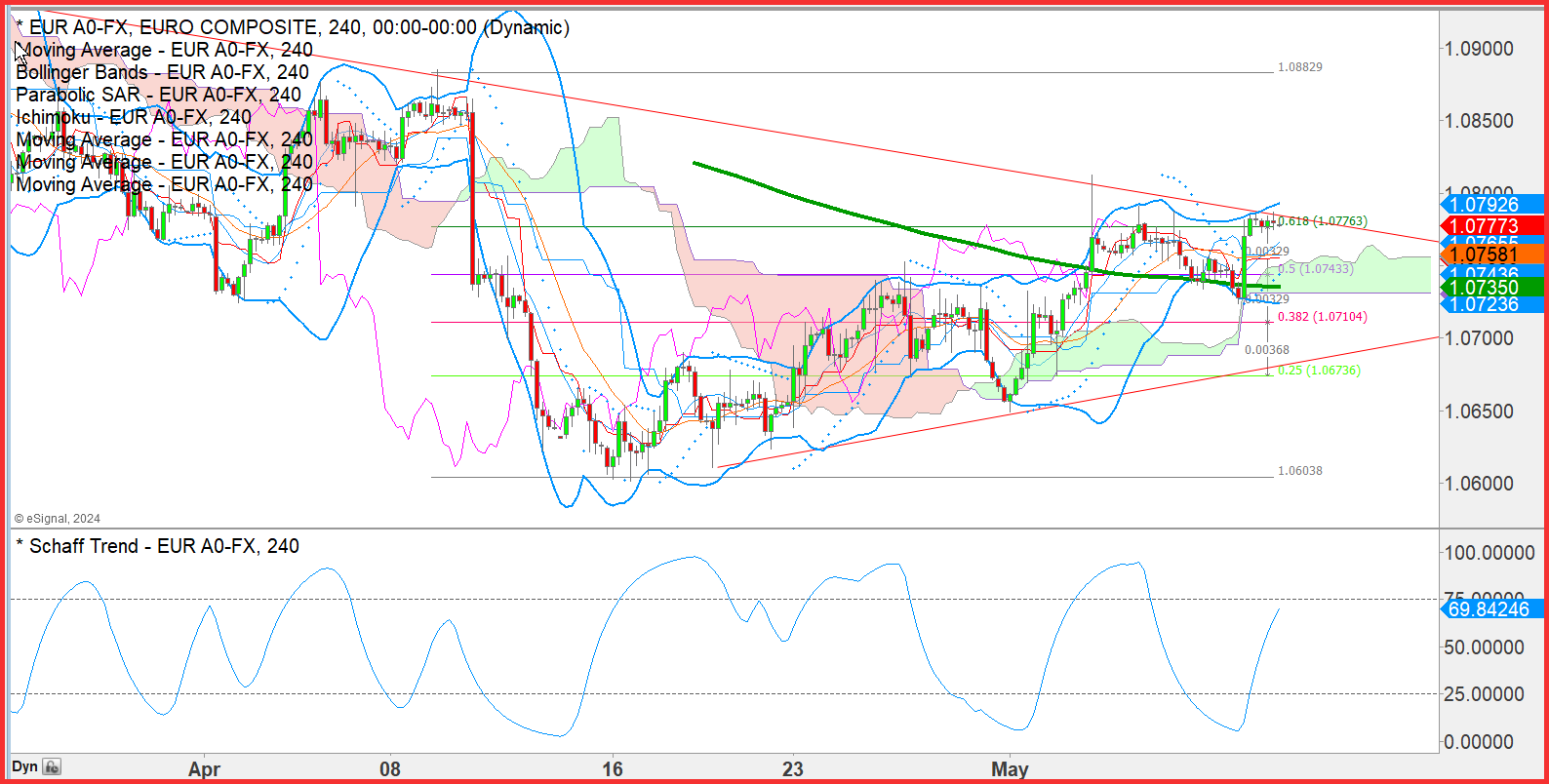

Forecast: The pullback hit a brick wall in the form of jobless claims. So far today the euro is not demonstrating much progress and has not gotten to the previous high at 1.0806 from May 13. On the 240-minutes chart, however, the euro has reached and surpassed the 62% retracement off the April 15 low, and we always expect a retreat when that level is hit. We therefore fear that the euro upward move will not stall, as it “should” if we were considering expected central bank conduct.

Intervention saga

Later yesterday Bloomberg used the Fed data to justify the charge on intervention. “Central banks’ holdings of US securities fell by about $10.6 billion, leaving total holdings at $2.95 trillion, data as of May 8 show. Meanwhile, monetary officials stashed $362 billion at the Fed’s reverse repurchase agreement facility, up from $360 billion a week earlier, according to the latest data from the central bank.

“The figures showing the cash drain cover a week that included at least another instance where Japanese policymakers likely intervened in foreign-exchange markets to support the yen, which is the weakest Group-of-10 currency this year versus a broadly strengthening dollar.”

“Last week, data from the prior reporting period showed a $17.8 billion drop in balances in a separate cash account used by central bankers, suggesting these funds may have been tapped to prop up the currency at some point.

“However, historically, Japanese authorities haven’t stockpiled their intervention resources at the Fed’s non-interest-bearing foreign official deposits category, according to Wrightson ICAP. That points to the possibility that the latest drop in foreign central bank Treasury holdings may have also been used in efforts to support the yen.”

Let’s note that these accounts are for all central banks with accounts at the Fed, not just the Bank of Japan. So, another Big Stretch. The last time we looked at these accounts was when the Fed lent to Europeans during the banking crisis in 2008-09.

Tidbit: Bloomberg and Reuters report that we could get a new China trade policy as early as next Tuesday. It would apply higher tariffs on strategic things like EV cars, solar and batteries. This is in contrast to Trump, who wants a 60% tariff on everything from China but would not target anything “green” like the current administration. Articles about the disastrous Trump policy proposals are appearing not only in the mainstream press but also academic journals and essays from self-appointed policy wonks like Brookings.

Tidbit 2: A front-page story in the FT is about carmakers shifting emphasis to hybrids from all-EV. Funny, this story was all over the press and American TV two or three weeks ago in the US.

Reasons for the Fed to cut rates

Avoid embarrassment from getting inflation wrong twice.

Normalize the yield curve.

Head off any recessionary tendencies.

Help housing via mortgage rates.

Help banks rollover commercial property loans.

Help the stock market.

Synchronize with the ECB (and Riksbank and SNB).

(Help the current White House).

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat