Dovish UK jobs report bolsters case for further rate cuts

UK private sector wage growth is falling and is likely to continue on this path for the rest of this year. A December rate cut is possible, though for now we’re forecasting February for the next move.

At a time when the Bank of England is poised to slow the pace of interest rate cuts, the latest UK jobs report suggests its work is not done yet. That’s because private sector wage growth – something that’s long proven to be a thorn in the Bank’s side – is finally showing signs of falling more rapidly.

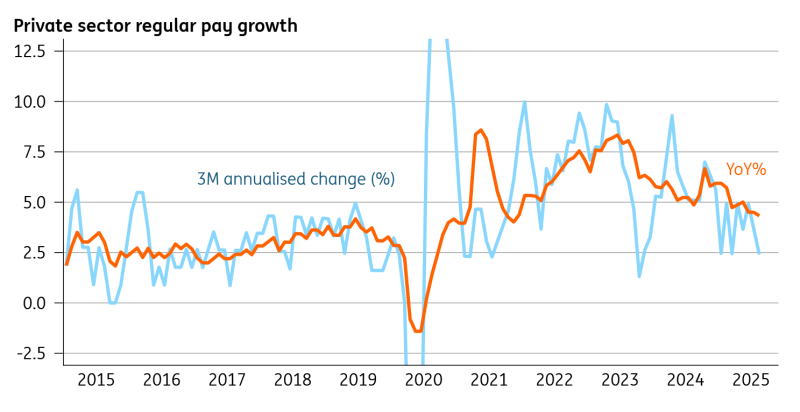

Pay growth among companies is now running at 4.4% in annual terms, down from 6% around the turn of the year. The news is even better if you look at the three-month annualised rate of private sector pay growth, which now sits at 2.4%. That suggests there’s a good chance now that the annual rate will fall below 4% by November.

It’s worth saying that this is already baked into the Bank’s forecasts. But remember that wage growth has consistently come in higher than most economists had expected over recent years. Simply seeing its latest forecasts materialise would go some way towards alleviating concerns about the upside risks to inflation.

Private sector wage growth is easing

Source: Macrobond, ING

That’s particularly true when you remember that the jobs market is still cooling. The unemployment rate nudged up to 4.8%. And payrolled employee numbers are still falling each month, albeit more gradually than earlier in the year. Surveys have turned marginally brighter on average, which suggests we’re past the peak impact of April’s tax hikes.

So far, so dovish. The only real fly in the ointment is that public sector pay growth is picking up. But this is linked to the sizeable real-terms increases in government spending in the current fiscal year, something that’s currently not planned to be repeated next year. Assuming that’s confirmed in the forthcoming Autumn Budget – a budget that’s likely to be dominated by tax hikes – then this should add to the case for further Bank of England easing.

As for the timing, a November rate cut now looks unlikely. But December is in play, given that this meeting falls after the budget. And assuming we see further falls in wage growth, coupled with a bit of undershooting on the Bank’s services inflation forecasts, then a Christmas rate cut is possible.

However, we think February is more likely, giving the Bank an extra month’s worth of data to look at before acting. We expect three cuts in 2026, which is more than markets are currently pricing.

Read the original analysis: Dovish UK jobs report bolsters case for further rate cuts

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.