Domino's Pizza (DPZ Stock): Rising crust, rising profits

Original content: Domino's Pizza (DPZ Stock): Rising crust, rising profits

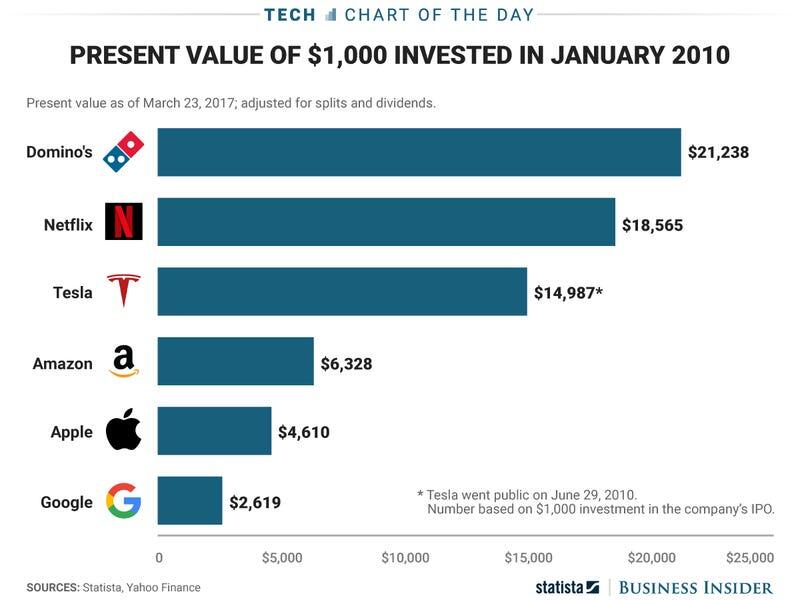

Around 2010, Domino's Pizza (NYSE: DPZ) was a struggling pizza chain, laughed at because of its quality control issues and poor ingredients. Shares fell below $3 in late 2009, and the company seemed doomed in the face of competition from Pizza Hut (NYSE: YUM) and Little Caesar's. Fast forward a little over ten years, and Dominos is arguably the world's largest pizza chain. However, with pressure from competitors and a market cap of over $20bn, is Domino's still priced well enough to be a worthwhile investment?

Turnaround of the Decade

Struggling heavily in late 2009, the company knew it had to do something. Determining that the key problem was the taste of the pizza itself, the company revamped its crust, sauce, and ingredients. It also appointed Patrick Doyle as the CEO, a decade-long Domino's executive who knew the company inside and out.

The company launched a stellar ad campaign to represent the changes in the company, and the results were almost immediate. Revenues surged from $1.4bn in FY09 to nearly $1.7bn in FY12. Same-store sales growth averaged out at around 5% during the same time, a figure that had been in the negative during FY09.

The company continued to improve and revamp its menu. Along with that, the company also finetuned its delivery service. Domino's was the first company to offer voice-based ordering on its app and even had a feature that instantly allowed customers to order their favorite pizza. With all these changes, the stock price continued to rise, backed by a consistent revenue and net income increase.

Riding the Technology Wave

Domino's is as much of a tech company as it is a pizza company. Around half of its orders are placed through digital means such as its mobile app. As such, it is currently pursuing innovative ways to cut costs and improve profits.

Domino's was the first company to complete a test delivery through an unmanned drone. Apart from this, the company has also been testing autonomous vehicles for delivering pizzas. Suppose the company manages to deliver its pizzas without the help of employees. In that case, it stands to save a fortune in wages and employee benefits.

Furthermore, since the company's food quality is no longer the problem, it stands to benefit from the rise in pizza demand. The stock price surged by over 10% when the company beat its 4Q21 earnings expectations. The company has managed to achieve this with a small increase in food prices and the delivery fee.

Although the company has faced pressure from third-party delivery services, the management believes that it only stands to lose 1-2% of its business in the long term. The business model of third-party delivery services is subpar, claims Domino's, citing the huge cut that aggregators take from each order.

All of these factors have led Pershing Square (AMS: PSH), managed by the renowned investor Bill Ackman, to invest over $1bn in Domino's between March-May 2021. An investment from Ackman is a huge sign of approval and could positively influence investor sentiment towards the company.

A Focus on Fundamentals

Dominos plans to expand by opening more stores. Despite being the world's largest pizza chain in terms of revenue, Pizza Hut (the company's main competitor) has a higher number of stores. In 2019, the company announced its plans to open 2000+ stores in the US by 2025.

However, the US is not the only market where Dominos plans to expand. The company has been focusing on Asia-Pacific heavily since 2014. It intends to do the same in the years to come.

There is no doubt that Dominos has a solid business model. However, potential investors have been wary of the $20bn market cap, citing that a P/E ratio of over 40 is too high for a pizza retailer. Despite that, it is hard to argue against 30 quarters of consecutive same-store sales growth. It is even harder to argue against a company that increased its revenue by 2.5x between FY09 and FY19 and plans to continue on the same trajectory in the years to come.

According to consensus estimates, revenue is expected to cross $5bn by FY23, with net income surging to $636m. This should prompt the company to increase its dividends. The stock price should also experience a modest increase following the earnings.

For the short term, Dominos plans to fuel growth by opening more stores and increasing revenues. In the long-term, the company plans to cut costs through innovative means (e.g., unmanned delivery). This way, the company has managed to bullet-proof its business model to quite an extent. As such, we believe that it is an ideal option for value-investors requiring long-term gains and consistently rising dividends.

Author

Baruch Silvermann

The Smart Investor

Baruch Silvermann is a personal finance expert, investor for more than 15 years, digital marketer and founder of The Smart Investor.