Dollar rally may endure beyond weak PCE

The white-hot and lightning-fast Dollar rally of June, which has swept USDEUR to its strongest since May of last year and propelled the broad DXY back above the 100 indexed level, below which it has lingered for most of the last 12 months, may yet have legs. Certainly, the Fed meeting of June 17th has acted as the firm catalyst for the most recent movement in the Dollar, but in many ways, the Fed may be forced to act regardless of whether it would like to or not.

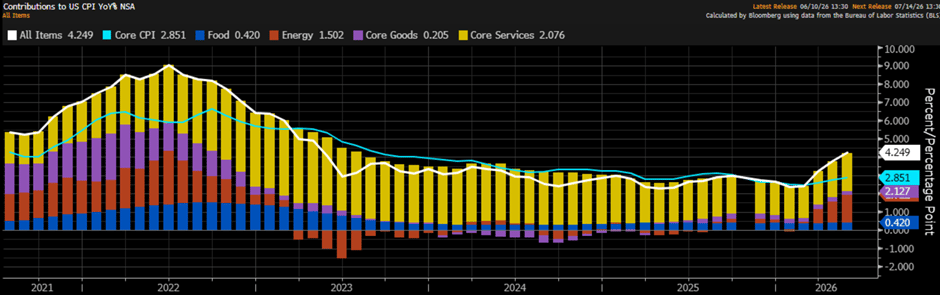

Now that the conflict and the blockade are, for the most part, concluded it makes sense that a routine 2nd-tier data point such as Personal Consumption Expenditure suddenly gains this level of intrigue and interest. The Fed’s benchmark is CPI, which has been above the 2% target for 64 consecutive months and currently sits at 4.2%, whether PCE is 3.5% or 3.6% is pale ale compared to this kind of extended performance.

Whether Warsh sees himself as the man to end this rueful run or whether he is simply the man left with the job, the Fed cannot endure such a period without damage to credibility. Certainly, the worst of the energy shock-induced inflation will, and possibly already has, evaporated, but the issue of high US CPI is more a story of services than goods.

The above chart shows the constituents of US CPI month by month, with services in yellow and energy in brown. Even a cursory glance tells the tale that US inflation is a services problem at its heart. Oil may steal a few months headlines, but the increasing cost of labour has proven a much more enduring problem for the Fed.

Warsh, the man who ‘does not believe in forward guidance’ gave plenty of it last week, even with what he didn’t say. Other FOMC members also seem to be taking a firm tone with regard to rates. The situation now is that the ECB started the talk before the Fed but soon lost its appetite once the Strait reopened, the BoE never started and the Fed’s just getting going.

Author

David Stritch

Caxton

Working as an FX Analyst at London-based payments provider Caxton since 2022, David has deftly guided clients through the immediate post-Liz Truss volatility, the 2020 and 2024 US elections and innumerable other crises and events.