Dollar dithers in thin trade as Trump passes aid package

The two themes that had been dominating the global macroeconomic landscape over the past many weeks were the US fiscal stimulus and EU-UK trade negotiations. There was a breakthrough on both the themes last week. The US Congress passed the USD 900bn stimulus package and the EU and the UK managed to reach a trade agreement.

As far as the EU-UK trade agreement is concerned, The devil would lie in the details. While a EU-UK trade agreement would avoid disruptions and ensure continuity for businesses over the short term, there are questions over how the enforcement of the deal would be ensured over the longer run and how disputes would be resolved. Even with the deal, output in the UK is likely to be 4% lower than potential according to estimates.

President Trump just signed the bill yesterday. His refusal to sign the stimulus bill passed by the Congress would delay benefits reaching those who need them the most. However, government shutdown has been averted. Without the bill being passed, funding would have dried out for several federal agencies. This could have had a serious debilitating effect on an economy where recovery is plateauing. The Georgia State Senate runoff elections assume even more significance now. Democrats are going to vote on expanding the cash transfers to USD 2000 from USD 600, however this may find resistance in the Republican controlled Senate. If Democrats manage to win both the seats in Georgia run off, they would end up have having control over the presidency, the Senate and the House. This would make doling out further stimulus a lot easier. Democrats winning the run offs could result in the next leg of USD weakness. If Republicans manage to retain control over Senate, we could see the Dollar see a relief rally.

PBoC has injected a lot of liquidity into the banking system. Chinese bond yields have moved lower. Onshore too bonds are likely to rally as the RBI announced a Rs 10000crs OMO twist on Friday. The government did not accept any bids in the 10y bond and instead borrowed more at the shorter end i.e. 2y and 5y and longer end. This caused the 10y bonds to rally post the cutoff on Friday. The OMO twist was announced post the cutoff.

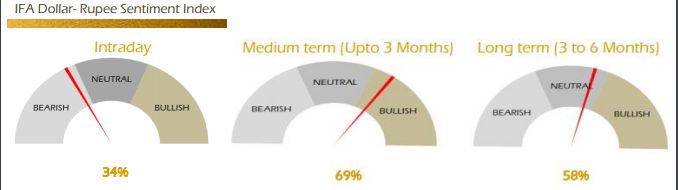

The price action in Rupee is likely to be largely flow driven in the coming week. There are likely to be few Global cues over the coming week on account of Christmas holidays. 73.40 is an extremely crucial support for USDINR. Participation is likely to remain muted and liquidity could be thin. We expect the RBI to continue buying Dollars in 73.40-73.50. Liquidity could dry up on Break of 73.40, leading to exaggerated moves. The December currency derivative expiry on Friday will be interesting given the high open interest due to RBI intervention. We expect the Rupee to trade in a 73.40-73.70 range intraday. Asian currencies are stronger against the USD. SGX is indicating a 100pt gain for Nifty on open.

Strategy: Exporters are advised to cover a part of their exposure on upticks to 73.80-73.90. Importers are advised to cover on dips to 73.40-73.50. The 3M range for USDINR is 73.00 – 75.40 and the 6M range is 73.00 – 76.00.

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.