Dismal Durable Goods Report: Inventories Up, Shipments and New Orders Down

The durable goods report was supposed to be a bad one. It was, but Boeing does not get most of the blame.

The Advance Durable Goods report on Shipments, Inventories, and new orders for April was a disaster.

New Orders: New orders for manufactured durable goods in April decreased $5.4 billion or 2.1 percent to $248.4 billion. This decrease, down two of the last three months, followed a 1.7 percent March increase. Excluding transportation, new orders were virtually unchanged. Excluding defense, new orders decreased 2.5 percent. Transportation equipment, also down two of the last three months, drove the decrease, $5.4 billion or 5.9 percent to $85.4 billion.

Shipments: Shipments of manufactured durable goods in April, down three of the last four months, decreased $4.0 billion or 1.6 percent to $253.3 billion. This followed a 0.5 percent March decrease. Transportation equipment, down four consecutive months, led the decrease, $3.7 billion or 4.1 percent to $85.8 billion.

Unfilled Orders: Unfilled orders for manufactured durable goods in April, down two of the last three months, decreased $0.7 billion or 0.1 percent to $1,179.1 billion. This followed a 0.1 percent March increase. Transportation equipment, also down two of the last three months, led the decrease, $0.4 billion or 0.1 percent to $810.6 billion.

Inventories: Inventories of manufactured durable goods in April, up nine of the last ten months, increased $1.8 billion or 0.4 percent to $422.6 billion. This followed a 0.3 percent March increase. Transportation equipment, also up nine of the last ten months, led the increase, $1.5 billion or 1.1 percent to $136.1 billion.

Capital Goods: Nondefense new orders for capital goods in April decreased $3.9 billion or 5.0 percent to $74.0 billion. Shipments decreased $2.4 billion or 3.0 percent to $75.9 billion. Unfilled orders decreased $2.0 billion or 0.3 percent to $705.3 billion. Inventories increased $0.9 billion or 0.5 percent to $185.9 billion. Defense new orders for capital goods in April increased $0.7 billion or 4.8 percent to $14.7 billion. Shipments increased $0.3 billion or 2.6 percent to $12.8 billion. Unfilled orders increased $1.9 billion or 1.2 percent to $159.2 billion. Inventories increased $0.1 billion or 0.6 percent to $23.4 billion.

Revised March Data: Revised seasonally adjusted March figures for all manufacturing industries, based on updated seasonal adjustment models, were: new orders, $503.5 billion (revised from $506.2 billion); shipments, $507.1 billion (revised from $508.5 billion); unfilled orders, $1,179.8 billion (revised from $1,181.1 billion) and total inventories, $691.3 billion (revised from $690.7 billion).

Econoday Comments

The Econoday economists expected a disaster thanks to Boeing. The report was an across-the-board disaster, but Boeing had little to do with it. Emphasis is mine.

There's no Boeing-related catastrophe yet but manufacturing is indeed slumping, confirmed by a broadly weak durable goods report for April. Orders in the month fell 2.1 percent to nearly hit Econoday's very soft consensus for 2.2 percent while ex-transportation orders were unchanged and again very near expectations for a 0.1 percent decline. What came in at the bottom of expectations were orders for core capital goods which fell 0.9 percent in April. And a sharp downward revision for this category in March, to a 0.3 percent increase from an initially reported 1.3 percent rise, underscores the fundamental slowing underway in manufacturing demand.

The list of negatives is unfortunately convincing: orders for primary metals down 0.8 and 1.9 percent the last two months; fabrications up 0.4 percent in April but following 1.6 and 2.1 percent declines the prior two reports; machinery up 0.1 percent in April following a 2.0 percent drop in March; new vehicles down 3.4 percent in April and civilian aircraft down 39 percent.

Civilian aircraft is always volatile month-to-month but April's decline is tame given outside expectations for gigantic contractions tied to 737 cancellations. Unfilled orders for civilian aircraft did slip but only 0.3 percent in April vs declines of 0.1 and 0.5 percent in the prior two months.

The big 737 fallout, if there will be one, has yet to hit but what is hitting is generally sliding demand for manufactured goods in what reflects generally weak global demand. But it's the decline in capital goods that headlines April, pointing to lack of momentum for business investment going into May and the breakdown of US-China trade talks.

Key Points

- Shipments are down. Shipments feed GDP.

- Unfilled orders are down. That's a reflection on future hiring needs.

- Core capital goods are a measure of future business expansion. The March revision to the downside was massive, from +1.3% to +0.3%. April was -0.9%. Economists expected +0.1%. Oops.

- Inventories are up for the 9th time in 10 months. I suspect Trump's tariffs might be the reason. Companies were stocking up to get ahead of price increases. This artificially boosted GDP in the first quarter.

This was a very weak report and it does not yet reflect much of Boeing.

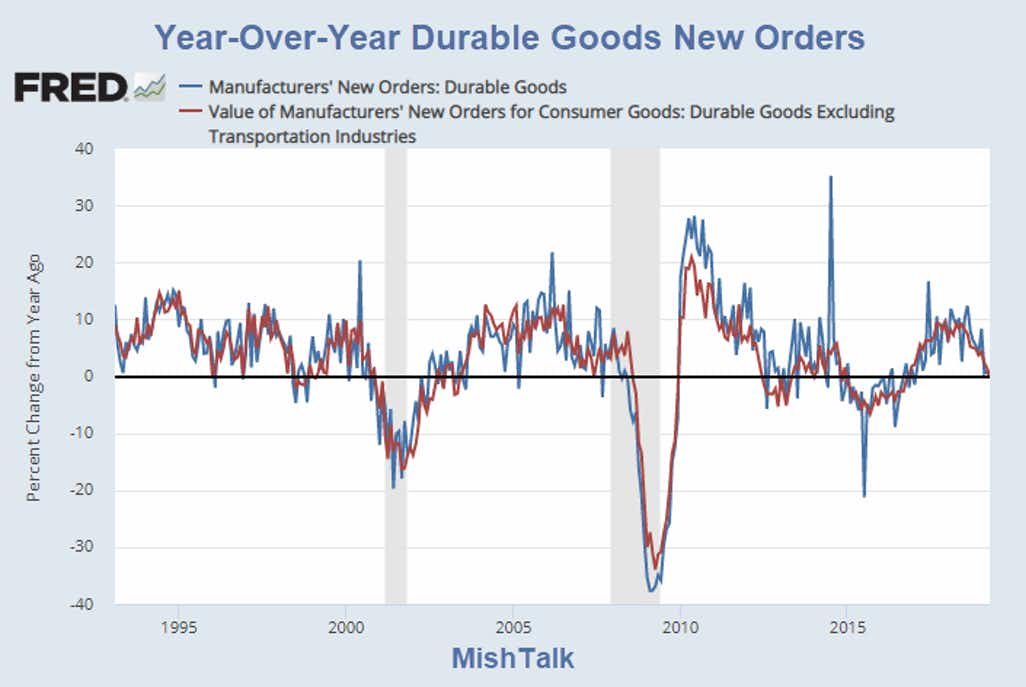

Year-over-year new orders are treading water to very slightly negative.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc