Developed economies: Housing prices and bubble risk

In many developed countries, housing prices have risen very sharply since the Covid-19 crisis. In the United States they jumped 37% between the 4th quarter of 2019 and the 2nd quarter of 2022. In Germany and the United Kingdom, the increases have also been significant and were 23.8% and 18.6% respectively over the same period. The increases in Italy (+7.4%) and Spain (+10.8%) were more restrained, while France (+14.1%) and Japan (+15%) were somewhere in between.

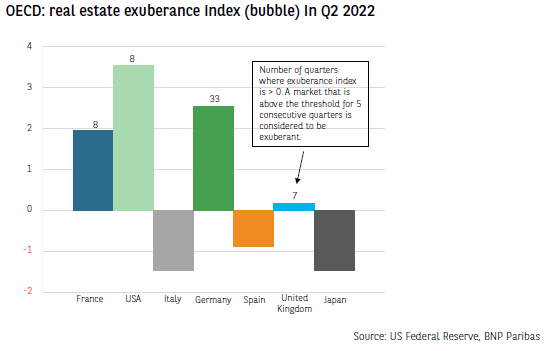

Can such price increases be justified in terms of fundamentals or are they more indicative of a real estate bubble? In order to quantify this, the Dallas Fed publishes a housing prices exuberance index each quarter. This is calculated as the difference between observed prices and a counterfactual which is intended to reflect the intrinsic value (“fair value”) based on fundamentals such as the demographic evolution of each country. The Fed indicates that the market can be described as exuberant if the index is positive for five consecutive quarters. Four of the major OECD countries are now exhibiting a risk of a bubble in their property markets: the United States, Germany, France and the United Kingdom. The risk seems particularly significant in Germany, where the index was in positive territory for the 33rd consecutive quarter.

Since the end of 2021 (in the United States and Spain) and the start of 2022 (in Germany and France), the index has tended to fall. In the past, a drop in the exuberance index has been an indicator that housing prices were likely to fall. This was the case in the early 90s when the Dallas Fed index reversed in most countries from 1989, while housing prices contracted in 1990-1991. An even more significant example is the 2008 financial crisis, because from 2005 the bubble detection indicator turned negative in most countries, whereas the real estate bubble only imploded in 2007-2008. In retrospect, therefore, it does appear that this indicator provides a precursor signal about excessive dwellings valuations.

If the index continues to fall in the coming quarters, a correction in housing prices can be expected. Up to the present time, prices have continued to rise (an average rise of 3.1% q/q in Q2 2022 in the main OECD countries), despite the rise in interest rates on new home loans and the tightening of conditions for granting loans. So for the time being prices are continuing to offer resistance, but for how much longer?

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.