DAX punches higher as Asian stocks rebound

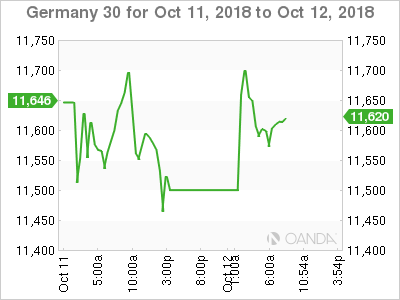

The DAX index has rebounded in the Friday session, posting gains. Currently, the index is at 11,617, up 0.68% since the Thursday close. In economic news, German Final CPI gained 0.4%, matching the forecast. Eurozone Industrial Production jumped 1.0%, well above the estimate of 0.4%.

It’s been a brutal week for global equity markets, but there has been some relief on Friday. Asian markets recorded gains, lifting European markets as well. Even with Friday’s gains, the DAX has declined 3.5% this week. Two key factors in the sharp decline are the spike in U.S bond yields and growing fears about the impact of the U.S-China trade war. The DAX touched a low of 12,518 this week, its worst showing since February 2017. If bond yields continue to rise next week, the DAX could face further headwinds next week.

German inflation climbed 2.3% in September on a year-to-year basis, its strongest gain since November 2011. Not surprisingly, much of the increase is a result of higher energy prices, as brent crude remains above $80 a barrel. Eurozone inflation has also been moving higher and is finally closing in on the ECB’s target of just below 2 percent. Stronger inflation has reinforced speculation that the ECB could raise interest rates for the first time in years in the second half of 2019.

The ECB opted to maintain its monetary policy at its September meeting, but not without some handwringing, according to the ECB minutes, released on Thursday. Policymakers debated whether to lower their risk assessment, clearly concerned that global trade tensions could dampen eurozone growth. However, the policymakers decided that the eurozone economy was strong enough to allow the ECB to maintain its ‘slow but steady’ stance of tightening policy. The ECB remains on track to end its massive bond purchase program at the end of the year. Meanwhile, with bond yields pointing higher, investors have reacted negatively and stock markets continue to spin lower. On Thursday, German 10-year bonds fetched 0.55%, marking a 6-month high.

Economic Calendar

Friday (October 12)

2:00 German Final CPI. Estimate 0.4%. Actual 0.4%

5:00 Eurozone Industrial Production. Estimate 0.4%. Actual 1.0%

Day 1 – IMF Meetings

Author

Kenny Fisher

MarketPulse

A highly experienced financial market analyst with a focus on fundamental analysis, Kenneth Fisher’s daily commentary covers a broad range of markets including forex, equities and commodities.