DAX boosted by car makers on talk of tariff deal

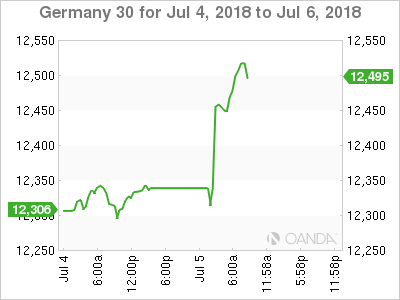

The DAX index has posted strong gains in the Thursday session. Currently, the DAX is at 12,505, up 1.58% on the day. On the release front, German Factory Orders jumped 2.6%, crushing the estimate of 1.1%. Eurozone Retail PMI ticked higher to 51.8 points. Later in the day, the Federal Reserve will release the minutes of the June policy meeting.

The escalating trade war between the U.S and the EU has raised concerns that the eurozone export sector could hit some significant headwinds. President Trump has threatened to impose tariffs of 20 percent on European car imports if the EU does not remove their tariffs on U.S. automobiles. The EU would clearly prefer not to engage in a full-blown tariff war with the United States. European officials are examining the possibility of a tariff-cutting agreement between the world’s largest car exporters. In essence, this would allow the EU and the U.S to reach a deal on automobile tariffs without going through the World Trade Organization. On Thursday, automobile manufacturers are sharply higher on the DAX index. BMW is up 4.97%, Daimler has climbed 4.58% and Volkswagen has jumped 4.79%.

Chancellor Angela Merkel is working overtime to save her coalition, and the latest crisis she is facing is over migration policy. Interior Minister Horst Seehofer had threatened to resign over the migration agreement that EU leaders reached in Brussels last week, but has decided to remain in the government. Merkel’s proposal involves setting up special transit centers at the border with Austria and having refugees return to EU countries were they had first registered, but Austria has expressed concern with the plan. The EU remains split on migration policy, and if Germany’s political crisis continues, European equity markets could fall.

Markets on hold, eyeing tariff implementation

Big Trouble in Big China?

Economic Calendar

-

3:15 Spanish Services PMI. Estimate 56.3. Actual 55.4

-

3:45 Italian Services PMI. Estimate 53.3. Actual 54.3

-

3:50 French Final Services PMI. Estimate 56.4. Actual 55.9

-

3:55 German Final Services PMI. Estimate 53.9. Actual 54.5

-

4:00 Eurozone Final Services PMI. Estimate 55.0. Actual 55.2

-

2:00 German Factory Orders. Estimate 1.1%

-

4:10 Eurozone Retail PMI

-

7:15 German Buba President Weidmann Speaks

-

8:15 US ADP Nonfarm Employment Change. Estimate 190K

-

8:30 US Unemployment Claims. Estimate 231K

-

10:00 US ISM Non-Manufacturing PMI. Estimate 58.3

-

14:00 US FOMC Meeting Minutes

Previous Close: 12,317 Open: 12,336 Low: 12,336 High: 12,514 Close: 12,503

Author

Kenny Fisher

MarketPulse

A highly experienced financial market analyst with a focus on fundamental analysis, Kenneth Fisher’s daily commentary covers a broad range of markets including forex, equities and commodities.