Counting the ways AUD is set to rise

The RBA has gone out of its way to damp down expectations that it will hike rates for some time; pointing to slack in the labour market, a higher exchange rate, retail competition intensifying as Amazon enters the Australia market, a subdued outlook for business investment, risk in the housing market and from household debt, and a weaker outlook for China and Australia’s terms of trade. Meanwhile, The Australian economy is punching out some of the strongest broad-based activity numbers in some time. Forward indicators of business investment and employment have accelerated, and inflation is set for a bump in the second half of this year on a surge in electricity prices and a jump in the minimum award wage. And the terms of trade are rising on renewed strength in Chinese commodity demand and a synchronized global economic recovery. The Australian external balance has virtually disappeared; at a low in over 30 years. As we have noted in recent reports, while the Australian economy is gaining momentum, New Zealand economic growth has slowed. On a number of counts (external balance, political risk, housing markets, construction trends, commodity price trends) the AUD comes out ahead of the NZD. The RBNZ quarterly policy statement on Thursday is likely to try and emulate the RBA effort to damp down interest rate hike expectations and the exchange rate. The AUD/NZD long run average is between 1.15 and 1.20, much higher than the current 1.075. There are few reasons to argue why it should not already be back up there, if not higher.

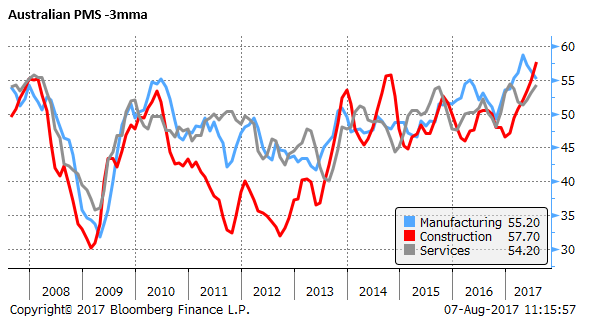

Australian Construction activity booming

On Monday, the AiG construction sector PMI rose to a record high of 60.5 in July (in data back to 2005). It was also at a record high on a 3mth (57.7) and 6mth (54.9) average basis, suggesting that this is not just a flash in the pan.

The AiG notes that, “the further upturn in industry conditions reflected expanding activity across all four major construction sectors.”

Government infrastructure spending is starting to influence the data, pushing up the engineering construction sector (+6.9 to 57.5).

We noted in our report last week that non-residential approvals were up 27% 3mth-yoy in June, helping push up the commercial construction sector (+9.8 to 64.3).

Construction, Commodities, and Politics build case for AUD/NZD; 3 August

Stamp duty reductions that came into effect on 1 July in the two largest states (NSW and Victoria) are reported to have led an increase in first home buyer activity. House building rose 3.4 to 62.4.

The weakest sector in the last year has been apartments, with approvals peaking last year. But the sector recovered in July, up 4.3 to 52.6.

The forward looking aspect of the survey was the strongest, with new orders rising 2.7 to 64.6. The employment component rose strongly 4.8 to 59.0, and the wages component rose 3.7 to 64.6, suggesting the sector will help lift wage growth in coming quarters.

Broad-based business confidence

The Construction PMI was the last of the three PMI reports to be released for July. It completes a relatively strong set of data. The three-month average for services was 54.2, manufacturing 55.2 and construction 57.7.

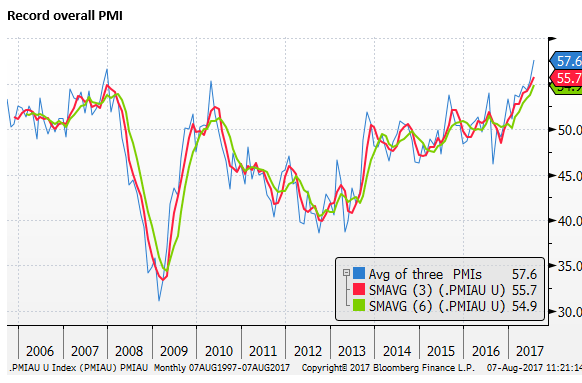

The chart below shows the simple average of the three sector PMI and the three and six month average for this overall PMI. The overall PMI was at a record high in the month, and on a three and six-month average basis in data back to 2005.

The NAB business survey is released later today. It is showing similar broad strength in the economy. The current conditions component was at a high in June since 2008. Other closely watched components were not clearly as strong. If the PMIs are any guide, we might expect another strong reading in the NAB survey with solid increases in other components, such as for confidence, employment, and investment intentions.

One component of the survey that is worth paying attention to is that for labour costs. It rose 1.1%q/q in June, a high since 2012, suggesting the wage growth data may be starting to pick-up from record lows in the national data (1.9%y/y in Q1).

RBA business investment outlook is conservative

The business survey data suggest that the RBA’s forecasts for growth presented last week may be conservative. The RBA said in their 3-August Statement on Monetary Policy that “[business] survey measures are at their highs since early-2008. It further said that, “Many of the conditions that would typically be associated with stronger growth in investment are in place, including low interest rates and high capacity utilisation.” And that, “Some spillover from the large pipeline of public infrastructure activity to private sector investment could also be envisaged.”

Sounds pretty positive! However, it forecast “a relatively gradual increase in non-mining business investment growth.” The RBA noted that, “Investment intentions in the ABS Capex survey suggest that non-mining investment is unlikely to pick up substantially over the next year or so.”

The RBA admits that this survey only accounts for around half the economy, and omits certain service sectors that have been rising more strongly recently. The most recent data is from Q1; so it may also not be picking up more recent strength in the economy.

In its risk section on business investment, the RBA said, “there is a risk that investment will pick up by much more than is forecast at some point. If a turning point in non-mining business investment becomes apparent, there could be a substantial upward revision to the forecast profile. On the other hand, a recovery in non-mining investment has been forecast for some time and, given the subdued signals from some leading indicators, it remains possible that a substantial pick-up is still some way off.”

The RBA has forecast that business investment will remain subdued. Their own analysis highlights the risk that they may be underestimating its strength. The most recent data suggests that the probability has shifted towards stronger private and public sector investment spending that reinforces each other.

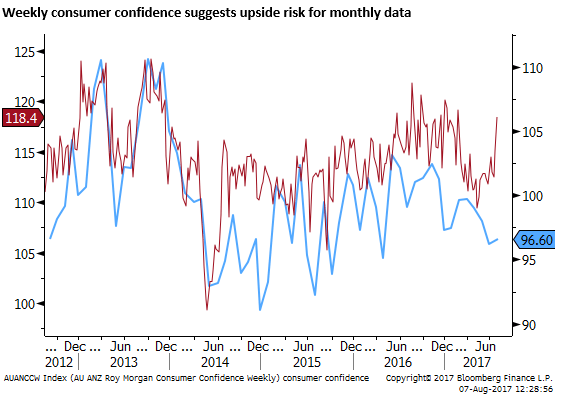

Consumer confidence also set to print higher

On Wednesday, the Westpac monthly consumer confidence data are due to be released for August. The weekly data point to a significant upside risk for this report. There seems little reason for the weekly data not to be repeated in the monthly survey. Perhaps the only reason is that the RBA appears to have gone out of its way to talk down the potential for the economy, it seems in an effort to discourage the AUD from rising further.

Too much focus on the housing tail risk

The RBA and many market commentators have expressed a subdued outlook for the Australian economy due to high levels of household debt and a view that the housing market is peaking. Such concerns are valid, but they also appear to be blinding the market to pretty clear signs of a broad-based pickup in the economy.

The facts are that housing credit growth remains stable and continues at above income growth. So households are not, it seems, trying to consolidate their debt. While investor loan growth has slowed, owner-occupier loan growth has picked up.

Consumer spending was quite weak in Q1, helping support the notion that household debt and housing market softness were spilling over the weaker consumer activity. However, retail spending recovered solidly in Q2, so it’s not clear that households are dragging on growth.

The housing market has not slowed all that much. It may have lost some momentum with softer foreign and investor demand, but the price growth and auction clearance rates are still quite robust.

The tightening in credit conditions since last year is relatively modest, taking interest rate somewhat higher for investors, more so for interest only loans, while in fact, they are somewhat lower for owner-occupiers willing to pay off some principal with interest.

The RBA SoMP said, “Since May, most lenders have increased their standard variable reference rates for interest-only loans by around 30 basis points and reduced standard variable rates for principal-and-interest loans to owner-occupiers by around 5 basis points.”

“The net effect of these changes is estimated to have increased the average outstanding variable interest rate by around 5 basis points. In combination with the increases previously announced since last November, this implies a rise in the average outstanding variable interest rate of 15–20 basis points.”

However, the RBA admits that “the increase in the average rate …. is expected to be less than this estimate” due to: switching from interest-only to principle-and-interest loans; discount rates offered by banks have not risen as much; and fixed-rate borrowers rolling into lower fixed-rates.

As such, rates faced by households on average have risen by significantly less that one standard RBA policy rate increase from record lows last year. Looking ahead, households might feel quite comfortable about their financial situation since the RBA has dampened expectations that they will hike rates for the foreseeable future.

As such, we should not expect frugal households and lower credit growth to drag down the economy in the near term. In the meantime, stronger employment prospects may underpin consumer spending. It may also continue to underpin the housing market, despite some headwinds.

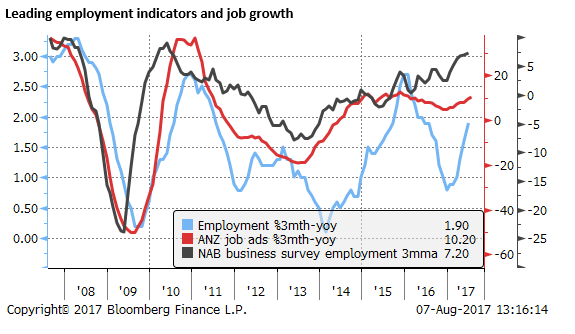

Job ads strong

Job ads rose 1.5%m/m in July (reported on Monday), following 2.7%m/m in June. They are up 1.6% on a three-month average; annualising at over 20%. Job ads are up 10.2% 3mth-yoy, a high annual growth rate since Jan-2016. Employment indicators continue to point to accelerating jobs growth.

The RBA is forecasting only a modest fall in the unemployment rate over the next two years. However, the recent data suggests risks lie towards faster job growth.

Inflation set to rise further

As we head into Q3, and the likelihood that the market will be woken up to a strengthening Australian economy, the inflation data are also set to print higher. The RBA sees some of these increases as temporary and has a subdued outlook for inflation over its forecast horizon. However, the market may shift its outlook when faced with stronger economic growth, lower unemployment, and higher Q3 inflation.

Inflation in the second half may get a boost from a sizable bump to the minimum wage that came into effect on 1 July. The minimum wage rose 3.3% on 1 July, a one-off increase that will hit the quarterly data, compared to a record low 1.9%y/y rise in the overall Wage Price Index (0.5%q/q) in Q1.

The RBA estimated that the direct impact on the WPI of the minimum wage increase in Q3 will be 0.5%, larger than the average direct contribution of 0.3% since 2010. The RBA also expect the rise in the minimum wage to flow onto other wages adding a further 0.25 to 0.5% to the WPI growth. This might be in addition to the underlying growth rate. As such, the WPI index is likely to appear to have bottomed in the first half of this year.

Secondly, the RBA noted that, “The announcement of price increases by a number of electricity and gas providers points to a significant pick-up in utilities inflation in both the September quarter 2017 and the March quarter 2018. Along with the direct effects on household utility bills, there will also be indirect effects on inflation as a result of rising business input costs.”

The rise in utility bills is relatively unique to Australia and reflects a jump in wholesale electricity prices this year on shortages related to under-investment in baseload power supplies blamed on inconsistent government policy on greenhouse gas targets, and some older coal plants closed in the last year. As such, this could be a prolonged issue for electricity prices.

Whether inflation takes off in the next two years remains to be seen, but sequentially the market is likely to see inflation continuing to rise this year, after bottoming last year, reaching the RBA’s 2 to 3% inflation target.

Evidence of faster economic growth and rising inflation may place pressure on the RBA to reassess its rates policy later in the year.

Recall the estimates of neutral rates by the RBA (3.5%) that they have told us to ignore? The market is still right to wonder at what point the RBA begins to normalise policy. Certainly, this starts well before policy targets are achieved.

Author

Greg Gibbs

Amplifying Global FX Capital

Greg has had a long career in foreign exchange. He began his career at the Reserve Bank of Australia in 1989 and in the early 1990s he was the first economics graduate at the Bank to be assigned to the foreign exchange dealing desk.