Could This Really Be Another Round In The Trade War Coming? [Video]

![Could This Really Be Another Round In The Trade War Coming? [Video]](https://editorial.fxstreet.com/images/Markets/Equities/stock-certificates-11742678_XtraLarge.jpg)

US data came in weak

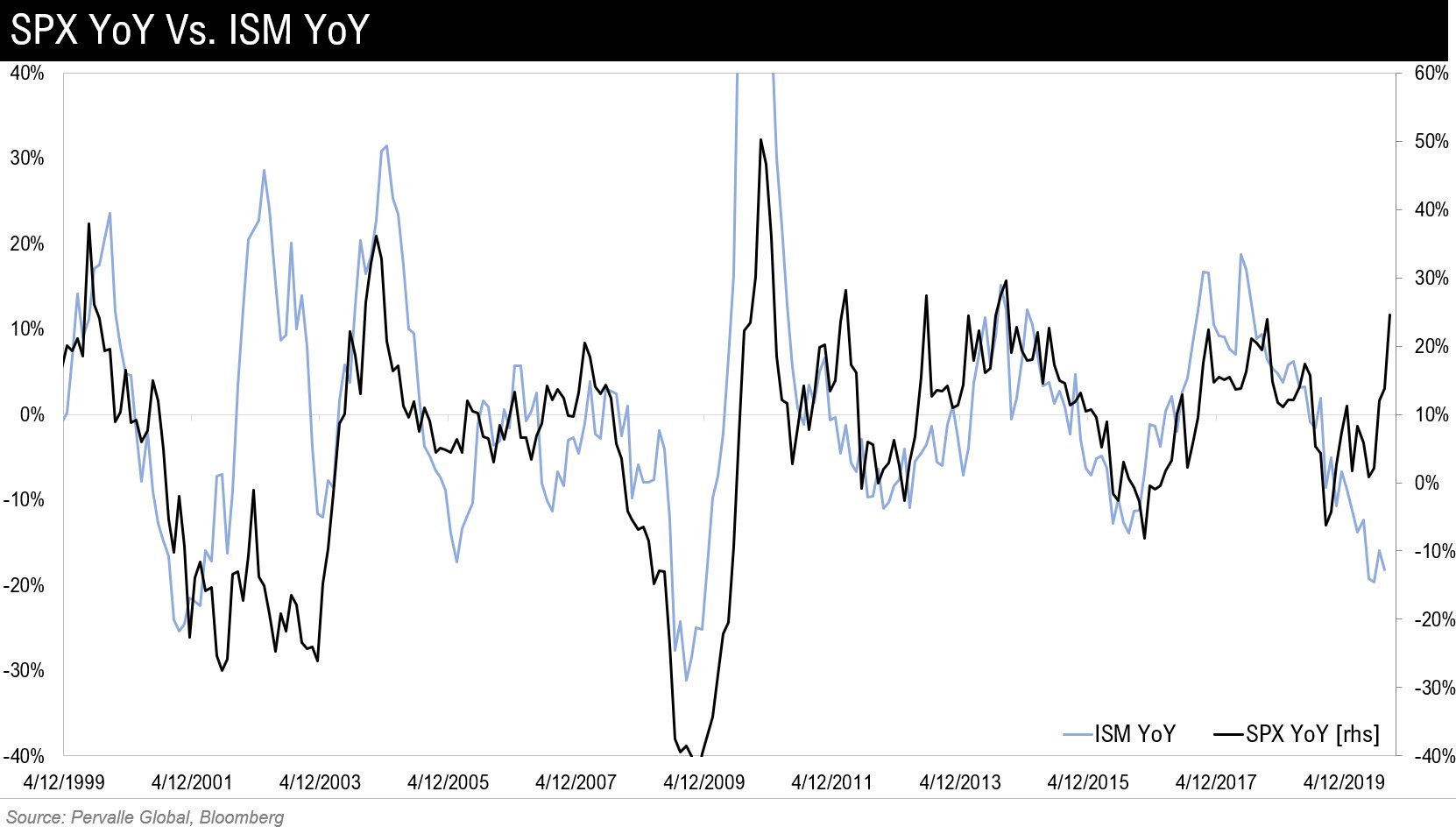

The US ISM manufacturing for November came in weaker than expected and all its subcomponents contributed to the weakness that ut the indicator to its lowest reading since 2014. Adding to it is the ISM Institute’s statement saying that even if the tariff issue was resolved people are not going to invest before the election, which makes the outlook for the US for the coming year quite negative. Looking at the chart below you can see that the S&P and ISM do correlate quite strongly and presently show a big divergence which could point to a bigger stock market drop coming.

New and more tariffs

Secretary Wilbur Ross made it clear that if China continues to “drag its feet” new and more tariffs are coming by December 15th. de any and all Chinese goods which would impact the everyday American life. It seems Donald is firm on this and by re-introducing tariffs for Steel and Aluminum from Brazil and Argentina he showed that he is not playing around, after it looked that Brazil may be devaluing its own currency to sell more agricultural goods to China.

China not backing down

On top of all this the US Congress plans to pass a Xinjiang-related bill and China is reacting with Visa restrictions. In a nutshell it seems China is not giving in to US pressure and with the tides of the economy possibly shifting in favor of China based on yesterday’s PMI readings, we could be in for another round of a trade war cycle between the US and China.

USD

The USD took a strong hit yesterday after the negative data out of the US and further Tweets by the POTUS requesting the Fed to ease further have contributed to further weakness in the USD that could be seeing significant more downside from here if the present situation continues to unfold this way.

EUR

The EUR benefited from the USD weakness yet was not able to gain above the so important 1,11 round figure. Should we see a break of that level and it holds on a daily closed basis we could expect the EUR to recover further from here as the price of the common currency does seem to be undervalued after it gave away a lot of its strength since mid 2018.

NZD

the Kiwi sees the big winner at the moment, not only do good news out of China help the NZD but also the news about a significant stimulus package coming soon is keeping the expectations for further upside in the NZD alive. In addition the RBA out of Australia stood pat on its rates today making clear that they will wait and see from here, which is also helping.

Oil

The price of Oil hardly moved after its big drop and is likely to wait for new input in the trade war saga and oil stocks tomorrow to see if there is an oversupply which could push its price further lower.

Gold

Not much news for the shiny yellow metal at the moment. Gold was not able to benefit from USD weakness just yet. That said in case we see the Phase 1 deal fall through, then Gold could quickly recover back to $1,480 level and beyond.

BTC

Bitcoin sees unable to break higher and remains thus far supported around the $7,2k level. Yet the price action suggests that there are many attempts to push the price lower than the $7,2k which has held so far. Compared to the price action on the way up, the bias appears to remain rather bearish.

Author

Alexander Douedari

Independent Analyst

Alexander Douedari is an Award Winning Hedge Fund Manager and Selfmade 7-Figure Trader. Now Mentor for Students all around the world.