The current crop of Democratic contenders can't beat Trump

Highlights:

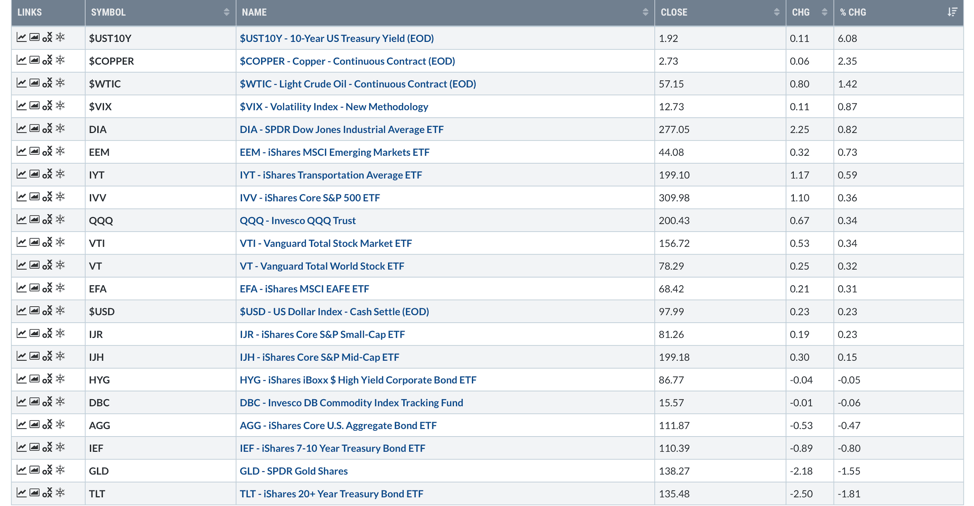

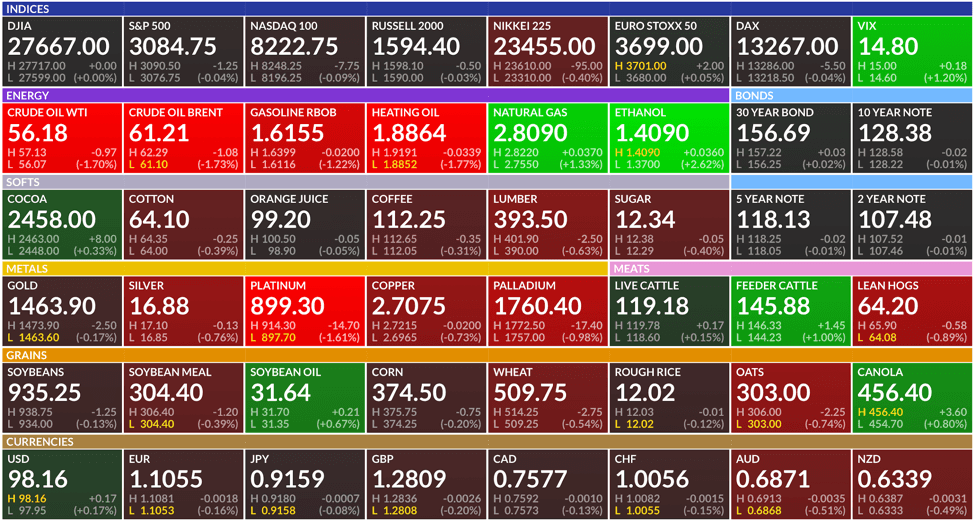

Market Summary: Markets moved higher yesterday on news that the U.S. and China planned to roll back tariffs. U.S. 10-year yields surged in one of the biggest single day moves in history. Bonds and gold fell in response to the 11 basis point move higher in the 10-year Treasury note yield. The S&P 500 ETF (IVV) finished the day up 0.36%. Copper and crude oil were both up more than 1% for the day.

Top Three Things:

Volatility: The VIX finished higher yesterday, despite the move up in equities. Furthermore, the VIX is holding above support at 12. We would like to see a breakdown in the VIX, below 12, which could be indicative of further upside in equities and a return to a lower volatility regime. With record short positioning in the VIX, this seems like an increasingly challenging scenario.

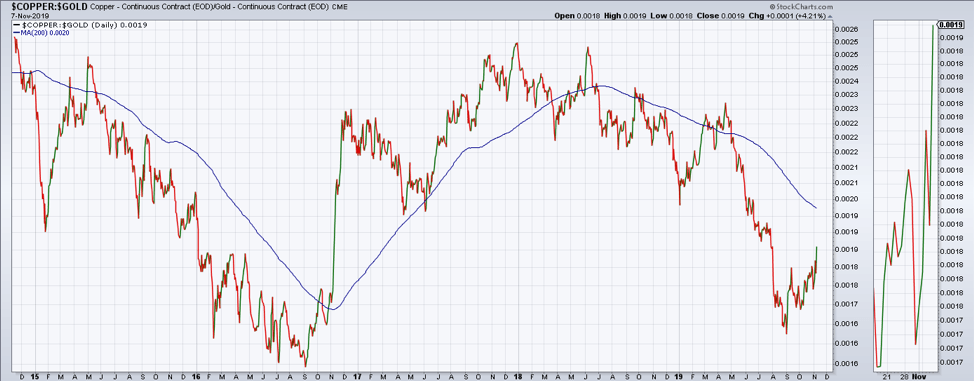

Copper to Gold: Copper surged more than 4% against gold yesterday. The ratio remains below its falling 200-day moving average and in a negative trend. However, a reversal of this trend could suggest that economic growth is set to accelerate and that interest rates should move higher. The data is not confirming this type of environment, so we will be watching this relationship closely.

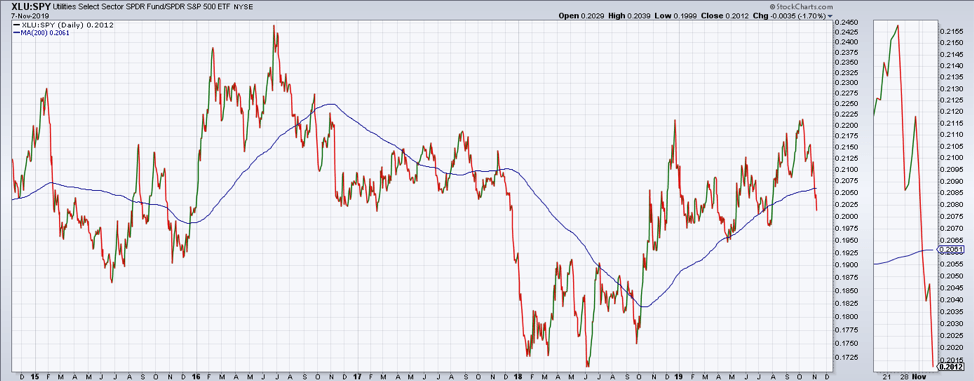

Utilities: The utilities sector broke below the 200-day moving average relative to the S&P 500. When this ratio is moving down, it is indicative of strength in cyclical segments of the market. Utilities have shown strength relative to the S&P 500 for the better part of the last year. The breakdown in this relationship suggests that defensive are weakening.

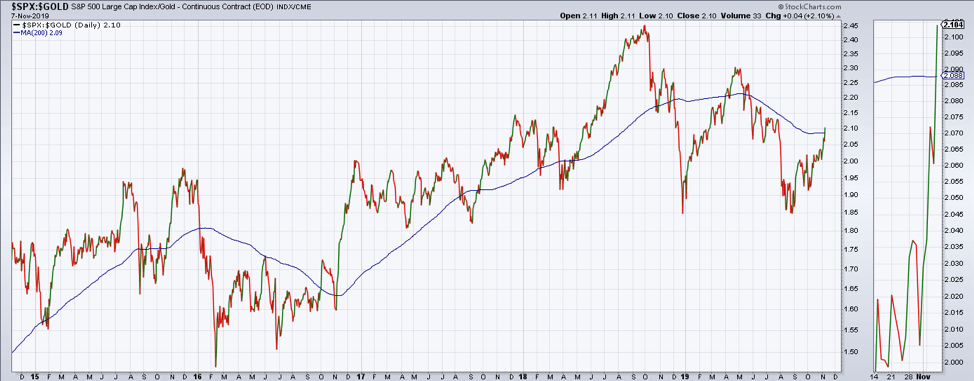

Chart of the Day: Stocks have rallied enough against gold to break back above the 200-day moving average. Is this a move to another lower high or the start of a new uptrend and cyclical rotation?

Futures Summary:

News from Bloomberg:

U.S. and Chinese officials said they agreed to roll back tariffs in stages, but presidential trade adviser Peter Navarro told Fox: "There is no agreement at this time to remove any of the existing tariffs as a condition of the phase one deal." White House colleague Larry Kudlow said there will be concessions. Meanwhile, China's imports from the U.S. plunged 21.5% in yuan terms in the first 10 months, while exports slid 6.8%. Overall, though, imports and exports fell less than expected.

Investors are waiting for signs of movement on trade. Global stocks are ending a strong week on a down note. U.S. equity-index futures posted modest losses, while the dollar and Treasuries both climbed. The yuan's eight-day rally came to a halt. Gold headed for its worst week since 2016 and Crude slid more than 1%.

Disney got Amazon on board for its streaming service. Disney+ will appear on Amazon, Samsung and LG devices. It had already signed pacts with Apple and Roku. The $7-a-month service featuring most of its best films and TV shows debuts Nov. 12.

Alibaba is aiming to raise up to $15 billion in a Hong Kong IPO. The company is gearing up for a listing hearing next week. It had aimed to list over the summer but was derailed by protests in Hong Kong and trade tensions. A solid result from its Singles' Day shopping event on Monday would be the perfect precursor for a share sale.

Michael Bloomberg may run for president. The former New York mayor is concerned the current crop of Democratic contenders can't beat Trump, adviser Howard Wolfson said. The 77-year-old may file candidate paperwork in Alabama, where the deadline is today, according to media reports. Several other states, including New Hampshire, have filing deadlines next week.

Author

Clint Sorenson, CFA, CMT

WealthShield