Consumers remain downbeat about jobs market

Summary

Consumers are worried about the jobs market and that's weighing on overall moods. Consumer confidence remains within its narrow range of the past two years, though there are some glimmers of hope about expectations for lower interest rates.

All about jobs

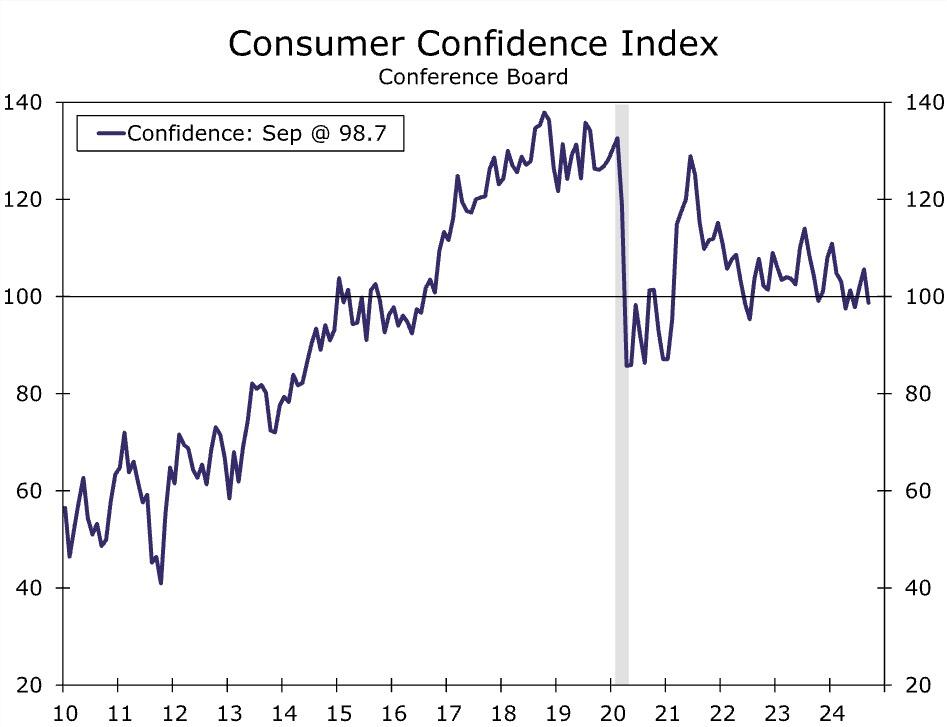

Consumers remain downbeat on the economy. The overall consumer confidence index slipped nearly seven points in September marking the largest one-month drop in three years. Part of the decline wasdue to more confident consumers in August—confidence was revised up to 105.6 last month (from 103.3 previously). At 98.7 in September, confidence remains well-within its recent range (chart). While households grew more pessimistic in both their present situation and expectations about the future, views on current conditions were responsible for most of the pullback. The present situation index has now pulled back to 124.3, notably the lowest value since coming out of the pandemic in early 2021.

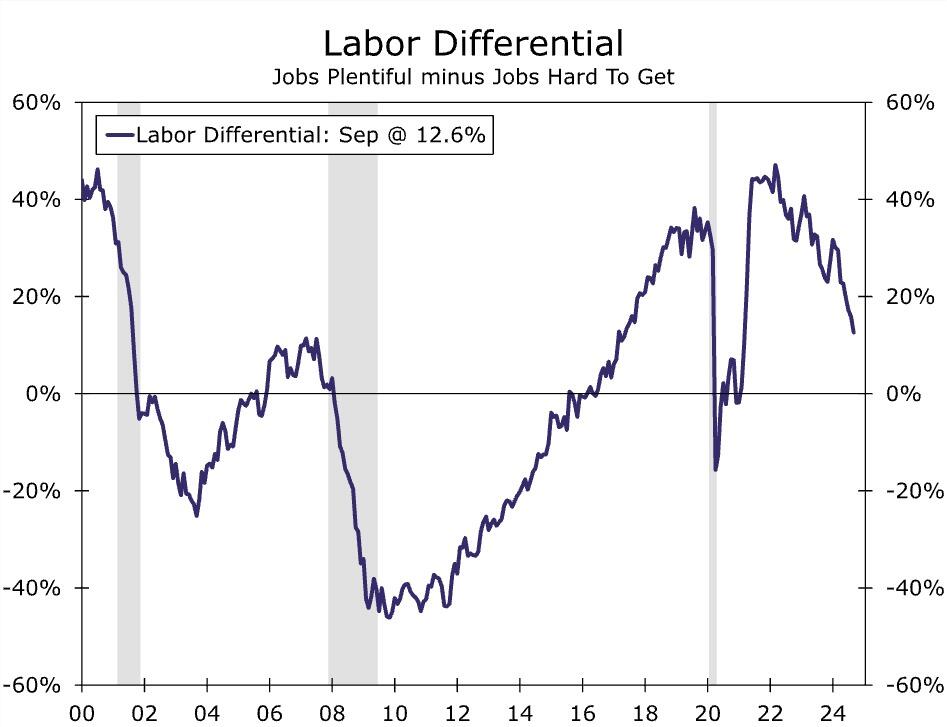

While we expect there are a number of reasons households are growing more pessimistic, the moderating labor market remains top of mind. The labor market differential, which is the difference between the share of consumers who view jobs as “plentiful” less those who view jobs as “hard to get,” also fell to its lowest reading since March 2021 (chart). The persistent drop in this measure is a clear sign that the labor market is not nearly as tight as it once was. That said, we're hesitant to put too much weight on this data given broader confidence measures have remained depressed this cycle despite resilient spending habits of households.

Moods may brighten as Fed eases

The survey cutoff date was September 17, which means even if households were hopeful of lower rates, the decision by the Federal Open Market Committee to cut interest rates by a historically-large 50 bps at its September 19 FOMC meeting are not fully reflected in this morning's consumer confidence data.

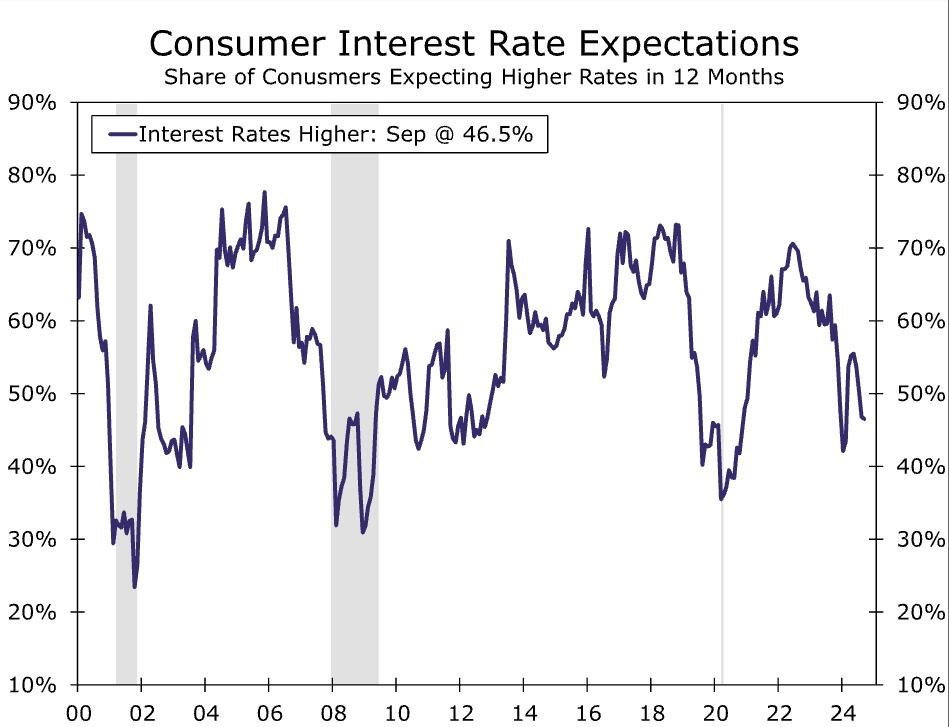

The share of consumers expecting higher interest rates within the next twelve months declined for a fourth consecutive month to 46.5% (chart). The interest rate expectations differential, or the share of consumers expecting higher interest rates over the next year less the share expecting lower rates, fell to 13.2%, its lowest since August 2020. This amounts to a consumer that is, at least historically speaking, growing optimistic about the prospect of lower rates. Even as consumers have fared well in terms of real income and have been able to maintain a solid pace of spending over the past two years, higher rates have weighed on purchasing power. Higher rates on credit cards have chipped away at household balance sheets as nonmortgage interest expenses have risen, and the cost of financing held certain big ticket purchases out of reach for many households.

As expectations for lower rates begin to take hold for consumers, their buying plans look set to increase, particularly for larger purchases that require financing, such as autos and homes. Consumer plans to purchase a home in the next six months increased to 5.7% in September from 4.8% in August, likely reflecting the recent decline in mortgage rates over the past few months. All told, there is room for buying plans to increase and interest rate expectations to continue to decline in the months ahead, particularly given the September federal funds target rate cut is not reflected in this data, and we look for continued Fed easing in the months ahead.

Author

Wells Fargo Research Team

Wells Fargo