Conference Board Consumer Confidence January Preview: Mirror to the labor market

- Confidence predicted to rise slightly to 89 from 88.6.

- Consumer outlook has fallen from September's 101.3 pandemic high.

- Michigan Consumer Sentiment had faded since its October's top.

- Markets are focused on the federal stimulus package.

American consumers are waiting out the end of the pandemic and if they have not given up hope their caution reflects the deterioration of the labor market.

Consumer Confidence from the Conference Board is forecast to edge up to 89 in January from 88.6. Confidence has been eroding since reaching the pandemic high of 101.3 in September. Confidence was 132.6 in February.

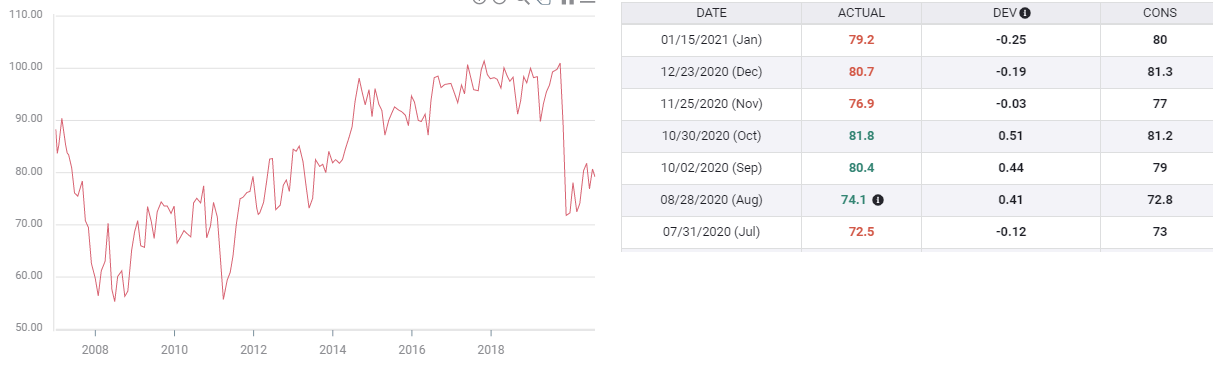

Michigan Survey

The Michigan Survey of Consumer Sentiment touched its pandemic high in October at 81.8, a half-year after plunging from 101 in February to 71.8 two months later in April. The Index slipped to 79.2 in January from December's 80.7.

Michigan Consumer Sentiment

FXStreet

US labor market

Initial Jobless claims began to rise in November when the middle part of the month averaged 767,500, sandwiched between two weeks at 713,500. At the end of the month the direction of claims was still undecided. Even with weekly totals for half the month increasing, the 740,500 average in November was still the seventh straight month of improvement and 58,000 better than October.

Initial Jobless Claims

The direction was determined in the next week when claims rose to 862,000 followed by 892,000, which was the highest seven-day total in two-and-a-half months. December's average of 837,000 was the highest in 12 weeks.

Nonfarm Payrolls reflected the deterioration in job markets brought on by the lockdown in California and various partial closures in a few other states like New York.

Payrolls dropped to 336,000 in November from an average of 660,500 in September and October. In December the market lost 140,000 positions, the first negative month since April and an large miss on the 71,000 forecast.

Claims have continued at a much higher pace in January averaging 870,000 for the three weeks tabulated through January 15 and are projected to be 878,000 on January 22 which will be released on Thursday.

With layoffs continuing this month at a higher level than December, the current 68,000 estimate for January payrolls, due on February 5, seems optimistic.

Retail Sales

Consumer spending has also mirrored of the changing fortunes of the job market. From July to September sales rose an average of 1.03% per month. In October that dipped to -0.1%. In the November and December holiday shopping months the average reversed to -1.05%.

Control Group Sales averaged 0.5% from July to September, -0.1% in October and -1.5% in November and December.

Conclusion

Consumer attitudes and spending have responded rationally to the reversal in the labor market. While equities can look ahead one or two quarters and price the future most consumers do not have that option. Even the promised stimulus packed form Washington will do little to raise consumers' outlook unless hiring picks up.

Markets will not move based on theses consumer figures, even though consuemr attitudes and consumption are paramount to the US economy, they will wait for the substance of payrolls.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.