Comfortably uncomfortable

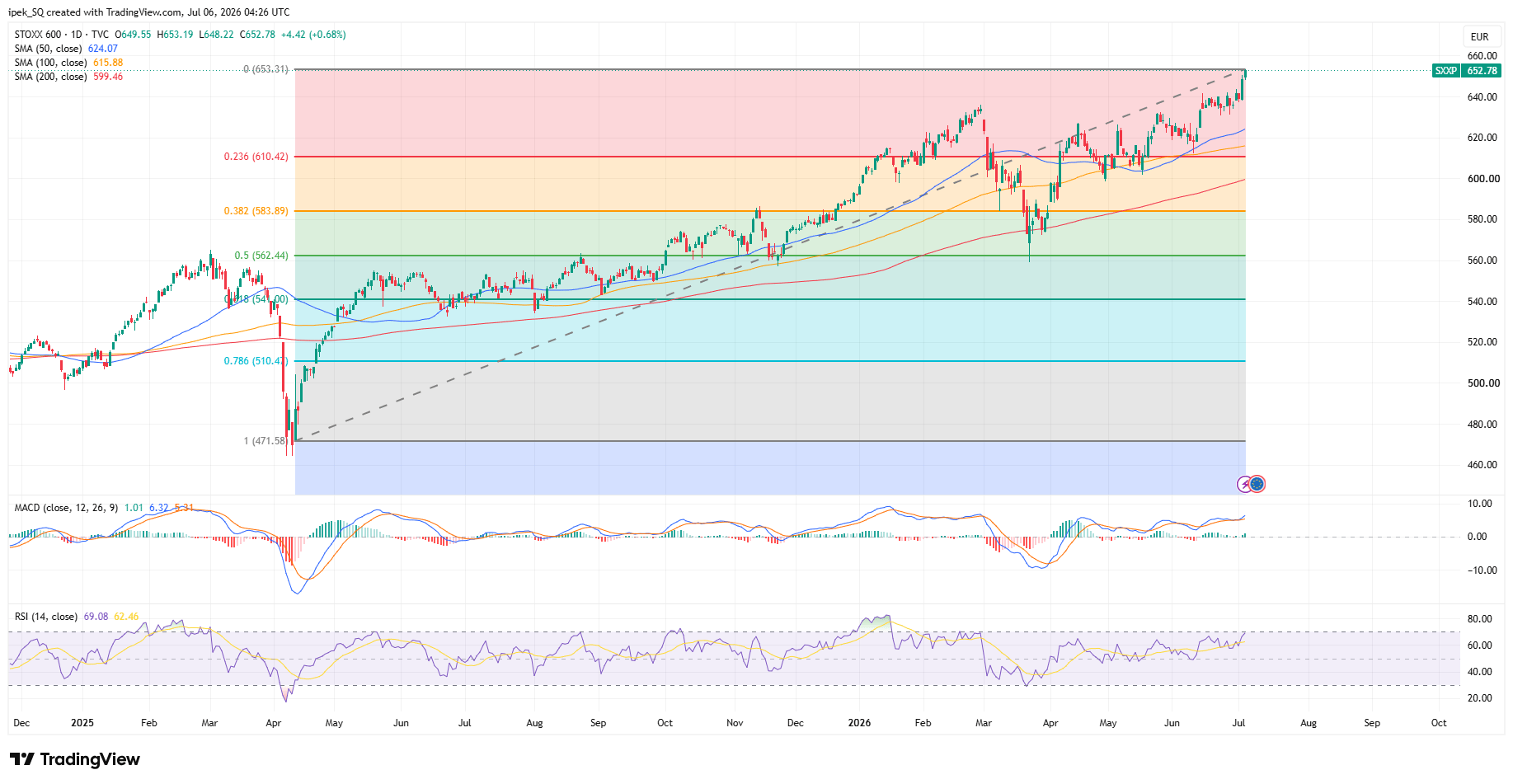

Last week ended on a positive note for European equities, as US markets were closed for the July 4th holiday. The Stoxx 600 advanced to a fresh record high despite a slight rebound in bond yields after Friday’s PMI data showed stronger-than-expected activity in June, especially in services, perhaps helped by sunny weather and the World Cup. The FTSE 100 is also approaching its own ATH levels – reached back in February – despite falling oil prices and downside pressure on mining stocks.

Speaking of oil, Friday’s data showed that several OPEC+ producers increased production, and the group also announced that it would raise output by 188K bpd, further unwinding the restriction strategy put in place back in 2023. The increase won’t materially change global supply, but it comes at a time when supply-glut talk is resurfacing, pulling oil prices lower (along with the Middle East de-escalation), and after the UAE quit OPEC, hinting at an upcoming battle for market share rather than cartel-boosted profits. US crude is consolidating near $68.50pb this morning, despite some jittery news in the Strait of Hormuz suggesting that some tankers made U-turns, but eventually crossed the Strait.

So, the new week starts on a mixed note. European futures are pointing to a cautious start, while tech-heavy US futures are leading gains before the European open, despite mixed sentiment toward tech in Asia. The Korean Kospi, for example, is slightly sold off – though recovering losses at the time of writing – after news that Samsung would increase the prices of its memory chips by another 20%. Remember, high triple-digit percentage rises in memory chip prices have started to squeeze profits at hardware makers, making the demand outlook cloudier for memory chip makers and investors anxious and undecided about whether the news is good or bad. Samsung initially jumped but gave back gains, and is up by around 0.80% at the time of writing. SK Hynix, which is preparing to list in the US this week to tap deeper US financing, starts the week more than 3% down. The company’s PE ratio is around 21.50, versus 21.90 for Micron. To me, and after a more than 1700% rise in a bit more than a year, I am curious to see how much juice the company can squeeze out of US markets at a time when bubble worries are getting louder and taming appetite.

Read the full article here.

Author

Ipek Ozkardeskaya

ipekScope

Ipek Ozkardeskaya began her financial career in 2010 in the structured products desk of the Swiss Banque Cantonale Vaudoise. She worked in HSBC Private Bank in Geneva in relation to high and ultra-high-net-worth clients.