Columbus Day? – The stock market is open

USD: Dec '24 is Up at 102.970.

Energies: Nov '24 Crude is Down at 73.90.

Financials: The Dec '24 30 Year T-Bond is Down 20 ticks and trading at 119.24.

Indices: The Dec '24 S&P 500 emini ES contract is 40 ticks Higher and trading at 5869.75.

Gold: The Dec'24 Gold contract is trading Down at 2671.20.

Initial conclusion

This is not a correlated market. The USD is Up and Crude is Down which is normal, but the 30 Year T-Bond is trading Lower. The Financials should always correlate with the US dollar such that if the dollar is Higher, then the bonds should follow and vice-versa. The S&P is Higher and Crude is trading Lower which is correlated. Gold is trading Lower which is correlated with the US dollar trading Up. I tend to believe that Gold has an inverse relationship with the US Dollar as when the US Dollar is down, Gold tends to rise in value and vice-versa. Think of it as a seesaw, when one is up the other should be down. I point this out to you to make you aware that when we don't have a correlated market, it means something is wrong. As traders you need to be aware of this and proceed with your eyes wide open. Asia is traded mainly Mixed. All of Europe is trading Mixed as well.

Possible challenges to traders

-

FOMC Member Kashkari Speaks at 9 AM EST. This is Major.

-

FOMC Member Waller Speaks at 3 PM EST. This is Major.

-

FOMC Member Kashkari Speaks at 5 PM EST. This is Major.

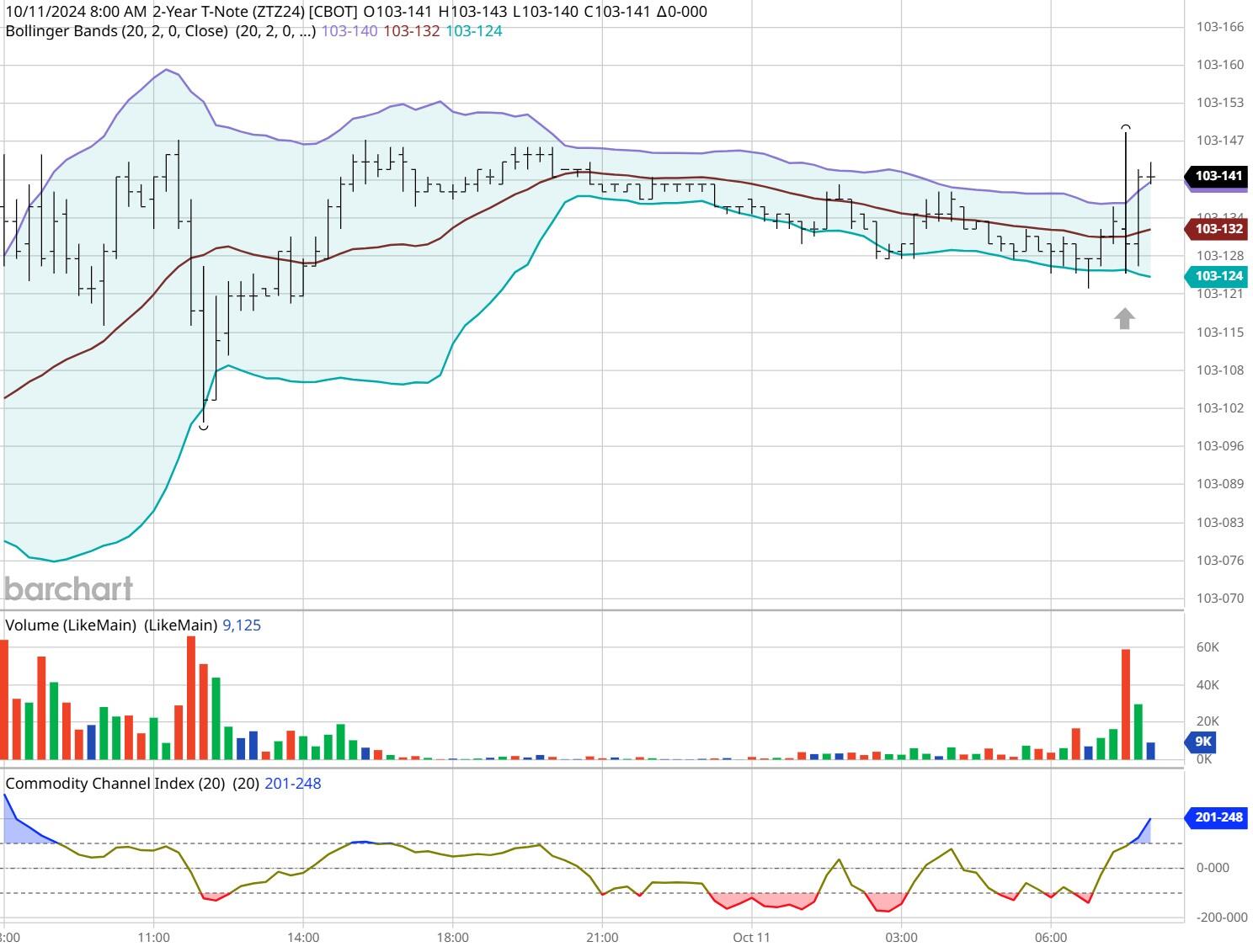

Traders, please note that we've changed the Bond instrument from the 10 year (ZN) to the 2 year (ZT). They work exactly the same.

We've elected to switch gears a bit and show correlation between the 2-year Treasury notes (ZT) and the S&P futures contract. The YM contract is the Dow Jones Industrial Average, and the purpose is to show reverse correlation between the two instruments. Remember it's likened to a seesaw, when up goes up the other should go down and vice versa.

On Friday the ZT migrated Higher at around 8:30 AM EST as the PPI numbers were being released and began its Upward Climb. Look at the charts below and you'll see a pattern for both assets. The Dow moved Lower at 8:30 AM and the ZT moved Higher at around the same time. These charts represent the newest version of Bar Charts, and I've changed the timeframe to a 15-minute chart to display better. This represented a Long opportunity on the 2-year note, as a trader you could have netted about 20 plus ticks per contract on this trade. Each tick is worth $7.625. Please note: the front month for ZT is Dec and the Dow is now Dec '24. I've changed the format to filled Candlesticks (not hollow) such that it may be more apparent and visible.

Charts courtesy of barcharts

ZT -Dec 2024 - 10/11/24

Dow - Dec 2024- 10/11/24

Bias

On Friday we gave the markets a Neutral or Mixed bias as we saw no evidence of Market Correlation Friday morning. The markets veered to the Upside on Friday as the Dow gained 410 points and the other indices gained ground as well. Today we aren't dealing with a correlated market, and our bias is to the Upside.

Could this change? Of Course. Remember anything can happen in a volatile market.

Commentary

So today is considered a bank holiday in the US but herein lies the dilemma. The stock market is open but the bond market isn't and that will make it very difficult to determine market correlation without the bond market open. We do have a couple of FOMC members speaking but that's about it in terms of economic news. Given that today is a bank holiday without the bond market, I would veer towards the Neutral or Mixed bias.

Author

Nick Mastrandrea

Market Tea Leaves

Nick Mastrandrea over 20 years experience in trading and formerly held a NASD Series 7. He currently holds a NJ Life, Health and Variable Authority. Nick is a published writer and his work has appeared in Futures Magazine, TraderPlanet and others.