Chinese inflation turned positive in June, but deflationary pressures remain

CPI inflation returned to positive year-on-year growth for the first time since January. On a month-on-month basis, though, downward price pressures persist.

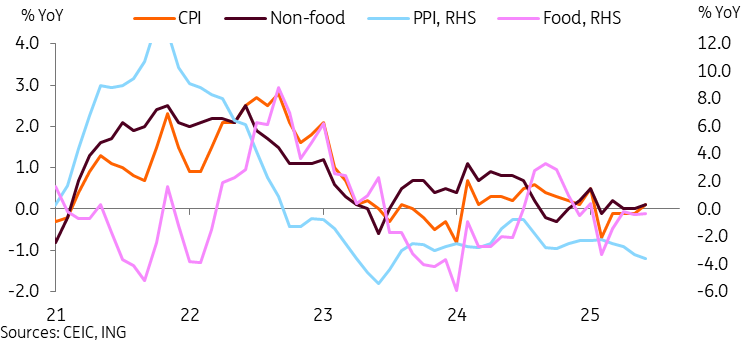

China's headline CPI snapped four-month streak of deflation

China's June consumer price index inflation returned to positive territory for the first time since January, rising to 0.1% year on year from -0.1% YoY in May, beating market expectations.

By subcategory, food remained in deflationary territory at -0.3% YoY, the fifth straight month of negative food prices. Most food products remained stuck in deflation, with the biggest drags from pork (-8.5%) and eggs (-7.7%). Exceptions include aquatic products (3.4%) and fruits (6.1%).

Non-food inflation fared better on the month with a 0.1% YoY rise, helping to offset the drag from food prices. Far and away the highest inflation belonged to the "other supplies and services" subcategory. It saw an 8.1% YoY gain, while most other non-food subcategories remained sluggish. While subcategories such as clothing (1.6%) and education, culture, and entertainment (1.0%) had decent YoY reads, the month-on-month readings for both were -0.1%, showing downward price pressures remain.

Producer price index inflation fell further into deflation, down to -3.6% YoY, which marked the 33rd straight month of falling prices and a 23-month low.

Headline CPI back to positive levels but food inflation and PPI still in deflation

Increased focus on stopping unhealthy price competition may take time to translate in inflation data

Through the first half of the year, China's CPI inflation remains slightly in deflation at -0.1% YoY, while PPI deflation is well entrenched at -2.8% YoY. Combined with the persistently negative GDP deflator, deflation remains a concern.

One of the main reasons is a contractionary cycle featuring heavy price competition as well as pay freezes and pay cuts. This will be a difficult challenge to tackle. Policymakers, though, recently shifted attention toward addressing the problem, with an eye on improving market exit mechanisms, encouraging consolidation and restructuring, and addressing non-market practices resulting in excessive price competition.

It's likely that aggressive efforts to stop these practices lead to some short-term pain for the labour market before things improve. We suspect that, given the external headwinds, a more gradual approach may be taken. While we will refrain from any forecast adjustments along this theme until there’s more clarity on policy execution, it’s nonetheless a worthwhile dynamic to monitor moving forward.

In the meantime, the relative strengthening of the CNY over the past few months and persistently soft inflation give the People’s Bank of China room to cut rates further later in the year, if needed. With activity data softening slightly in recent months, but not signalling a sense of immediate urgency, we currently expect the next rate cut to come in the fourth quarter.

Read the original analysis: Chinese inflation turned positive in June, but deflationary pressures remain

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.