China trade surplus beat forecasts amid resilient exports but sluggish imports

Exports remained well-supported by strength in autos and semiconductors, but imports slid amid modest demand in June.

Export growth continued to edge up in June

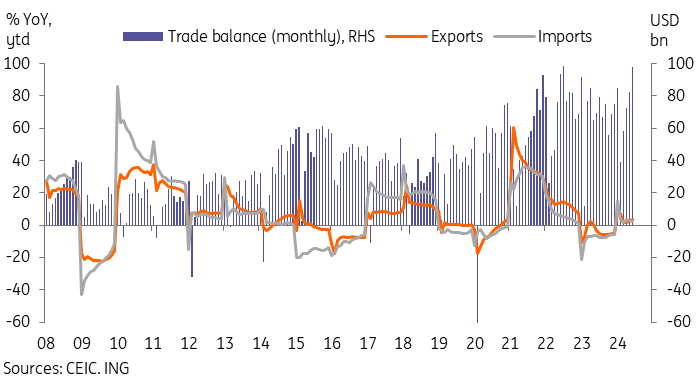

China's June exports grew by 8.6% year-on-year to USD 307.8bn, which came broadly in line with forecasts, a little lower than our house forecasts and a little higher than the consensus. Through the first half of 2024, China exports totalled USD 1.71tn, up 3.6% YoY, year-to-date. While the growth level does not appear too high at first glance, this has been stronger than most market participants were expecting at the start of the year.

In terms of product exports through 1H24, auto exports saw a strong performance of 18.9% YoY YTD. It is worth noting that auto export volume growth was higher at 25.3% YoY YTD; the disparity illustrates the price competition which has reduced export prices. There still could be some frontloading effect before auto tariffs from the EU and US come into play, but tariffs could lead to a slowdown in auto exports towards the end of the year. Household electronics also exhibited a similar trend, with solid value growth of 14.8% YoY YTD, but even faster volume growth of 24.9% YoY YTD.

Bucking the trend was semiconductor exports, which grew by 21.6% YoY YTD in terms of value, and a comparatively smaller 9.5% YoY Ytd in terms of volume. Strong semiconductor export growth shows that China's self-sufficiency push in tech and its pivot towards hi-tech manufacturing is starting to pay some dividends. China has been a major player in both the export and import of semiconductors as it gears up for the AI race.

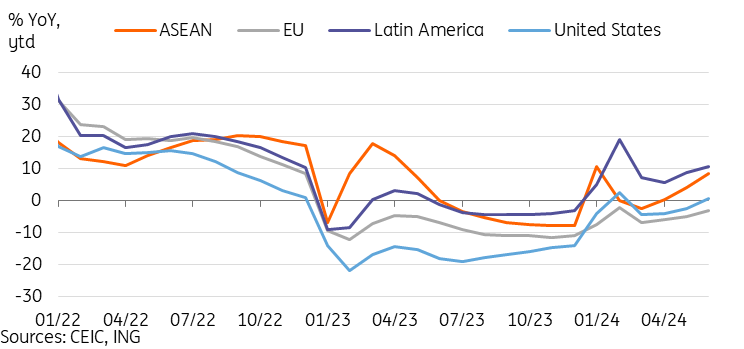

Looking at export destinations, exports to ASEAN continued to see strong growth of 10.7% YoY YTD, of which exports to Vietnam (22.5%) and Malaysia (12.6%) led the way. Exports and investment to Vietnam have benefited from the China + 1 theme. Exports to Latin America saw an even higher growth rate of 11.3% YoY YTD, with Brazil (24.4%) seeing rapid growth amid the EV boom, and accounting for over a third of exports to the region. Exports to key developed markets were comparably quite lacklustre, with exports to the US (1.5%), EU (-2.6%), Japan (-6.3%) and Korea (-3.7%) all a drag on export growth.

ASEAN and Latin America continued to drive export growth

Imports slowed to a four-month low amid sluggish demand

June's import growth returned to negative levels, down to -2.3% YoY to USD 208.8bn, which marked the lowest level since the Lunar New Year impacted February numbers, and coming in a little weaker than most forecasts which had been looking for low single-digit growth. Through 1H24, imports grew 2.0% YoY YTD to USD 1.27tn.

Import growth has been very much imbalanced in the year to date.

On the positive side, there has been strong demand for hi-tech imports (10.8%) amid the AI race. Semiconductor (10.8%), automatic data processing equipment and parts (53.7%), and LCD display panel (12.7%) imports all saw solid growth. China's strategic priorities will likely keep these import categories in strong growth mode moving forward.

On the negative side, the majority of other import categories have been in contraction in the year to date. Agricultural product imports (-10.3%) have been particularly weak, with sharp declines in soybean (-19.8%), vegetable oil (-34.1%), and grain (-16.4%) imports. The continued drag from the property market is also dragging down steel (-7.0%) and timber (-5.1%) imports. As China's domestic auto industry produces more competitive products, its auto imports (-13.9%) have also contracted sharply.

Trade balance beat expectations amid in line exports but disappointing imports

Trade balance beat expectations in June in a slight boost to 2Q24 GDP

The net impact of June's data of higher exports but slower imports has translated to a higher trade surplus of USD 99.1bn. China's trade surplus through the first half of the year was USD 434.9bn, which represents an increase from 2023's USD 400.7bn levels over the same period. As for 2Q24, the trade surplus settles at USD 252.6bn, up from USD 219.8bn.

More relevant for GDP is the RMB-denominated values, which totalled RMB 1.79tn in 2Q24 and RMB 1.51tn in 2Q23, indicating that net exports should remain a solid contributor to the 2Q24 GDP data out on 15 July.

Heading towards the second half of the year, incoming tariffs and moderating growth in other global economies could start to weigh on export growth, but a supportive base effect will likely keep YoY export levels in mid-high single digit growth for most months. We expect a smaller boost to growth from net exports in the second half of the year, though if imports continue to disappoint this contribution to GDP growth may remain solid in the coming quarters.

Read the original analysis: China trade surplus beat forecasts amid resilient exports but sluggish imports

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.