China demand miss meets US yield surge, lifting Dollar carry

Key takeaways

- China’s April activity data missed expectations; VXUS broke its rising trendline, showing pressure on non-U.S. equity exposure and supporting defensive USD demand.

- U.S. front-end yields are extending higher; US02Y near 4.10% keeps the dollar’s rate premium alive.

- USD/JPY has reclaimed 158.70; widening rate divergence is pushing carry back into focus.

- The fresh market test is whether global growth weakness can cap yields, or whether U.S. rate pressure continues to dominate FX.

Macro theme of May 18

Today’s fresh macro theme is global growth divergence. The new catalyst is weaker China activity data at the start of the week: April industrial output slowed to 4.1% year on year, retail sales rose only 0.2%, and fixed-asset investment unexpectedly contracted over the January-April period. That changes the market question. Traders are no longer only asking whether the Fed can hike; they are asking whether non-U.S. growth can absorb higher global yields. The transmission is clear: weaker China demand reduces confidence in global cyclicals, international equities lose momentum, U.S. yields remain high, and FX rotates back toward the dollar carry channel.

The “price of money” steering today is the U.S. 2-year yield near 4.10%. The attached charts confirm a clean divergence setup: US02Y is pressing toward a new extension zone, USD/JPY has recovered toward 159, and VXUS has broken below its April-May uptrend. This is a different market message from May 15. Then, the story was Fed hike optionality. Today, the story is that higher U.S. yields are starting to stress non-U.S. risk assets while still rewarding dollar exposure. For FX, that means broad USD support can continue if US02Y holds above 4.03% and international equities fail to reclaim trend support.

Macro catalysts that moved price

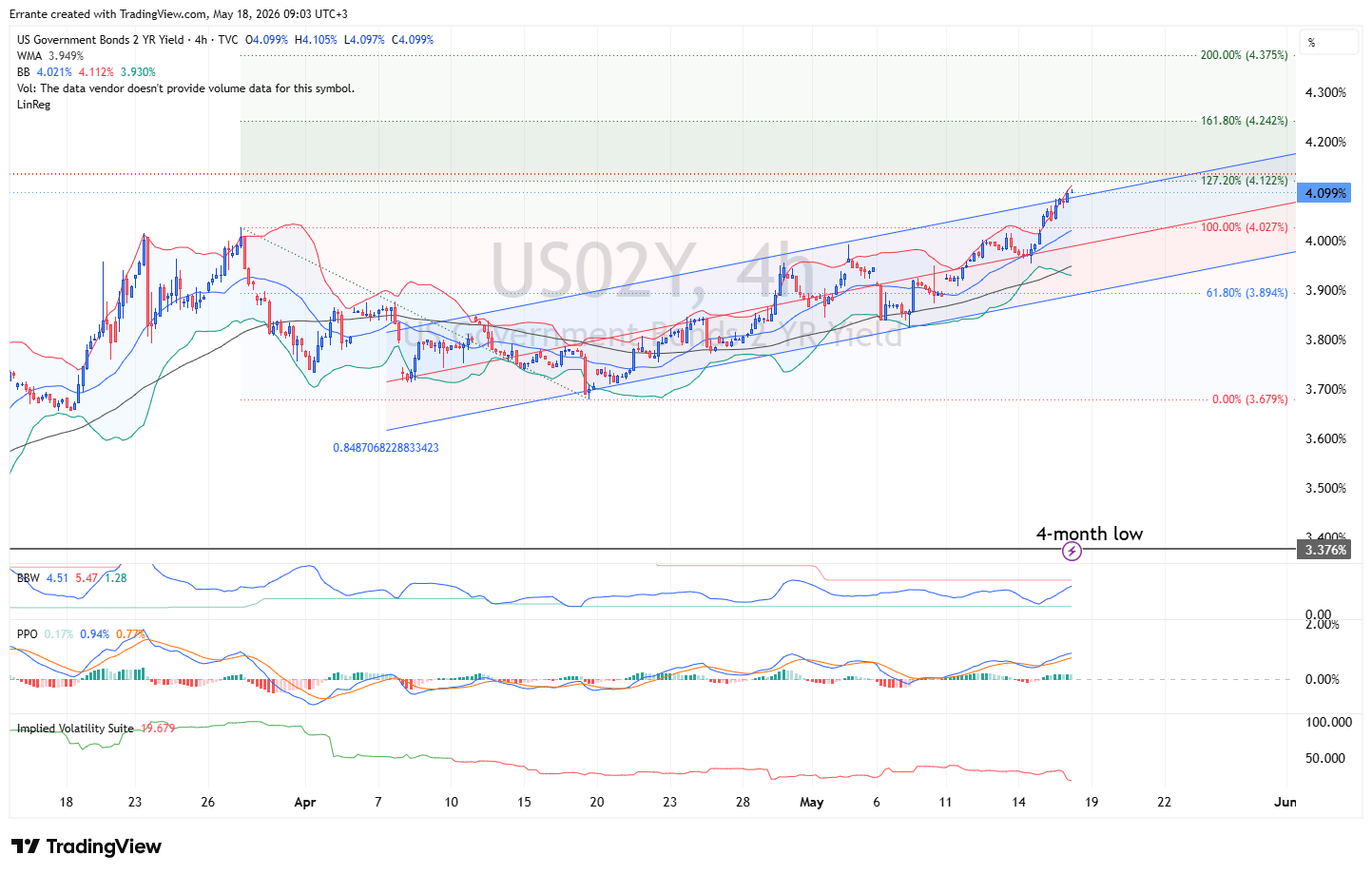

US 2-Year Yield four-hour

US02Y is the clearest expression of the policy-rate premium. The yield is trading near 4.103%, above the 100% extension at 4.027% and approaching the 127.2% extension at 4.122%. This move matters because weaker global data have not yet pulled U.S. front-end yields lower. Instead, the market is still pricing a restrictive Fed path.

Technically, the rising channel remains intact, price is above the 4-hour WMA near 3.95%, and PPO momentum is positive. A break above 4.122% would open 4.242% and 4.375%. Support is 4.027%, then 3.949% and 3.894%. FX consequence: as long as US02Y holds above 4.027%, the dollar keeps a yield advantage; a break below 3.894% would show that growth concerns are finally overpowering the rate story.

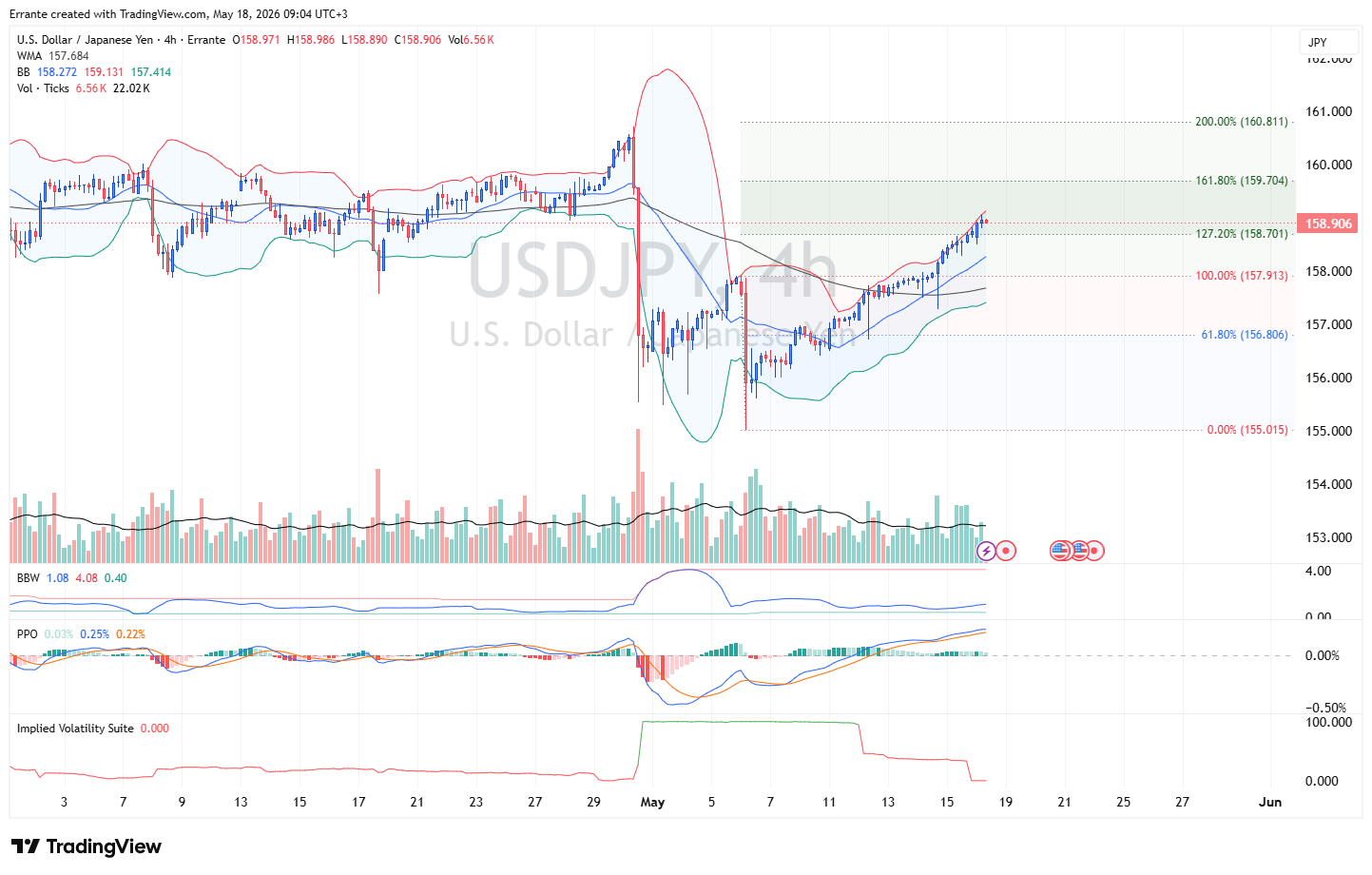

USD/JPY four-hour

USD/JPY is confirming the carry channel. The pair trades near 158.93 after clearing the 127.2% level at 158.70. This matters because higher U.S. front-end yields are again dominating the FX impulse, while Japan’s low-yield structure leaves the yen exposed to dollar-rate strength.

Technically, price is above the 4-hour WMA near 157.68 and close to the upper Bollinger band near 159.14. PPO remains positive, but the pair is approaching an important resistance cluster. A move above 159.70 would open 160.81. Support sits at 157.91, then 156.80 and 155.01. FX consequence: above 158.70, the market is still rewarding USD carry; below 157.91, the move would start to look overextended.

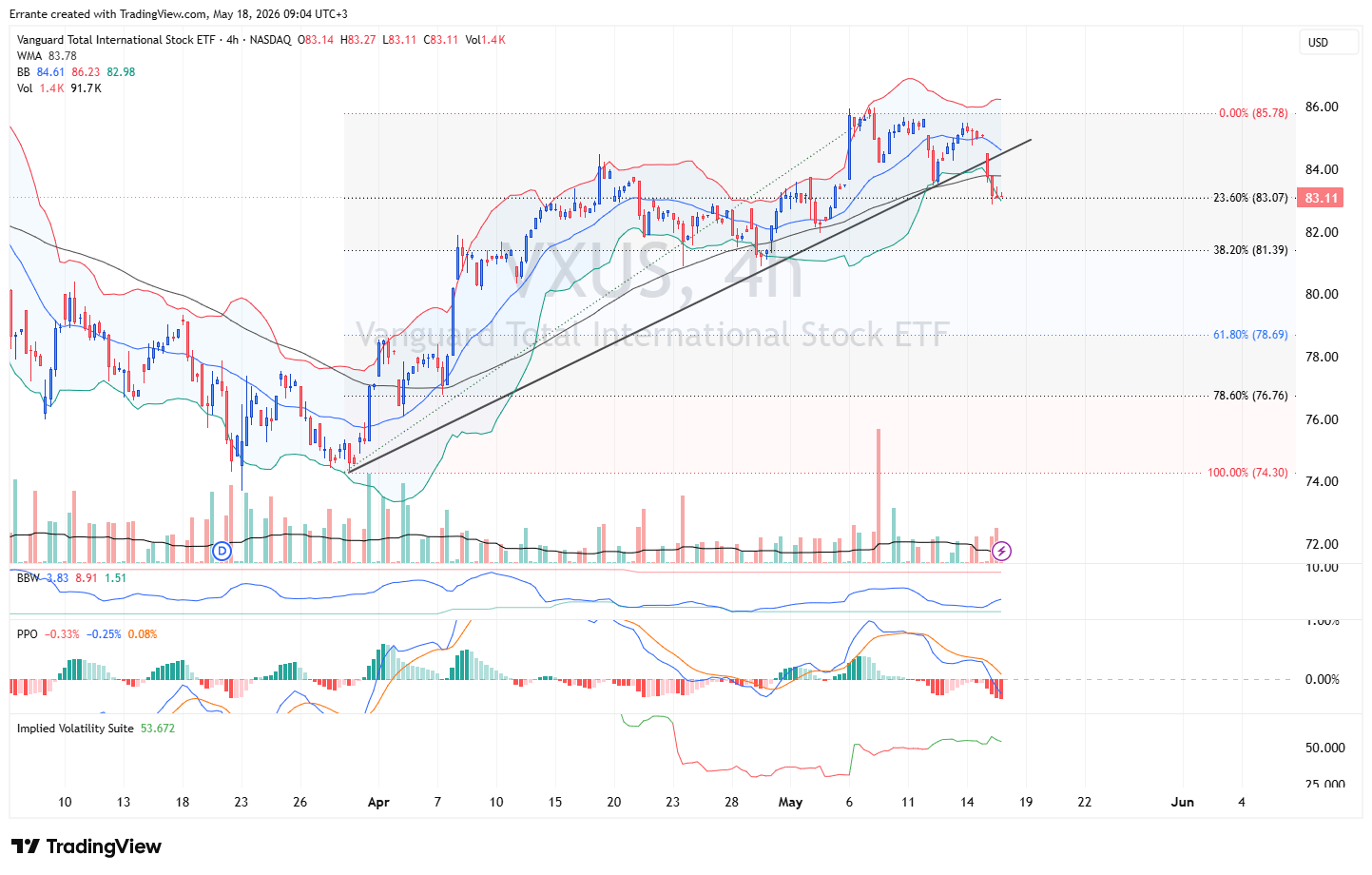

VXUS four-hour

VXUS is the key chart showing today’s non-U.S. growth stress. The ETF is trading near 83.11 after breaking below its rising trendline and falling under the 4-hour WMA near 83.78. This matters because weaker China data and higher global yields are pressuring international equity exposure at the same time.

Technically, price is sitting on the 23.6% retracement at 83.07. A break below this level would expose 81.39 and 78.69. Resistance is now 83.78, then 84.61 and 85.78. PPO has turned negative, and Bollinger bandwidth is rising, which shows the pullback has momentum behind it. FX consequence: a weak VXUS supports defensive USD demand and weighs on cyclical and Asia-sensitive FX.

Tactical market map

Base case: US02Y holds above 4.027%, USD/JPY stays above 158.70, and VXUS remains below 83.78. This keeps the dollar supported through rate divergence and weaker non-U.S. risk appetite.

Alternative case: growth concerns start to cap U.S. yields. US02Y falls below 4.027%, USD/JPY loses 157.91, and VXUS reclaims 83.78. That would weaken the dollar-carry theme.

Confirmation signals: US02Y above 4.122%, USD/JPY above 159.70, and VXUS below 83.07.

Invalidation signals: US02Y below 3.894%, USD/JPY below 157.91, and VXUS above 84.61.

Most important level to watch: US02Y 4.122%. Above it, the dollar-rate premium extends. Below 4.027%, the move becomes vulnerable to reversal.

Bottom line

The dominant theme is global growth divergence after weak China data met still-rising U.S. front-end yields. The clearest confirming chart is VXUS because it shows that international equities are no longer absorbing the rate shock smoothly. Into the next session, the broad FX consequence is continued USD support unless US02Y falls back below 4.027% and VXUS quickly recovers its broken trendline.

Author

Ali Mortazavi

Errante

BEc, CMSA, Member of IFTA - International Federation of Technical Analysis, Associate Member of STA - Society of Technical Analysis (UK).