Central Europe: Improving growth prospects in the short-term

In the first quarter, economic growth in Central European countries improved as expected (Poland: +0.4% q/q in Q1 2024; Hungary: +0.8% q/q; Czech Republic: +0.5% q/q; Slovakia: +0.7% q/q; Romania: +0.5%). Although details of the accounts are not yet available, there is strong evidence that growth was primarily driven by consumption, as reflected by the boost in retail sales. Private consumption has benefited from renewed household confidence, the rise in households’ purchasing intentions, sustained wages and lower inflation figures in recent months. Meanwhile, industrial production and business confidence remain rather subdued.

In the short term, the outlook for growth is well oriented. According to forecasts published by the European Commission last week, Romania and Poland could be among the best-performing economies in Central Europe, with a GDP growth of 3.3% and 2.8% expected on average respectively for 2024. A more modest rebound is expected in Hungary and Slovakia. In contrast, Czech Republic may still be lagging behind (forecasts: +1.2% this year).

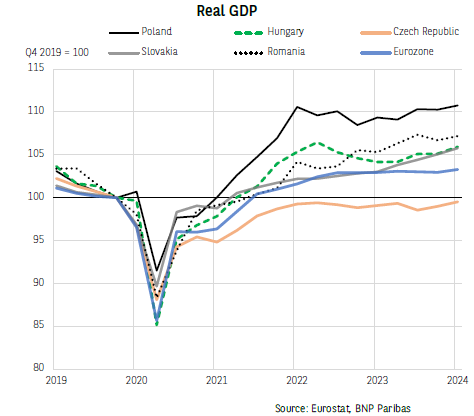

The Czech Republic’s economic underperformance is not limited to 2024. Czech GDP has still not returned to its pre-Covid-19 level, unlike that of neighbouring countries. Supply constraints have been a major obstacle to the country’s economic recovery. Similarly, savings accumulated by households during the pandemic were barely used afterwards. The household savings rate, close to 18% in Q1 2024, remains higher than in December 2019.

By contrast, Poland stands out in the region with a significant catch-up effect since 2020. GDP is currently 11% above its pre-pandemic level. While successive shocks since 2020 have constrained growth momentum, Poland has shown resilience due to generous government support measures. Investment has accelerated markedly (+11.6% after +3.4% in 2022), driven by foreign direct investment since 2021 (almost 5% of GDP on average each year). After narrowly escaping a recession in 2023, the expected revival in growth in 2024 should be supported by all growth drivers. Households should benefit from a significant increase in family allowances (+60% for child allowances) and an extension of the moratorium on debt servicing this year. In addition, the release of European funds, including a first tranche of EUR 6.3 billion already approved for Poland at the beginning of the year, will likely support investment.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.