Brexit gets a red card, and the Fed flattens its dots

Carl reports from London, where Brexit fever is rising.

While British politicians can’t figure out how they should stand in Europe, English Premier League clubs are much more confident of their positions. For the first time in a decade, four English football clubs have made it to the quarterfinal stages of the Champions League. On the pitch, at least, there is no rush to withdraw from Europe.

The U.K. parliament showed similar intentions last week, seeking a delayed departure from the European Union (EU). Early this morning, their European counterparts gave them just two more weeks to conclude an agreement. The cliff has moved, but it is still a cliff; Britain could still crash out of the EU without a deal.

It is disappointing that this tail risk remains so high. Efforts to define a new relationship between the U.K. and the EU have made little progress in the last two years. On one hand, delaying the deadline for a longer period would be a path of least resistance, but there is no guarantee that the extra time would produce a conclusive outcome.

Embattled Prime Minister Theresa May is still hoping to bring her Brexit plan to a third vote next week. In the unlikely event that it succeeds, Britain will depart in April. If it fails, a longer delay is possible, but the price set by the EU for the extra time will be a concrete outline of the way forward. Given the extreme dissonance here, assembling that outline may be a bridge too far.

Even if the additional extension is granted, substantial complications remain. Firstly, the delay would prolong the economic uncertainty that has led investment, talent and capital away from the U.K. Regardless of how the Brexit issue is resolved, those losses are likely permanent. The sooner something definitive can be reached, the better.

Several automakers recently announced plans to shift production away from the U.K., citing uncertainty over the country’s trade linkages to the rest of the world.

Secondly, a prolonged extension raises the uncomfortable possibility of the U.K. being forced to participate in elections for the European Parliament next May. This would be an awkward situation both sides would like to avoid.

Thirdly, The U.K. is obligated to continue paying membership dues to Brussels during the interim, which must rankle those who thought those funds might better be used elsewhere. The willingness of the EU to continue investing those funds in Britain might be compromised.

Fourth, it seems difficult to imagine that Ms. May would remain as prime minister over the length of a longer extension. A change of government, whether through a new Tory leader or a general election, would send negotiations with the EU virtually back to square one and could have severe consequences for the pound and U.K. equity markets.

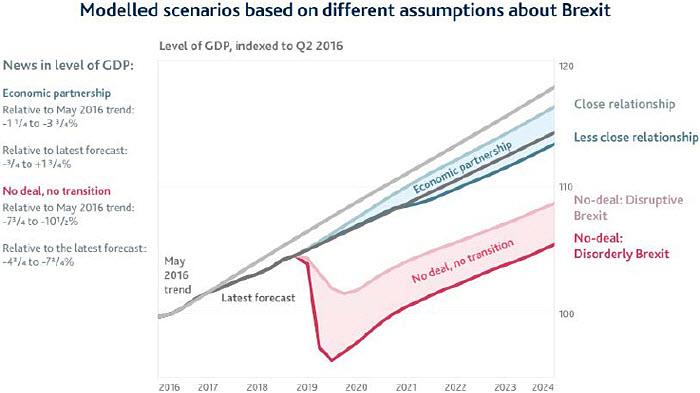

The politics of the situation are deep and thick. Those in favor of Brexit must sense their window of opportunity slipping away; the more time that passes, the more the public appreciates the terrible economic cost that Britain has borne. The Bank of England continues to simulate the possible outcomes (see below), with even the mildest of them producing a substantial long-term economic loss.

The politics of the situation are deep and thick. Those in favor of Brexit must sense their window of opportunity slipping away; the more time that passes, the more the public appreciates the terrible economic cost that Britain has borne. The Bank of England continues to simulate the possible outcomes (see below), with even the mildest of them producing a substantial long-term economic loss.

In light of this advancing evidence, backbenchers on both sides are looking for a softer Brexit and have nearly wrested control of the process from party leadership. Keeping track of the factionalism requires daily monitoring. By contrast, the Europeans have been firm and consistent. Their stance is borne of a desire to deter others who might contemplate separation, and the difficulty of negotiating with an opponent that doesn’t know what it wants. The remaining EU countries have been the beneficiaries of the migration of business, talent and capital, which will continue as long as the uncertainty persists. May continues to shuttle back and forth to Brussels, but has gotten little for her efforts.

EU leaders have struggled to suppress their exasperation with London. Donald Tusk, president of the European Council, has said that there is a “special place in hell” for the people who pushed for Brexit without a plan. French President Emmanuel Macron noted, “(T)his crisis is a British one. It’s now up to the British to end the ambiguities.” These statements do not suggest a lot of sympathy for the British plight, which makes the path to a longer extension more difficult.

One seemingly simple way to stop the madness would be a new referendum, but that would be fraught with uncertainty. There is no assurance it would produce a different result, and political wrangling over how to phrase the question for voters could take weeks. None of this would improve the reputation of the U.K. as a stable place to trade and do business.

Remarkably, the U.K. economy has been resilient to rising uncertainties. But things could change quickly from here, especially if the U.K. moves out without a deal. The vast majority of U.K. trade is conducted under EU, European Economic Area or preferential trade agreements and only a handful of “continuity” deals have been agreed so far, including with Norway and Iceland.

Businesses, particularly small-scale ones, are not ready for a sudden separation. Several questions remain unanswered: would “no deal” lead to cross-border trade tariffs? What regulatory or legal structure will the U.K. adopt? How much will it diverge from the European standards already in place? Will the taxation system change meaningfully? With no clarity on these topics, businesses are struggling in assessing risks, tax planning, diversification of investments and amending supply chains.

Businesses, particularly small-scale ones, are not ready for a sudden separation. Several questions remain unanswered: would “no deal” lead to cross-border trade tariffs? What regulatory or legal structure will the U.K. adopt? How much will it diverge from the European standards already in place? Will the taxation system change meaningfully? With no clarity on these topics, businesses are struggling in assessing risks, tax planning, diversification of investments and amending supply chains.

Forecasting is especially hazardous, but we still expect an agreement that largely preserves the existing provisions of business and finance. But our confidence is fading as more extreme scenarios gain likelihood. The next few weeks will be critical.

Winning the Champions League would be quite a prize for one of the English clubs. But a more valuable and lasting prize for England, Scotland, Wales, Northern Ireland and Europe would be a sensible Brexit deal. As we write today, a red card seems more likely.

Dot Matrix

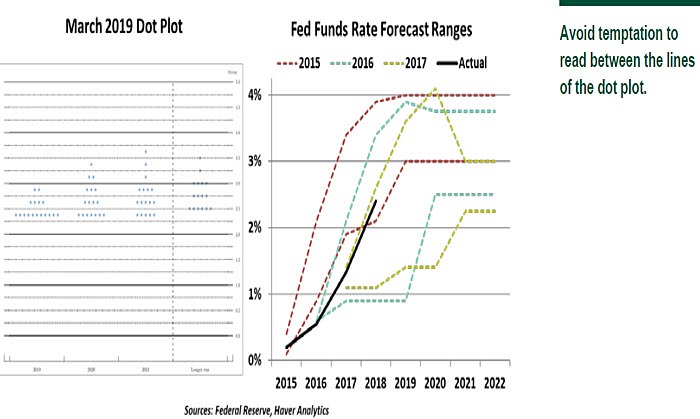

This week’s meeting of the U.S. Federal Open Market Committee yielded a quarterly update to its Summary of Economic Projections, including a chart known as the “dot plot.” This week’s dot plot was notable for a tight consensus and the change it represented from the last edition three months ago. The majority of FOMC participants do not recommend a rate increase in 2019; overnight U.S. interest rates may be unchanged for some time.

For all the attention this scatterplot receives, it is often misunderstood. Some background is essential to place it into proper perspective.

Publication of the dot plot began in 2012, as the Fed contemplated the end of accommodative, near-zero interest rates. The chart allows each Fed governor and regional reserve bank president to express his or her view of the outlook for the federal funds rate in the three years ahead.

The dots were intended to improve transparency and help markets understand the Fed’s thinking about the process of interest rate normalization. From the very beginning, markets have assumed that the median progression in the dot chart represents the Fed’s intended course. But this is something of a misinterpretation.

Each dot is conditioned on individual forecasts for the economy and the contributor’s monetary reaction function. Each of these can certainly vary across participants, and each might be misaligned with the consensus view.

Every regional reserve bank president gets to mark a dot, even those who do not currently have votes. (The voting powers of the regional banks vary each year on a set schedule.) A committee member who marks an outlier dot may have no influence on upcoming rate decisions. Unless the dots are closely clustered (which has been a rare occurrence), the chart does more to illustrate differences than clear direction.

In practice, the dot plot has not been the best predictor of actual outcomes. Recall that the current cycle of rate increases started in 2015, at which time, most FOMC members expected to maintain a steady cadence of rate hikes. The next increase, however, did not occur until the end of 2016, undershooting most estimates made in 2015. Since then, many Fed governors have forecasted a long-term rate of over 3% that now appears to be unattainable.

In our view, the chart is best understood as evidence of a committee having active discussions and diverse views. The dispersion in the dots can be informative, with a tighter grouping reflecting a greater degree of consensus. It is a rough guide of how individual members are thinking, not a summary or firm forecast of the Fed’s expectations.

Some have suggested that the Fed cease issuing the dot chart as part of a program to tighten communication. But we would miss the dot plot if it were retired. As long as the reader understands its limitations, the dot plot remains useful. As former Fed Vice Chairman Stanley Fischer summarized: “You can’t expect the Fed to spell out what it’s going to do. Why? Because it doesn’t know.”

Getting Schooled

It’s been a rough stretch for American higher education. Student debt has reached $1.5 trillion, and more than a million borrowers default on those loans every year. For the second year in a row, foreign enrollment in U.S. universities declined, as overseas students feel less welcome and more limited. And the evolving college admissions scandal has evoked an immense public response, and justifiably so.

It has also been suggested that college is getting less necessary, as an increasing fraction of those who earn bachelor’s degrees take first jobs that do not require a degree. Graduates who start their careers in this fashion take longer to reach their full potential. Policy makers in many locations are taking a hard look at apprenticeship systems as an alternative to the cost and time required to complete four years at a university.

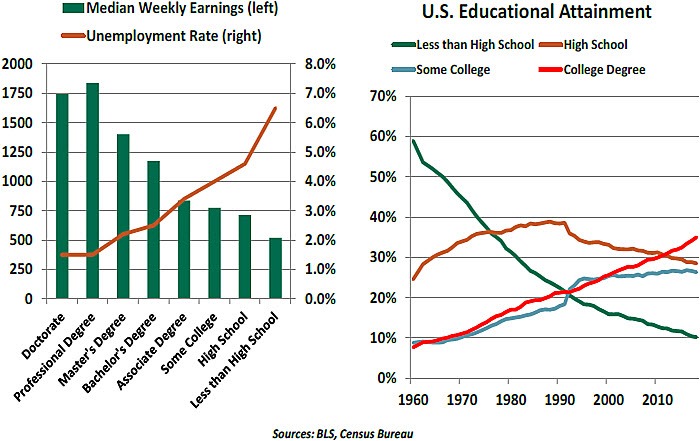

So why continue in school? Simple. The data still show, conclusively, that individuals with college degrees earn substantially more over their lifetimes. Workers change jobs or roles many times during their careers, and the broad background provided by a baccalaureate can position them to accept and adapt to new assignments. And it’s not just millennials who find themselves flitting about: a recent study from the Bureau of Labor Statistics found the average baby boomer held six jobs between the ages of 24 and 50.

Reducing attrition would be one way for students and society to gain more value from education. Almost 70% of U.S. students go to college, but fewer than half of those who do will eventually earn a degree. Those who drop out often carry the cost of the experience, but do not gain the benefit; this leaves them in an uncomfortable economic position. Additional academic support, for example, might help narrow the gap.

Reducing attrition would be one way for students and society to gain more value from education. Almost 70% of U.S. students go to college, but fewer than half of those who do will eventually earn a degree. Those who drop out often carry the cost of the experience, but do not gain the benefit; this leaves them in an uncomfortable economic position. Additional academic support, for example, might help narrow the gap.

The NCAA basketball tournament is underway, which will take people’s minds off rigged admissions. But after March madness ends, we should try to bring some common sense back to the issue of who should go to college. And we should find ways to help them finish what they start.

The U.K. parliament showed similar intentions last week, seeking a delayed departure from the European Union (EU). Early this morning, their European counterparts gave them just two more weeks to conclude an agreement. The cliff has moved, but it is still a cliff; Britain could still crash out of the EU without a deal.

It is disappointing that this tail risk remains so high. Efforts to define a new relationship between the U.K. and the EU have made little progress in the last two years. On one hand, delaying the deadline for a longer period would be a path of least resistance, but there is no guarantee that the extra time would produce a conclusive outcome.

Embattled Prime Minister Theresa May is still hoping to bring her Brexit plan to a third vote next week. In the unlikely event that it succeeds, Britain will depart in April. If it fails, a longer delay is possible, but the price set by the EU for the extra time will be a concrete outline of the way forward. Given the extreme dissonance here, assembling that outline may be a bridge too far.

Even if the additional extension is granted, substantial complications remain. Firstly, the delay would prolong the economic uncertainty that has led investment, talent and capital away from the U.K. Regardless of how the Brexit issue is resolved, those losses are likely permanent. The sooner something definitive can be reached, the better.

Several automakers recently announced plans to shift production away from the U.K., citing uncertainty over the country’s trade linkages to the rest of the world.

Secondly, a prolonged extension raises the uncomfortable possibility of the U.K. being forced to participate in elections for the European Parliament next May. This would be an awkward situation both sides would like to avoid.

Thirdly, The U.K. is obligated to continue paying membership dues to Brussels during the interim, which must rankle those who thought those funds might better be used elsewhere. The willingness of the EU to continue investing those funds in Britain might be compromised.

Fourth, it seems difficult to imagine that Ms. May would remain as prime minister over the length of a longer extension. A change of government, whether through a new Tory leader or a general election, would send negotiations with the EU virtually back to square one and could have severe consequences for the pound and U.K. equity markets.

In light of this advancing evidence, backbenchers on both sides are looking for a softer Brexit and have nearly wrested control of the process from party leadership. Keeping track of the factionalism requires daily monitoring. By contrast, the Europeans have been firm and consistent. Their stance is borne of a desire to deter others who might contemplate separation, and the difficulty of negotiating with an opponent that doesn’t know what it wants. The remaining EU countries have been the beneficiaries of the migration of business, talent and capital, which will continue as long as the uncertainty persists. May continues to shuttle back and forth to Brussels, but has gotten little for her efforts.

EU leaders have struggled to suppress their exasperation with London. Donald Tusk, president of the European Council, has said that there is a “special place in hell” for the people who pushed for Brexit without a plan. French President Emmanuel Macron noted, “(T)his crisis is a British one. It’s now up to the British to end the ambiguities.” These statements do not suggest a lot of sympathy for the British plight, which makes the path to a longer extension more difficult.

One seemingly simple way to stop the madness would be a new referendum, but that would be fraught with uncertainty. There is no assurance it would produce a different result, and political wrangling over how to phrase the question for voters could take weeks. None of this would improve the reputation of the U.K. as a stable place to trade and do business.

Remarkably, the U.K. economy has been resilient to rising uncertainties. But things could change quickly from here, especially if the U.K. moves out without a deal. The vast majority of U.K. trade is conducted under EU, European Economic Area or preferential trade agreements and only a handful of “continuity” deals have been agreed so far, including with Norway and Iceland.

Forecasting is especially hazardous, but we still expect an agreement that largely preserves the existing provisions of business and finance. But our confidence is fading as more extreme scenarios gain likelihood. The next few weeks will be critical.

Winning the Champions League would be quite a prize for one of the English clubs. But a more valuable and lasting prize for England, Scotland, Wales, Northern Ireland and Europe would be a sensible Brexit deal. As we write today, a red card seems more likely.

Dot Matrix

This week’s meeting of the U.S. Federal Open Market Committee yielded a quarterly update to its Summary of Economic Projections, including a chart known as the “dot plot.” This week’s dot plot was notable for a tight consensus and the change it represented from the last edition three months ago. The majority of FOMC participants do not recommend a rate increase in 2019; overnight U.S. interest rates may be unchanged for some time.

For all the attention this scatterplot receives, it is often misunderstood. Some background is essential to place it into proper perspective.

Publication of the dot plot began in 2012, as the Fed contemplated the end of accommodative, near-zero interest rates. The chart allows each Fed governor and regional reserve bank president to express his or her view of the outlook for the federal funds rate in the three years ahead.

The dots were intended to improve transparency and help markets understand the Fed’s thinking about the process of interest rate normalization. From the very beginning, markets have assumed that the median progression in the dot chart represents the Fed’s intended course. But this is something of a misinterpretation.

Each dot is conditioned on individual forecasts for the economy and the contributor’s monetary reaction function. Each of these can certainly vary across participants, and each might be misaligned with the consensus view.

Every regional reserve bank president gets to mark a dot, even those who do not currently have votes. (The voting powers of the regional banks vary each year on a set schedule.) A committee member who marks an outlier dot may have no influence on upcoming rate decisions. Unless the dots are closely clustered (which has been a rare occurrence), the chart does more to illustrate differences than clear direction.

In practice, the dot plot has not been the best predictor of actual outcomes. Recall that the current cycle of rate increases started in 2015, at which time, most FOMC members expected to maintain a steady cadence of rate hikes. The next increase, however, did not occur until the end of 2016, undershooting most estimates made in 2015. Since then, many Fed governors have forecasted a long-term rate of over 3% that now appears to be unattainable.

In our view, the chart is best understood as evidence of a committee having active discussions and diverse views. The dispersion in the dots can be informative, with a tighter grouping reflecting a greater degree of consensus. It is a rough guide of how individual members are thinking, not a summary or firm forecast of the Fed’s expectations.

Some have suggested that the Fed cease issuing the dot chart as part of a program to tighten communication. But we would miss the dot plot if it were retired. As long as the reader understands its limitations, the dot plot remains useful. As former Fed Vice Chairman Stanley Fischer summarized: “You can’t expect the Fed to spell out what it’s going to do. Why? Because it doesn’t know.”

Getting Schooled

It’s been a rough stretch for American higher education. Student debt has reached $1.5 trillion, and more than a million borrowers default on those loans every year. For the second year in a row, foreign enrollment in U.S. universities declined, as overseas students feel less welcome and more limited. And the evolving college admissions scandal has evoked an immense public response, and justifiably so.

It has also been suggested that college is getting less necessary, as an increasing fraction of those who earn bachelor’s degrees take first jobs that do not require a degree. Graduates who start their careers in this fashion take longer to reach their full potential. Policy makers in many locations are taking a hard look at apprenticeship systems as an alternative to the cost and time required to complete four years at a university.

So why continue in school? Simple. The data still show, conclusively, that individuals with college degrees earn substantially more over their lifetimes. Workers change jobs or roles many times during their careers, and the broad background provided by a baccalaureate can position them to accept and adapt to new assignments. And it’s not just millennials who find themselves flitting about: a recent study from the Bureau of Labor Statistics found the average baby boomer held six jobs between the ages of 24 and 50.

The NCAA basketball tournament is underway, which will take people’s minds off rigged admissions. But after March madness ends, we should try to bring some common sense back to the issue of who should go to college. And we should find ways to help them finish what they start.

Author

Northern Trust Economic Research Department

Northern Trust

More from Northern Trust Economic Research Department