BoE Interest Rate Decision Preview: The last 50 bps hike but not the end yet

- The Bank of England is set to raise rates by 50 bps in February from 3.50% to 4.0%.

- Sticky UK inflation and a resilient economy point to more BoE rate hikes in the offing.

- The vote split, forecasts and Governor Bailey’s press conference will steal the show.

- GBP/USD braces for massive volatility, awaiting the Fed and BoE double bonanza.

The Bank of England (BoE) is set to begin 2023 with yet another 50 basis points (bps) rate hike, with Governor Andrew Bailey hinting at further monetary policy tightening. The BoE will announce its interest rate decision at 12:00 GMT this ‘Super Thursday’, publishing the Minutes of the meeting and Monetary Policy Report (MPR) alongside.

BoE to signal more rate hikes

It seems like a crackling start to this year, as the Bank of England’s ‘Super Thursday’ follows the critical Federal Reserve policy meeting, the first of the central banks’ policy announcements of 2023. With a 50 bps rate hike widely expected, the BoE will raise its policy rate from 3.50% to 4.0% on February 2, marking the tenth consecutive hike after raising rates by a total of 325 bps in 2022.

The language in the central bank’s policy statement, the Minutes of the meetings and Governor Bailey’s presser could hint that the BoE will likely keep up interest rate increases, watering down expectations of the bank signaling a pause in its tightening cycle this month.

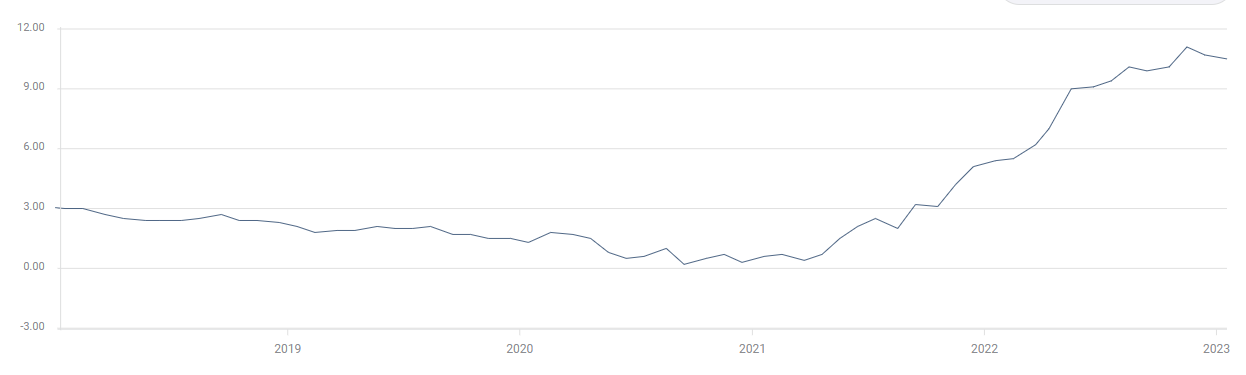

UK annualized inflation

Source: FXStreet

However, the latest UK business activity numbers for January have underscored the risk of the economy slipping into recession. The seasonally adjusted S&P Global/CIPS UK Manufacturing Purchasing Managers’ Index (PMI) unexpectedly improved to 46.7 in January but still remained in contraction territory. Meanwhile, the Preliminary UK Services Business Activity Index for January dropped sharply to 48.0 from December’s 49.9. Slowing consumer spending, with the UK Retail Sales down 1.0% MoM in December vs. -0.5% previous, also remains a cause for concern.

Vote split in focus again

Against this backdrop, attention will turn toward the vote split on the rate hike decision. At the December meeting, the BoE Monetary Policy Committee (MPC) members voted by a majority of 6-3 to increase the bank rate by 50 bps. Members Silvana Tenreyro and Swati Dhingra voted to keep the rates unchanged at 3.0% while Catherine Mann voted for a 75 bps lift-off to 3.75%.

This ‘Super Thursday’, we could once again see a divided vote count, as a majority of policymakers are expected to vote in favor of a 50 bps increase. Tenreyro and Dhingra may continue dissenting on rate hikes. A three-way split would not come as a surprise should a few of the members vote in favor of a 25 bps rate increase instead.

That said, the odds of the UK central bank signaling the end of its tightening cycle look unlikely as Bailey & Company could say that they have yet to see a sustained downtrend in inflation towards its 2.0% target. Economists polled by Reuters foresee one more rate rise to 4.25% in March while financial markets price in the rate hike cycle ending in the middle of this year at 4.50%.

Besides the hints in the policy statement and the vote split, traders will also closely scrutinize the Bank of England’s outlook on both inflation and wages, which will be key to reprice expectations on the central bank’s peak rate. The economic forecasts will continue showing a prolonged downturn through 2024. The International Monetary Fund (IMF), in its latest global economic outlook, said that the UK economy is the only nation in the G7 to shrink this year.

Trading GBP/USD with the BoE

The GBP/USD pair is keeping its corrective downside intact below the key 1.2450 resistance heading into the critical Fed and BoE interest rate decisions. The US central bank is widely expected to hike rates by 25 bps, with one more rate hike expected in March before the Fed puts a brake on its tightening cycle. Fed Chair Jerome Powell is likely to maintain his hawkish rhetoric, which could offer extra legs to the ongoing recovery in the US Dollar across its main rivals.

Thus, the US Dollar’s price action and persisting risk sentiment will significantly influence Cable’s reaction to the BoE policy announcements. In any case, the outcome is set to trigger two-way business for the GBP/USD pair in the coming days. Any knee-jerk move on the BoE rate hike decision could be quickly reversed, as investors slowly digest the underlying tone in the statement and the vote split. Governor Bailey’s words could also spur a fresh volatility wave around the currency pair.

A surprise 25 bps rate hike (personally I see a slim chance) could smash the Pound Sterling bulls, taking GBP/USD further south toward 1.2150. A split in the rate hike voting composition, with more MPC members favoring a 25 bps hike, will be also seen as an outright dovish move.

GBP/USD could resume its uptrend toward the 1.2450 barrier and beyond should the Bank of England deliver the expected 50 bps rate hike, with a relatively hawkish vote count and words suggesting further monetary policy tightening.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.