Australian Dollar Price Forecast: Short-term outlook remains constructive

- AUD/USD reverses part of its multi-day advance, coming close to 0.7100.

- The US Dollar picks up pace amid the resurgence of the flight-to-safety mood.

- Consumer Inflation Expectations rose to 5.2% in March, the Melbourne Institute said.

The Australian Dollar (AUD) remains firm amid elevated domestic inflation and the hawkish stance from the Reserve Bank of Australia (RBA). This combination maintains the door open for AUD/USD to go up even more, and it also helps to protect against occasional pullbacks. However, persistent global concerns are likely to restrain rallies from climbing too high for now.

The ongoing rally of the Australian Dollar appears to have met some resistance on Thursday, with AUD/USD leaving behind four straight days of gains and facing some downside pressure toward the 0.7100 region.

The pair’s daily correction comes on the back of extra gains in the US Dollar (USD), as market participants remain concerned over the fragile situation in the Middle East and its impact on the energy markets, particularly oil.

Australia: resilient backdrop keeps AUD supported

Australia’s macro backdrop continues to provide a fairly solid floor for the Australian currency.

Growth remains respectable, inflation is still proving sticky, and the RBA continues to lean on the hawkish side. For currency markets, that combination tends to keep a meaningful cushion under the AUD.

The latest data reinforce that narrative, as February’s final Purchasing Managers' Index (PMI) readings showed manufacturing at 51.0 and services at 52.2, both comfortably in expansion territory and broadly consistent with an economy that continues to grow at a steady pace.

Consumer activity is also holding up better than many had expected, with retail spending remaining resilient and the trade balance continuing to provide support, with the surplus reaching A$2.631 billion in January.

At a broader level, the economy is still expanding at a healthy rhythm: the Gross Domestic Product (GDP) expanded by 0.8% QoQ in the October-December period and 2.6% YoY, comfortably above the bank’s estimates.

The labour market is beginning to cool slightly, but there are still no signs of a sharp deterioration. Indeed, the Employment Change increased by 17.8K in January, while the Unemployment Rate held steady at 4.1%. In other words, the slowdown still appears gradual and orderly rather than abrupt.

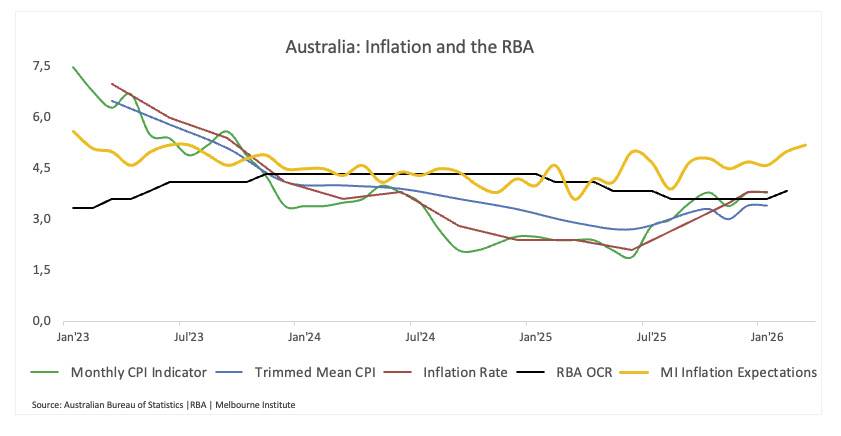

However, progress on inflation remains slow.

That said, RBA officials are still struggling with the current inflationary pressures.

That said, January’s headline Consumer Price Index (CPI) held at 3.8% YoY, slightly above expectations, while the Trimmed Mean measure edged higher to 3.4% YoY. The overall direction remains downward, but the pace of disinflation is proving slower than policymakers would ideally like.

From the RBA’s perspective, the job is clearly not finished yet. The central bank continues to expect inflation to peak around the second quarter of 2026 before gradually moving back towards the midpoint of the 2–3% target band by mid-2028.

Inflation expectations are also showing signs of persistence. The Melbourne Institute’s Consumer Inflation Expectations survey ticked up to 5.2% in March from 5.0% previously.

China: stabiliser rather than growth engine

China’s role in Australia’s economic outlook has also evolved.

Rather than acting as a powerful engine for global growth, the Chinese economy currently looks more like a stabilising force.

The headline figures suggest a reasonably robust growth trajectory at first blush. Indeed, China's GDP grew by 4.5% over the last twelve months in Q4 2025. Retail sales, too, saw a yearly rise of 0.9% in December, and trade data continued to show strength after the surplus reached $213.62 billion in the January–February period, with exports up 21.8% and imports up 19.8%.

Business surveys, however, offer a more nuanced picture. The official PMIs from the National Bureau of Statistics (NBS) remained in contraction territory in February, with manufacturing at 49.0 and services at 49.5.

Private surveys paint a somewhat stronger picture. The RatingDog indicators remained comfortably in expansion territory, with manufacturing at 52.1 and services at 56.7, both slightly higher than the previous month.

Inflation pressures remain subdued. The Consumer Price Index (CPI) rose just 0.2% YoY, while the Producer Price Index (PPI) remained in deflation at -1.4% YoY.

Meanwhile, the People’s Bank of China (PBoC) left the one-year and five-year Loan Prime Rate (LPR) unchanged at 3.00% and 3.50%, as widely expected.

For the Australian currency, the takeaway is relatively straightforward. China is no longer acting as a major drag on the outlook, but it is not yet providing a powerful growth impulse either.

RBA: policy remains firmly restrictive

For now, the RBA remains focused almost entirely on inflation dynamics.

Following the latest rate hike, Governor Michelle Bullock noted that financial markets have remained broadly orderly despite rising tensions in the Middle East. For Australia, the implications are mixed. As a net energy exporter, higher commodity prices can support national income, although a prolonged geopolitical shock could still weigh on household consumption.

Bullock also reiterated that inflation remains elevated and that the Board’s priority is to keep inflation expectations firmly anchored. Policymakers will therefore continue to assess incoming data carefully, with each meeting effectively remaining live.

She also acknowledged that if labour market tightness persists, the unemployment rate may need to rise somewhat to help bring inflation back under control.

Markets currently assign around a 71% probability of another 25 basis points rate hike at the March 17 meeting, while investors price just over 68 basis points of tightening by year-end.

Positioning: speculative longs continue to build

The latest Commodity Futures Trading Commission (CFTC) data for the week ending March 3 show speculative traders continuing to add to their bullish exposure to the AUD.

Non-commercial net long positions increased to around 67.8K contracts, marking a fresh multi-year high. This suggests speculators are still leaning into the trade rather than trimming exposure after the recent rally.

Market participation also increased, with open interest rising to roughly 262.3K contracts. That indicates the increase in net longs likely reflects fresh positioning entering the market rather than simple short covering.

Overall, speculative sentiment remains clearly constructive.

That said, with net long positions already at levels not seen in years, the market might be more susceptible to changes in the bigger picture. When a trade gets crowded, it often reacts swiftly when the underlying story starts to shift.

What’s in store for AUD/USD

Near term: AUD/USD will probably keep following the lead of the US Dollar and the wider geopolitical situation. Robust economic signals emanating from the United States, alterations in trade policy, or intensifying strife in the Middle East could rapidly alter market perceptions.

Risks: the AUD, known for its volatility, is inherently exposed to risk. It tends to struggle when global investors pull back, when China's economy shows signs of slowing, or when the US Dollar's standing suddenly changes.

Technical landscape

In the daily chart, AUD/USD trades at 0.7094. The near-term bias stays bullish as spot holds well above the rising 55-, 100- and 200-day Simple Moving Averages (SMAs), which cluster between 0.67 and 0.67 mid and reinforce an underlying uptrend. Price consolidates just above the 23.6% Fibonacci retracement at 0.6976, measured from the 0.6421 low to the 0.7147 high, suggesting shallow pullbacks within the broader advance. The Relative Strength Index (RSI) retreats toward 55 from overbought territory, indicating easing but still positive momentum, while the declining Average Directional Index (ADX) near 27 signals a maturing trend rather than fresh impulsive strength.

Immediate resistance emerges at the recent ceiling around 0.7158, with a break higher exposing the next resistance at 0.7283 and then 0.7661. On the downside, initial support aligns at the 23.6% retracement at 0.6976, followed by the horizontal level at 0.6897, which protects deeper losses toward 0.6784, the 50.0% retracement of the 0.6421–0.7147 rally. A sustained drop below 0.6897 would bring the 0.6660 and 0.6593 supports into focus, where proximity to the longer-term SMAs could attract dip-buying interest and maintain the broader bullish structure.

(The technical analysis of this story was written with the help of an AI tool.)

Bottom line: constructive bias, but conditional

For now, Australia’s relatively solid domestic fundamentals and a still-hawkish RBA should keep the broader bias for AUD/USD constructive.

That being the case, the Australian dollar's strength is still contingent. It usually shines when global risk appetite is robust. Should geopolitical strife escalate or market turbulence resurface, the US dollar might swiftly reassert itself, putting pressure on the currency pair.

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.