Australian Dollar Price Forecast: Bulls need (far) more faith

- AUD/USD adds to the recent pullback, revisiting the 0.7120 zone.

- The US Dollar alternates gains with losses amid ongoing geopolitical uncertainty.

- Australian inflation figures came in mixed in April, weighing on the Aussie.

The Aussie Dollar’s uptrend seems to have met some solid resistance in the 0.7270-0.7280 band so far, with AUD/USD still looking for a strong catalyst to attempt another move to the area of yearly peaks. In the meantime, the pair’s constructive outlook remains unchallenged for now, reinforced by still elevated domestic inflation and the RBA’s cautious approach.

The Australian Dollar (AUD) remains on the defensive for the second day in a row, sparking a deeper retracement in AUD/USD to the 0.7130-0.7120 band, or weekly troughs, on Wednesday.

Indeed, the pair’s marked decline comes in tandem with humble gains in the US Dollar (USD) in a context where uncertainty around the potential US-Iran peace talks is still running high.

Australia is still holding up, but cracks are beginning to appear

The Australian economy does look healthy and stable altogether, and honestly, in much better shape than many of its G10 peers.

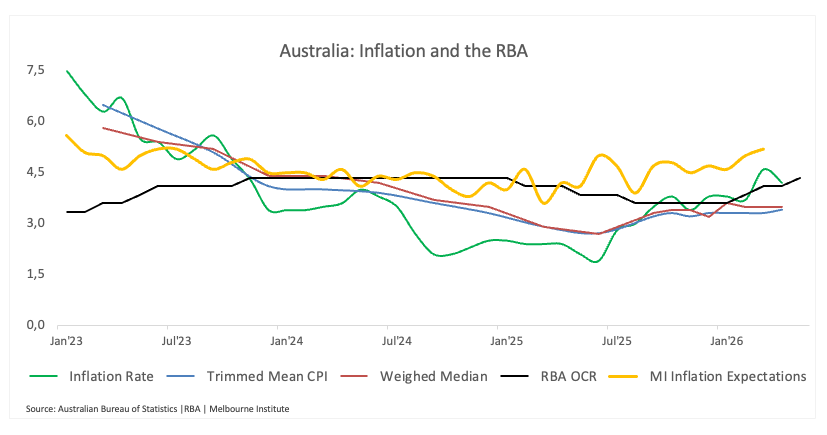

This performance appears underpinned by a solid domestic demand and pretty decent figures when it comes to economic growth.The spectre of a sticky inflation seems to justify the cautious and data-dependent stance from the Reserve Bank of Australia (RBA), particularly following the latest meeting, where it raised rates to 4.35%, broadly in line with market expectations.

Supporting the above, the flash data from the May Purchasing Managers’ Index (PMI) showed Manufacturing at 50.2 (from 51.3) and Services at 47.7 (from 50.7).

In the same vein, the latest trade balance figures showed an unexpected deficit of A$1.841 billion in March, markedly lower than the A$5.026 billion recorded in February. The Gross Domestic Product (GDP), meanwhile, showed the economy expanded by 0.8% QoQ and 2.6% YoY in late 2025.

On the not-so-bright side, the labour market has been cooling in the last couple of months. Indeed, the Unemployment Rate ticked higher to 4.5% in April (from 4.3%) and the Employment Change dropped by 18.6K individuals (from the revised 23.3K gain seen in the prior month).

Regarding inflation, April data saw the Consumer Price Index (CPI) come in at 4.2% from a year earlier (from 4.6%), the Trimmed Mean ticking higher to 3.4% (from 3.3%), and the Weighted Median holding steady at 3.5% over the last twelve months. All in all, a real sense of disinflation remains pale, although direction appears just about right. Somehow reinforcing that view, the latest Consumer Inflation Expectations eased to 5.6% in May (from 5.9%), according to the Melbourne Institute.

For the RBA, that means the job is far from done, as policymakers continue to signal that inflation may only return to target around mid-2028, keeping the focus firmly on patience rather than any imminent pivot.

China is stabilising the backdrop, but no longer driving growth

China now looks more like a stabilising force than the tailwind it usually was for the Australian economy.

Let’s see some numbers: the economy expanded by 5.0% YoY in Q1, Retail Sales gained 1.9% since the beginning of the year and a meagre 0.2% in a year to April. In addition, Industrial Production disappointed expectations in last month after expanding by 4.1% from a year earlier and 5.6% YTD.

Of note is the sharp reduction of the trade surplus, which narrowed to just over $51 billion in March from nearly $214 billion previously, all in response to weaker demand dynamics.

However, business activity seems to be regaining traction after the National Bureau of Statistics (NBS) reported Manufacturing PMI at 50.3 in April, while Services slipped into contraction territory at 49.4. At the same time, private gauges such as RatingDog still point to expansion, with Manufacturing climbing to 52.2 and Services up to 52.6.

The disinflationary pressure in China has been losing steam, as the CPI rose 1.2% YoY in April, while Producer Prices jumped by 2.8% YoY, moving further away from deflation.

And what about the People’s Bank of China (PBoC)? The central bank kept the Loan Prime Rates (LPR) unchanged at 3.00% for the one-year tenor and 3.50% for the five-year tenor at its latest event, matching the broad consensus.

To sum up, China is no longer pushing growth higher, but it is not dragging it down aggressively either. It is simply keeping things steady.

Inflation remains the RBA’s biggest headache

The Reserve Bank of Australia (RBA) matched expectations earlier this month, raising the Official Cash Rate (OCR) by 25 basis points to 4.35%, but the overall message was one of growing uncertainty.

The central bank now expects inflation to stay higher for longer, with the CPI returning to target only around 2027–2028, while growth slows and unemployment gradually rises. A big part of that shift comes from the oil shock linked to the Middle East conflict, which the RBA sees as both a drag on activity and a fresh source of inflation pressure.

Even so, policymakers do not believe demand has weakened enough yet, while businesses are increasingly expected to pass on higher costs.

Governor Michele Bullock struck a slightly calmer tone in the press conference, saying rates are now clearly restrictive and giving the bank room to “sit and see” how the situation evolves. Still, she made it clear that further tightening remains possible if higher energy costs start feeding into inflation expectations.

The Minutes reinforced the hawkish side of the story after policymakers appeared more concerned about persistent inflation than slowing growth, with some warning inflation expectations could become de-anchored if the RBA does not remain firm enough.

For markets, the broader message is that the RBA still looks far from dovish. Interest rates are likely to stay restrictive for longer, a backdrop that should continue to offer some support to the Australian currency, particularly if inflation remains sticky.

In the meantime, markets expect the RBA to keep its OCR unchanged at its June 16 gathering while pencilling in roughly 22 basis points of extra tightening by year-end.

AUD/USD pushes higher, but conviction still looks fragile

Base case

The pair has managed to refocus its attention to the key 0.7200 level, but it still feels heavily dependent on the broader backdrop. Without a sustained improvement in risk sentiment or continued US Dollar weakness, the move could start to lose traction.

Bull case

Further conviction is needed. If risk appetite picks up serious pace, spot could extend the uptrend and challenge the 2026 peak near 0.7280, just ahead of the minor 0.7300 barrier. Further up, the 2022 ceiling at 0.7593 awaits. Speculative positioning seems to be leaning toward this scenario.

Bear case

The loss of further momentum should not be ruled out in the current volatile context. If sentiment deteriorates, the Greenback picks up extra pace, or Chinese data keep disappointing, spot could recede further and dispute the key 0.7000 neighbourhood in the relatively short-term horizon.

The rally is there, although markets are still not fully convinced.

Speculators continue to favour the Aussie

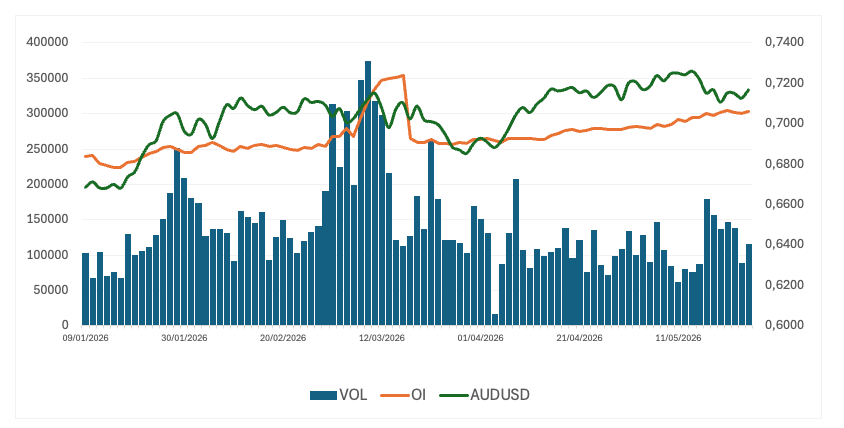

According to the latest Commodity Futures Trading Commission (CFTC) data, speculative net longs in the Australian Dollar increased for the second consecutive week, this time to levels last seen in January 2013 around 85.7K contracts for the week ending May 19.

The move also came in tandem with the fifth consecutive gain in open interest, which climbed to nearly 301.3K contracts.

It is worth recalling that speculators’ sentiment toward the Aussie shifted in late January following several years of being net short.

Despite the corrective move in the pair during that period, its prospect remains largely constructive, paving the way to further gains in the short-term horizon.

What could shape the AUD's next move?

In the near term, it is still all about the US Dollar, global risk sentiment, and geopolitics. Those remain the key drivers of price action. Next on tap on the Australian docket will be the key Private Capex data for the January-March period, out on Thursday.

Key risks include a sharper slowdown in China, a more aggressive Fed, a change of heart from investors when it comes to risk sentiment, or any shift in the RBA’s stance. Any of these could quickly destabilise the Australian currency in the near term.

Technical levels

In the daily chart, AUD/USD trades at 0.7137. The pair maintains a constructive near-term bias as it holds above the 55-day, 100-day and 200-day simple moving averages (SMAs), which cluster between roughly 0.70 and 0.71 and suggest underlying demand on dips. The Relative Strength Index (14) around 47 points to neutral momentum, while the subdued Average Directional Index (14) near 16 hints at a relatively weak trend phase rather than an impulsive move in either direction.

On the downside, initial support is seen at the horizontal level of 0.7079, reinforced by the nearby 55-day and 100-day SMAs around 0.71 and the 200-day SMA further down near 0.6807, ahead of more distant levels at 0.6833 and 0.6660. On the topside, immediate resistance is aligned at 0.7278, followed closely by 0.7283, while a sustained break above this band would expose the next key barrier at 0.7661.

(The technical analysis of this story was written with the help of an AI tool.)

Bottom line: supportive backdrop, uncertain momentum

The broader backdrop for the Australian Dollar remains supportive, and the RBA’s stance should continue to provide a degree of support on dips.

But this is still a currency that trades heavily on sentiment. When confidence is strong, the Aussie performs well. When uncertainty creeps in, the Greenback tends to take over.

So while the medium-term story still leans constructive, the near-term outlook feels less certain. The move higher is there, but conviction is not quite there yet.

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.