AUD/USD Price Forecast: Bearish momentum picks up pace

- AUD/USD weakened to new multi-week lows near 0.6450 on Wednesday.

- The US Dollar grabbed further upside impulse ahead of the FOMC event.

- Australian inflation readings eased across the board in the second quarter.

The Australian dollar found itself under renewed pressure on Wednesday, mirroring the weakness seen in other risk-sensitive currencies. In the face of a stronger US Dollar (USD), AUD/USD revisited the key contention zone around 0.6450, hitting new five-week troughs.

Mixed economic signals

Investors closely followed the release of Australia’s inflation figures, where the Inflation Rate rose by 0.7% QoQ in the April-June period and 2.1% on an annual basis. Still around inflation, the Monthly CPI Indicator came in at 1.9% in June, while the RBA’s Trimmed Mean came in at 0.6% QoQ and 2.7% YoY.

Additionally, July’s flash PMIs offered a glimmer of hope: the S&P Global’s manufacturing index climbed to 51.6 and services to 53.8, both firmly in expansion territory. However, the labour market presented a different picture, with only 2K new jobs created in June, an increase in unemployment to 4.3%, and a slight increase in participation to 67.1%.

RBA remains watchful

In early July, the Reserve Bank of Australia (RBA) surprised markets by pausing at a 3.85% cash rate. Governor Michele Bullock emphasised that the decision was based on "timing rather than direction," potentially leading to rate cuts if price pressures decrease.

The meeting Minutes reinforced this cautious optimism, and money markets are now pricing in roughly 75 basis points of easing over the next year—an August cut remains unlikely but far from impossible.

China’s uneven bounce

Australia’s biggest trading partner continues to rebound unevenly. Q2 GDP growth of 5.2% YoY and 7% industrial output contrast with underwhelming consumer spending, where retail sales remain stuck below 5%.

Beijing has opted for stability over stimulus, keeping its one- and five-year Loan Prime Rates (LPR) at 3.00% and 3.50%, respectively, earlier in the month.

Widening yield gap

In the meantime, the central banks’ divergence remains well in place and fuels the yield gap. The Federal Reserve (Fed) seems poised to keep rates higher for longer on the back of sticky inflation and looming tariff risks, while the RBA is flirting with the idea of interest rate cuts. Any shift in either narrative could quickly tip the scales and put the Aussie under extra pressure.

Speculators go (very) bearish

Contributing to the downside pressure on the AUD, non-commercial players have ramped up net short positions to roughly 81.2K contracts—their most pessimistic stance since April 2024—while open interest increased to a multi-week high near 161.4K contracts.

Technical levels in focus

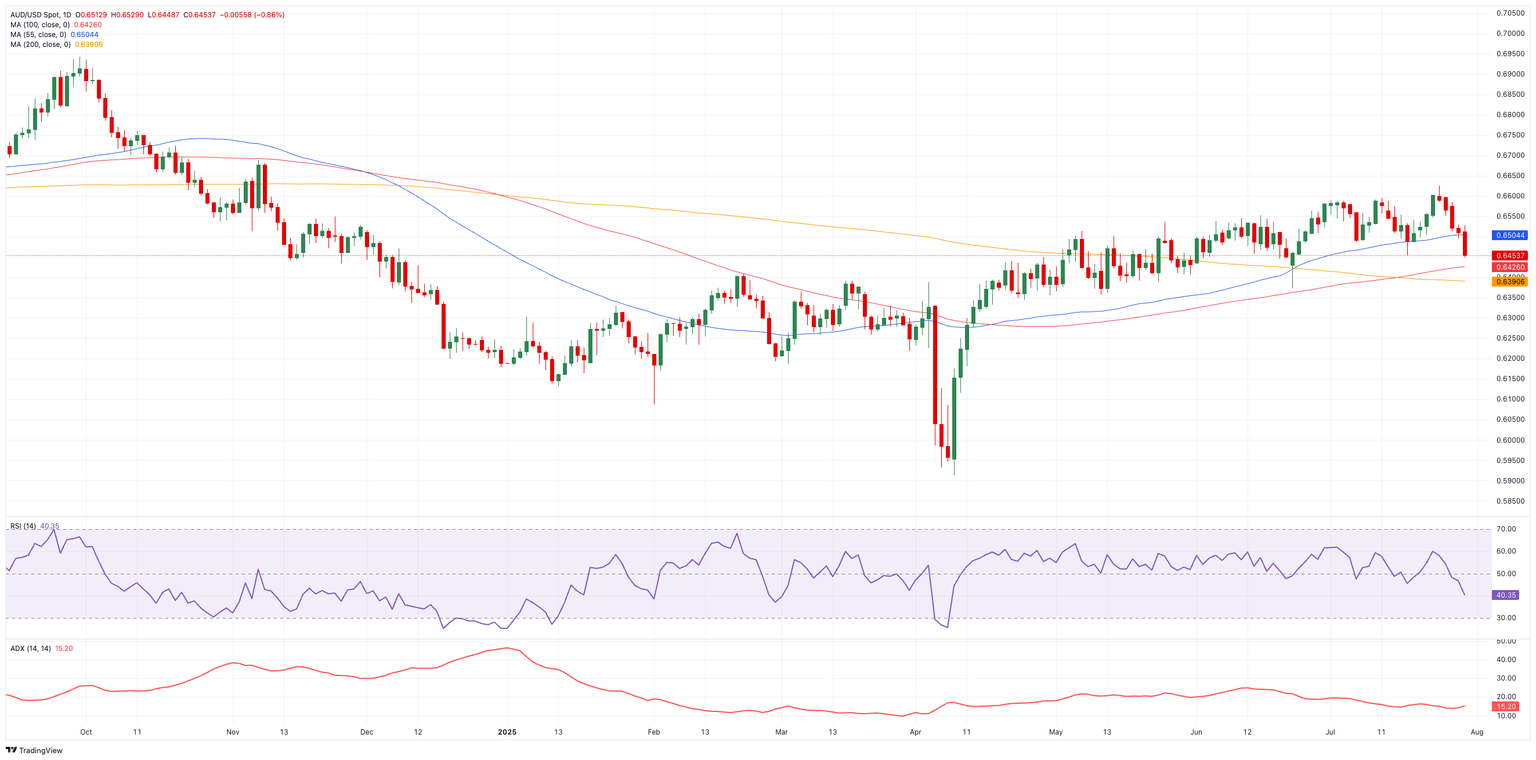

Immediate resistance for AUD/USD is eyed at 0.6625, the 2025 peak reached on July 24, with the November 2024 high of 0.6687 and the psychological 0.7000 mark looming just above.

On the downside, support begins at 0.6448, the July base (July 3), before giving way to the 200‑day SMA at 0.6393.

In addition, the Relative Strength Index (RSI) receded to nearly 40, pointing to growing bearish pressure, while the Average Directional Index (ADX) around 15 suggests the current trend lacks strong momentum.

What’s next for the Aussie?

Unless Beijing throws us a curveball or global trade suddenly goes haywire, the Aussie is likely to meander in a familiar range this summer. Traders will be scouring the horizon for a fresh spark—whether it’s a U‑turn from the Fed, a geopolitical flare‑up, or a change in tune from the RBA—to shake things loose.

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.