At the crossroads of abundance, scarcity, and disruption

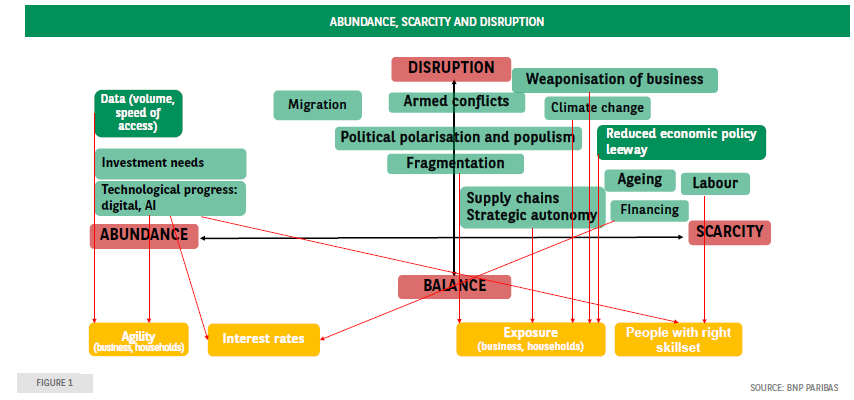

Over the past three and a half decades, the world has undergone profound change. From a situation of balance in the early 1990s -the peace dividend, the Great Moderation, globalisation- we have ended up in a world characterised by geopolitical, economic (supply side) and environmental disruption. A distinctive and fascinating characteristic of this new era is the coexistence of abundance (data generation and dissemination, investment needs) and scarcity (shortage of skilled staff given population ageing, difficulty in finding financing). These developments raise important questions. What is my exposure to climate risk, AI, increasing economic fragmentation and interest rate levels, as a business, an investor, an employee, a government? How exposed are my clients? How resilient are my business model and investment portfolio to unexpected shocks? How robust are public finances? In a world characterised by abundance, scarcity and disruption, exposure analysis under different scenarios will play a central role.

The summer break offers time to relax and try to disconnect from the daily news flow. It also provides an opportunity to take a step back and look beyond the traditional data we need to digest all year long. What are key longer-term trends? How may they influence my investment portfolio or my company? Where are the risks and uncertainties? A useful starting point is to go back in recent history and observe how much the world has evolved. At the risk of oversimplifying and being accused of selective amnesia, one can say that over the past three and a half decades, the world has evolved from balance to disruption. ‘Balance’ refers to the peace dividend in the early 1990s following the fall of the Berlin Wall and the Iron Curtain. That meant that financing capacity could be redirected to investments in technology and the provision of public goods.

It is also linked to the Great Moderation, an era starting in the mid- 1980s during which the variability of real GDP growth and inflation declined significantly1, although it should be noted that, judging by several crises –the 1987 crash of Wall Street, the Asian crisis of 1997, the collapse of the large Long Term Capital Management hedge fund in 1998, the bursting of the bubble in technology stocks in 2000, etc. – financial market instability increased. A third aspect of balance was the drive towards globalisation as exemplified by China joining the World Trade Organisation in 2001. Fast forward to the 2020s and balance has given way to ‘disruption’ in geopolitics and national politics in many countries, with polarisation2, and populism (Figure 1).

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.