Asian shares tumble as global growth fears mount

USDINR 77.65 ▼ 0.08%.

EUR/USD 1.0503 ▲ 0.35%.

GBP/USD 1.2388 ▲ 0.41%.

India 10-Year Bond Yield 7.339 ▼ 0.22%.

US 10-Year Bond Yield 2.913 ▲ 1.01%.

ADXY 102.78 ▲ 0.14%.

Brent Oil 110.78 ▲ 1.53%.

Gold 1,814.88 ▼ 0.06%.

NIFTY 50 15,949.50 ▼ 1.79%.

Global developments

The overall sentiment is that of risk aversion. High inflation and central bank tightening slowing down growth are making investors nervous.

Despite various Fed speakers including Fed Chair Powell saying that a 75bps hike is not the base case, markets are pricing in a 9% probability of a 0.75% hike in the June meeting.

Price action across assets

Risk aversion has triggered a flight to safety. US treasuries have rallied with a yield of 10y down to 2.90%. The dollar has strengthened across the board. Commodity currencies have been hammered down while the safe-haven Yen has strengthened. The pound has retraced almost 150 pips from yesterday's high. Euro too is back below 1.05 after printing a high of 1.0564 early in the Asia session yesterday. US equities saw the worst session since June'2020. The S&P500 dropped 4% while Nasdaq fell 4.7%. Asian equities too are seeing a meltdown and are down anywhere between 1.5-2%.

China lockdowns impeding supply chain recovery, slowdown risks spillovers, Yellen says.

Domestic developments

The minutes of the May meeting post which the MPC opted for an out-of-policy hike came out yesterday. They were extremely hawkish with members justifying the tightening by citing inflationary pressures. In fact, MPC member Jayant Verma was of the view that more than 100bps of rate increases needed to be carried out soon.

Rating Agency S&P has cut India's GDP growth forecast for FY'23 to 7.3% from 7.8%.

USD/INR

USD/INR ended at a record closing high and continues to get bought on dips. RBI intervention is ensuring that there is no runaway depreciation of the Rupee. Elevated crude prices and sell-off in equities continue to put the current account and capital account under pressure respectively. 1y forward yield ended 2bps higher at 3.67% yesterday.

Bonds and rates

The yield on the 10y benchmark ended almost flat at 7.35% yesterday. 1y T-bill cutoff came in at 5.92% yesterday. We may see a sell-off in bonds on account of the hawkish MPC minutes.

Equities

The Nifty gave up gains from earlier in the session to end 0.12% lower at 16240 yesterday.

Strategy

Exporters are advised to cover on upticks towards 77.90. Importers are suggested to cover on dips towards 76.50. The 3M range for USDINR is 75.50–78.30 and the 6M range is 75.00–78.90.

Japan's trade gap widens as import costs surge on supply pressures.

FX outlook of the day

USD/INR (Spot: 77.71)

The overall sentiment in the global market is that of risk aversion. High inflation and central bank tightening slowing down growth are making investors nervous. The dollar has strengthened across the board. The USDINR pair ended at a record-closing high and continues to get bought on dips. RBI intervention is ensuring that there is no runaway depreciation of the Rupee. Elevated crude prices and sell-off in equities continue to put the current account and capital account under pressure respectively. The minutes of the May meeting post which the MPC opted for an out-of-policy hike came out yesterday. We may see a sell-off in bonds on account of the hawkish MPC minutes. The pair is expected to trade within the range of 77.65-78 levels today.

EUR/USD (Spot: 1.0500)

Yesterday, EUR gave up its gain and settled a few pips below the 1.05 mark. After the release of eurozone CPI numbers which came in at 7.4% slightly lower than the expectation of 7.5%, the euro was facing pressure as investors have started believing that the inflationary pressures will persist longer due to supply chain issues and the Eastern European crisis. On the other hand, DXY has rebounded sharply amid an improved safe-haven appeal. There is no major data to be released today. The pair is expected to trade in the range of 1.0440 to 1.0540.

GBP/USD (Spot: 1.2380)

The pound remained under pressure on the back of downbeat headlines concerning Brexit and a broad risk-off sentiment. The European Union is considering a targeted trade war on troublesome Brexiteer MPs and Tory ministers, as the bloc war-gamed its response to Boris Johnson’s plan to override the Northern Ireland Protocol. Market participants will be looking forward to UK's industrial order data to be released today and Brexit-related headlines. The pair is expected to trade in the range of 1.2320-1.2420.

USD/JPY (Spot: 128.77)

The yen has strengthened against the greenback after the release of Japan's less negative GDP numbers on Wednesday. The annualized figure remains higher at -1% against the consensus of -1.8%. As per a report, two-thirds of Japanese firms say the BOJ should end large-scale stimulus by end-March 2023. The pair faced decent selling pressure on Wednesday despite a broader strength in the greenback. Tomorrow's CPI data of Japan can be a trigger point for further directional moves in the pair. The pair is expected to trade in the range of 128.20 to 129.10.

UK's Sunak to warn cost of living crisis won't be easy to fix.

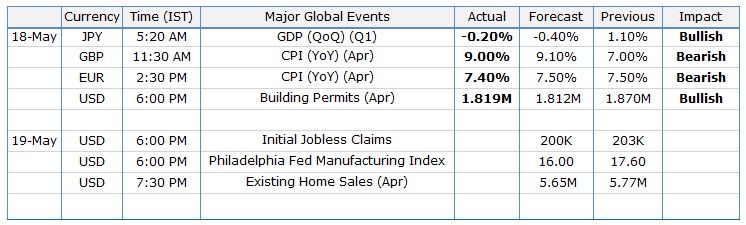

Economic calendar

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.