Asia open: TACO Thursday sends stocks and bonds into Orbit despite sticky inflation and an ECB hike

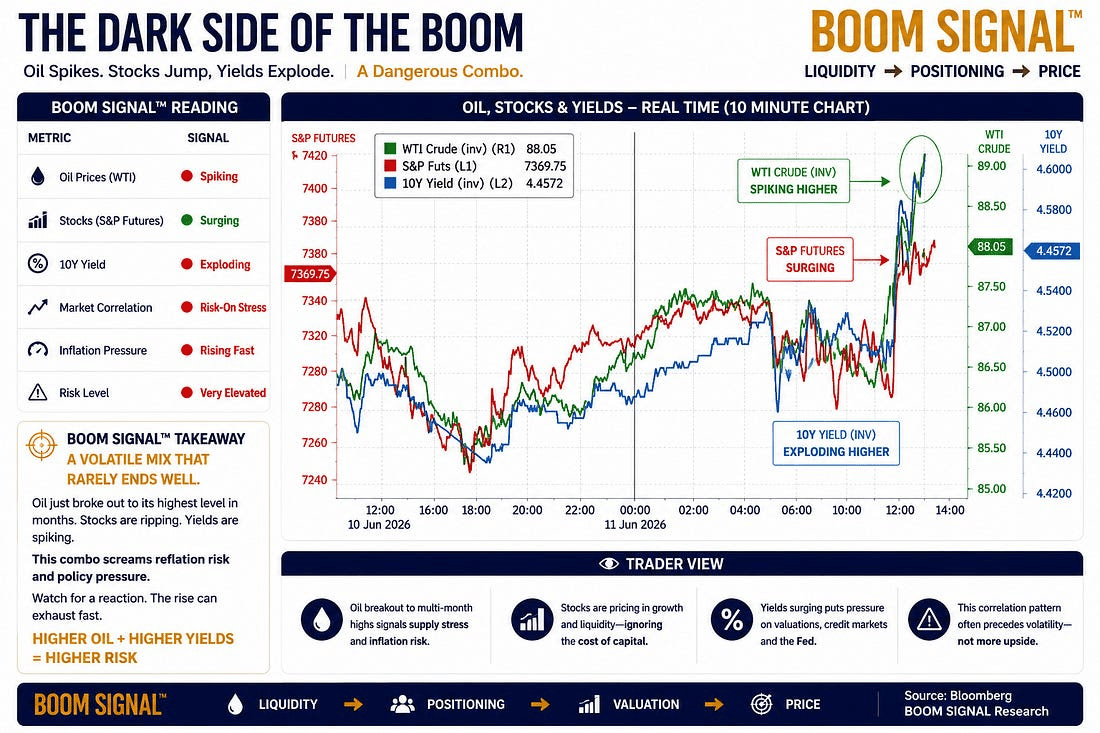

Takeaways by dark side of the boom

- Soft oil was the release valve. Once crude gave back war premium, yields fell and equities found room to rally.

- The Fed hike scare moved back, not away. Hot headline inflation still matters, but softer core data and lower energy risk changed the timing debate.

- Asia inherits a strong risk bid. Japan, Australia and Korea are trading the Wall Street squeeze, the oil unwind and the AI rebound in one package.

- SpaceX changed the mood music. The biggest IPO in history arrived just as traders were ready to reprice growth and semiconductors.

- The deal is still the line in the sand. A signed agreement can extend the move. A failed agreement can pull the relief premium straight back out.

- This is risk on, not risk free. The tape is higher for good reasons, but the stop loss still sits in the Gulf.

TACO Thursday

What a day. Markets came in braced for the full geopolitical siren, hot inflation embers, an ECB hike, and another oil shock, only to end the session trading as if someone had opened the pressure valve on the entire macro boiler room. The tape did not rally because the world suddenly became calm. It rallied because the worst near-term outcome was repriced in real time, and when crowded fear gets downgraded even slightly, the covering move can become violent.

This was TACO Thursday in its purest form. Donald Trump’s rhetoric flipped intraday from strike risk and hard military language toward no immediate attack, high-level diplomacy with Iran and talk of a deal being close enough to sign as soon as this weekend in Europe, with Vice President JD Vance expected to attend. That shift was the switch. Oil fell, yields dropped, equities surged, and the market shifted from bunker mode to chase mode in a single trading session.

Crude was the first pressure point to release. Brent slipped back toward the high $80s as traders pulled some war premium out of the barrel. That mattered because the current market is once again trading through the same oil, bond and equity triple gearbox.

Yet bonds are in a better place than stocks on the charts

Lower oil cools the inflation impulse. Cooler inflation expectations pull yields lower. Lower yields give duration equities breathing room. And when that happens after a period of heavy caution, the equity market does not walk higher. It gets dragged higher by forced repositioning.

That was the shape of the Wall Street move. Stocks were already bid earlier in the session, even while oil was still carrying geopolitical heat, but once the White House tone shifted toward diplomacy, the rally found another engine. The S&P 500 and Dow rose strongly, small caps and the Nasdaq led the charge, and the late-day giveback did little to change the message. The market had moved from protecting against escalation to paying up for de-escalation.

Tech was the loudest part of the tape. The Nasdaq 100 ripped higher, the Philadelphia Semiconductor Index surged close to 8%, and the AI complex roared back as if the market had decided the entire geopolitical shock was a temporary cloud over the same secular engine. Then SpaceX landed the kind of IPO headline that not only supports sentiment; it electrifies it. A $75 billion raise, the biggest IPO in history, arrived at exactly the moment traders were already leaning back into growth, semiconductors and the AI capital story. That was not just a headline. It was jet fuel for the risk narrative.

Asia now inherits that baton. Japan and Australia advanced, the broader regional index climbed sharply, and Korea’s Kospi, which has become the region’s high-beta AI mood ring, jumped by around 7%. That is not ordinary follow-through. That is Asia repricing the same three things at once: lower oil risk, lower rate pressure and renewed faith that the AI trade has not lost its sponsorship. When Wall Street semis rip, SpaceX breaks the IPO tape, and oil gives back war premium, Asia does not need much imagination to find a bid.

But this is where traders need to separate the trade from the truth. The market is cheering a possible path to peace, not a completed peace deal. There is still no signed treaty. Iranian channels have already pushed back against the idea that the agreement text has been fully approved. So the rally is real, but the foundation is still headline sensitive. If a deal is signed, risk can squeeze further because oil and volatility are still carrying conflict insurance. If the deal slips, stalls or gets denied, the market will have to mark back the relief premium it just front-loaded.

Treasuries understood the assignment immediately. The rates market moved from fully pricing a Fed hike by December toward pushing that risk into early 2027. That is a major psychological reset. Only a few hours earlier, traders were still dealing with hotter headline wholesale inflation and an ECB that had just raised rates for the first time since 2023. Under normal conditions, that combination should have leaned hard against risk. But this was not a normal conditions tape. Oil de escalation overpowered the inflation headline.

The inflation detail gave bonds enough cover to rally. Headline producer prices were hotter than expected, but core prices excluding food and energy were softer than feared. That allowed rate traders to argue that the worst inflation impulse may be passing through the system rather than embedding more deeply. In market terms, the headline number made noise, but the core detail cooled things off. That was enough to move the Fed conversation away from immediate tightening fear and back toward patience.

The ECB hike was important, but it did not control the global tape. The first rate increase since 2023 should have reminded markets that central banks are not ready to declare victory. Instead, the oil drop and the softer core inflation detail stole the steering wheel. The message from bonds was clear. Energy is still the swing variable. If crude keeps cooling, the market can look through central bank discomfort. If crude spikes again, the rate trap snaps back into focus.

Gold and bitcoin added another layer to the story. Gold pushed above $4,210 an ounce, bitcoin rallied, and the dollar was choppy as the first relief impulse knocked it lower before it later steadied against G10 peers. That mix tells me this was not a simple risk-on rally. It was a market buying relief, liquidity, optionality and insurance at the same time.

The bigger equity message is that investors are desperate to get back to earnings and AI the moment the geopolitical smoke thins. The market wants to believe the Middle East shock can be contained before it feeds into energy prices, inflation expectations, Fed pricing and corporate margins. That is why the rally was so powerful. It was not just about hopes for peace. It was about removing the one obstacle preventing traders from returning to the growth story they already wanted to own.

For Asia Open, the path of least resistance is higher as long as oil stays soft, yields stay contained, and the diplomatic script remains alive. But this is still a market trading on a possible signature, not an actual one. The risk has shifted from panic selling to relief chasing, and that is a different kind of danger. Traders can ride the move, but they cannot forget what lit it. One confirmed deal could unlock another leg higher. One denial could turn the same positions into trapped inventory.

So yes, TACO Thursday delivered the full market reversal package. Oil lower, yields lower, stocks higher, semis roaring, SpaceX lighting the IPO fuse, gold firm, bitcoin bid and the Fed hike scare pushed further out on the calendar. But the cleanest read is this: the market did not price peace. It priced the possibility that the worst case has been delayed. That is enough for a rally. It is not enough for complacency.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.