ASA Letter to Shareholders: “More Dynamic Portfolio”

In 2019, the gold price increased as global uncertainty led to lower global interest rates, in part driven by trade tensions and concerns of a potential recession. The move earlier in the year by the Federal Reserve (the "Fed") to a more dovish stance propelled gold higher in the middle of the year, as they cut rates three times. Gold peaked at $1,552 in September of 2019 from a low of $1,221 at the end of November 2018, an increase of over $300, one of the largest intra-year increases we have seen since the post financial crisis gains in 2010-11.

Established in 1958, ASA Gold and Precious Metals Limited is a closed-end precious metals and mining fund (NYSE: ASA) registered with the United States Securities and Exchange Commission and domiciled in Bermuda. The Company is one of the oldest investment management firms focused on the precious metals and mining industry. Gold increased 20.0% during the fiscal year ended November 30, 2019, while ASA Gold and Precious Metals Limited ("ASA" or the "Company") reported a total return of 47.0% based on its net asset value ("NAV"), compared to a total return of 43.0% for the FTSE Gold Mines Total Return Index (the "Index"). Total return of ASA's share price for the fiscal year was 41.1%. At fiscal year-end, total net assets of ASA were $286 million, an increase of $91 million as compared to fiscal year-end 2018.

The Company's average expense ratio rose to 1.38% during the 2019 fiscal year from 1.35% during fiscal year 2018 due primarily to higher operating costs associated with the transition from internal management to Merk Investments (the "Adviser" or "Merk") as external adviser, which saw severance payments to the departing management team and elevated legal costs. Together with the Board, we worked hard to keep these transition costs low to the extent possible. If assets remain relatively constant and no unforeseen expenses arise, we expect the expense ratio to drop in the coming fiscal year.

Separately, investment income increased to $2.4 millionduring fiscal year 2019 from $1.6 million during 2018, generated by increased dividends from portfolio investments.

The discount at which ASA's shares traded in the market fluctuated during the year from a high of 17.8% to a low of 13.6% and ended the fiscal year at 17.7%. The Board of Directors of ASA and Merk monitor the Company's share price and discount to NAV on an ongoing basis. Part of the higher discount might be a result of good performance, with market participants taking their time to evaluate whether the improved absolute and relative performance is a fluke or may be due to a robust investment process (outperformance leads to a greater discount if the NAV increases faster than the share price). At Merk, we have launched several initiatives which we hope will help address the discount over time, including:

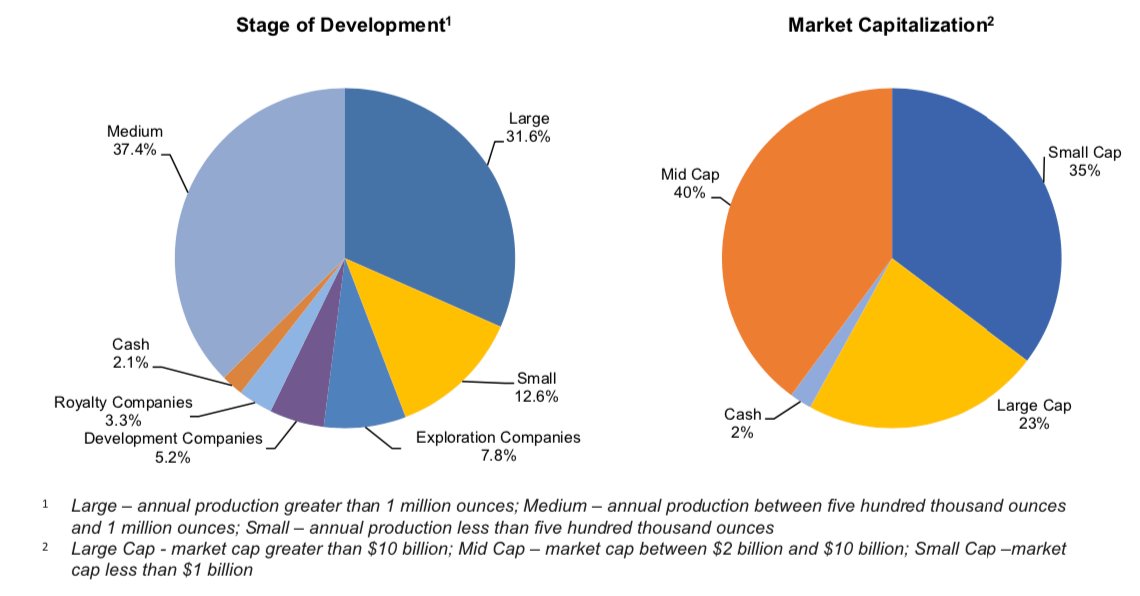

First and foremost, we will continue to focus on execution of our investment process as to achieve ASA's investment objective. ASA's portfolio has become more dynamic as we have reduced large cap and royalty companies, increasing investments in mid-cap, development and exploration firms. ASA has also helped finance several mining companies, usually at a discount to prevailing market prices, and sometimes taking warrants and similar interests along with the equity investments. Unlike in other industries, such dilutions to shareholders are often taken as a positive, as the injection of capital provides much needed resources for the development or exploration company's next phase of growth, bolstering the respective balance sheet. Merk looks for companies that have other strong backers that may be available to inject additional capital down the road as the need may arise. While any such investments tend to be small relative to the fund's assets, we believe they have the potential to deliver positive returns over time.

Second, we have worked hard to increase public awareness about ASA, in several ways

-

Merk has significantly increased communications about ASA and our portfolio management, including holding webinars to explain our investment process in more detail and giving interviews to industry associations. We invite you to for replays.

-

We invite anyone to reach out to us with questions about ASA and our investment process. We have spoken to many shareholders over the past year and would like to encourage anyone who has not spoken to us to send us a note to schedule a call.

-

Starting with the September 2019 fact sheet, we publish all of ASA's holdings monthly, whereas previously only the top 10 holdings were reported. Until then, the complete holdings were only available from regulatory filings that are published with significant delay. While the smaller holdings may not influence the portfolio much on a day-to-day basis, we believe many investors may appreciate the additional information, especially in the gold mining space where significant value can potentially be added through smaller holdings. ASA's monthly fact sheet is available.

-

Also, starting in September 2019, we initiated a Google Ads campaign seeking to increase investor awareness (Merk pays for the campaign). ASA has not raised money since it was first launched all the way back in 1958, and we do not seek to raise money now. That said, we believe it may be helpful to the discount to have a new generation of investors evaluate whether ASA may be appropriate for them.

Some investors find a significant discount to be a buying opportunity. Such investors may want to evaluate whether our efforts will bear fruit; if so, maybe they can help us reduce the discount by buying shares in ASA.

As mentioned in the semi-annual letter, we were in the process of transitioning the portfolio to be more dynamic so the fund will react more positively to the gold price in a bullish gold environment. Since Merk took over the adviser role of ASA, our analysis suggests the fund has shown increased performance relative to the gold price, indices and peer funds. After significant repositioning of ASA's portfolio, notably by moving down in market cap, we believe the majority of the portfolio transition has been completed.

The significant increase in the gold price during the 2nd and 3rd fiscal quarters was fast and took many by surprise. In our analysis, the initial move in a broader trend always starts with the large caps as market participants move into the liquid names. In our experience, once the market gets comfortable with a higher gold price, the investor base usually moves further down in capitalization, attempting to gain increased leverage to the gold price. The speed at which gold increased appears to have so far limited the breadth of the gains in gold equities. Furthermore, by the fiscal 4th quarter, the Fed was beginning to communicate an end to the recent series of rate cuts. This, and what appears to be an understanding that the trade dispute between the U.S. and China was easing, caused the gold price to drop and then stabilize below $1,500/oz.

In recent months, we continued to move away from the large cap producers and royalty companies, into medium and smaller capitalization companies, which we believe will react more favorably to an increasing gold price due to better growth opportunities and increased margin expansion. We also invested in development and exploration companies based on our belief that the larger companies will need to improve their production profile because mine lives are getting shorter due to lack of investment over the previous 10 years, as when many companies focused on balance sheet improvements and cost reductions. Fortunately, most of these improvements were completed by the time that gold started rallying and a significant portion of that increase should start to drop to the bottom-line during the calendar year 3rd quarter. Among our larger holdings, Agnico, Alacer, Perseus and Detour all showed solid quarterly improvements. Furthermore, a number of smaller companies that we helped finance started to release solid results; in combination with the market feeling comfortable with the medium-term balance sheet, their share prices reacted favorably post financings.

Despite the more dynamic positioning, the portfolio reacted less than some might have anticipated to the down to neutral gold price at the end of the fiscal year. It is in this backdrop that we continue to believe that the fund should continue to outperform in a rising gold environment.

As seen below, ASA's portfolio now emphasizes medium sized producers with significant holdings in development and exploration companies:

Mergers & Acquisitions

The mergers and acquisitions/asset dispositions that the gold sector has been waiting for since the large mergers that Barrick and Newmont undertook at the end of 2018 and early 2019 finally started in the final two months of the calendar year. Once Barrick announced the sale of their half of the Kalgoorlie Superpit to Saracen in early November, a few weeks ensued where we saw eight significant transactions, culminating in the sale by Newmont of the other half of the Superpit to Northern Star in the middle of December 2019, putting this historic asset back into the hands of Australian operators. We believe ASA's portfolio is well placed to participate in further portfolio rationalization into the new year.

It is in this environment, that Merk believes ASA will realize the benefits of a more dynamic portfolio and improved returns. Feel free to reach out to us if you have any questions.

Author

Axel Merk

Merk Hard Currency Fund

Axel Merk is the Founder and President of Merk Investments. Merk is an expert on macro trends, hard money, international investing and on building sustainable wealth.