Are the bond and FX markets ready for this giant disappointment?

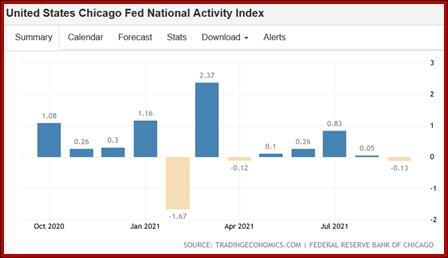

Outlook: Today we get August house prices and September new home sales, both likely to show strong growth, with the Case-Shiller 20-cuity index likely up as much as 20% y/y. We also get the Conference Board consumer confidence index for Oct and the Richmond Fed survey. But the most powerful data is Thursday’s GDP, and for that we get a preview from the Chicago Fed National Activity Index, which dropped to -0.13 in Sept from +0.05 in Aug.

This is the lowest since April and drops in just about every component (although consumption was flat). Trading Economics reports “the index’s three-month moving average moved down to +0.25 in September from +0.38 in August.” See the chart. This is in keeping with the Atlanta Fed’s terrible, awful 0.5% forecast.

Are the bond and FX markets ready for this giant disappointment? Another looming potential shock is an OPEC meeting next week to reconsider the increase in oil output already agreed. OPEC decided once before not to increase the number and expectations of a change of heart this time are unfounded. The energy crisis continues, especially in Europe, but starting to get recognized in the US and everyone watching long-term weather forecasts.

Thursday is also the day the ECB meets, with expectations low of any changes except perhaps the now customary admission that inflation is not so transitory. But by Thursday, the Fed policy meeting the following week will be in view, and tapering fully expected, which should overshadow anything the ECB might have in mind. Besides, the UK releases the new budget tomorrow and is showing a maverick mentality that is entirely foreign to the Europeans. We could also get some minor thrills from the BoC today, expected to taper a bit and perhaps hint at when the end of the taper might be and therefore when the first rate hike might fall. The BoC seems to have signaled mid-year but reports indicate the market sees it sooner (March/April).

While we await what is nearly certain to be very bad news, we have some strange stuff to distract attention. First is the climate change summits and the analysis by everyone, universally, that shows the transition to non-carbon energy is way far behind need. So what do we get today? The Economist reports “ABP, the biggest pension fund in the Netherlands, announced it will stop investing in producers of fossil fuels.” Gee, great timing, on the same day “Saudi Aramco warned that companies need to invest more in production as spare capacity across the world rapidly shrinks. Chief Executive Officer Amin Nasser said that a pick-up in aviation next year could accelerate the issue. OPEC and its allies meet next week to decide whether to change their strategy of increasing production by 400,000 barrel per day each month. Blackstone Inc. co-founder Stephen Schwarzman has a more pessimistic take, saying the shortage of energy could become so severe that it leads to social unrest, particularly in emerging markets.”

Also a nugget of no real importance except it boggles the mind—Tesla became a trillion-dollar company when a car rental outfit committed to buying 100,000 cars. Does no one wonder how the car-renters are going to re-charge them? The number and location or re-charging stations is still far behind the Wish for electric cars.

Then there are the Facebook Papers demonstrating in living color that Facebook deliberately nurtured hatred and discord, as though anyone didn’t know that already. A bit like the attitudes toward the Supreme Court, confidence in institutions is no longer circling the drain, but halfway down the sewer.

Having said that, Bloomberg preempts a panic over slow growth/stagflation with a few nice little charts showing the US economy is still pretty much all right, Jack. The first chart shows robust consumer demand for goods. “Americans are buying a lot of stuff. Yes, it's come down a bit lately, but it's still way above the pre-crisis trend and one reason for the congestion on the ports is just that Americans have money to spend and they're spending a lot of it.”

-637708494381653178.jpg)

Then there’s the job problem. But while “Some of the recent jobs reports have been disappointing. But overall, this labor market recovery has been extremely rapid. Check out this chart of the trajectory of permanent job losses in this crisis versus the last two downturns. The return to normalcy has happened *way* faster than previous go rounds.”

We can buy into these stories but still fret and fume over the looming slowdown in the final two months of the year plus probably Q1. The only real question is how markets respond to the unfolding data that likely began with the Chicago national index. We suspect they are not prepared, being distracted by the likes of Tesla. Having said that, a Shock probably favors the dollar as a safe haven.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat