April Core PCE, Personal Spending and Income Preview: The fall of records, where the wage earner leads, the consumer is sure to follow

- Core PCE price index to fall 0.3% in April.

- Plunging consumer and business spending pressures prices lower.

- Annual core PCE inflation rate to drop to 1.1% from 1.7%, near financial crash low.

- Federal Reserve annual PCE inflation standard to make the largest single month drop on record.

- Personal income and spending expected to plunge to a six decade lows.

- Dismal but expected numbers will not reignite dollar risk trade

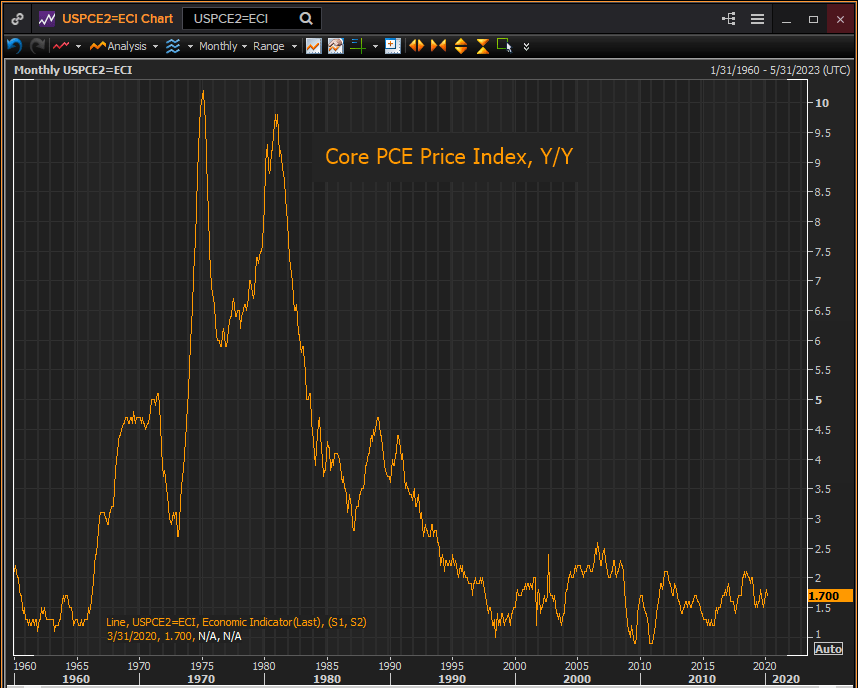

PCE prices

The collapse in consumption and income that has accompanied the destruction of the American labor market combined with the global economic downturn will push US consumer prices to their lowest annual rate since the financial crisis.

Core PCE prices are expected to slip 0.3% in April their largest single month drop in the 61 year history of the series.* Previously the biggest one month decrease was 0.1% which occurred four times, March 2020, March 2017, October 2008 and June 1998.

The annual core PCE rate is forecast to drop from 1.7% in March to 1.1% in April. If accurate this would be the largest one month decline in the yearly rate on record. The lowest annual rate in the 60 year PCE history is 0.9% which registered in July and August 2009 and October, November and December 2010.

Reuters

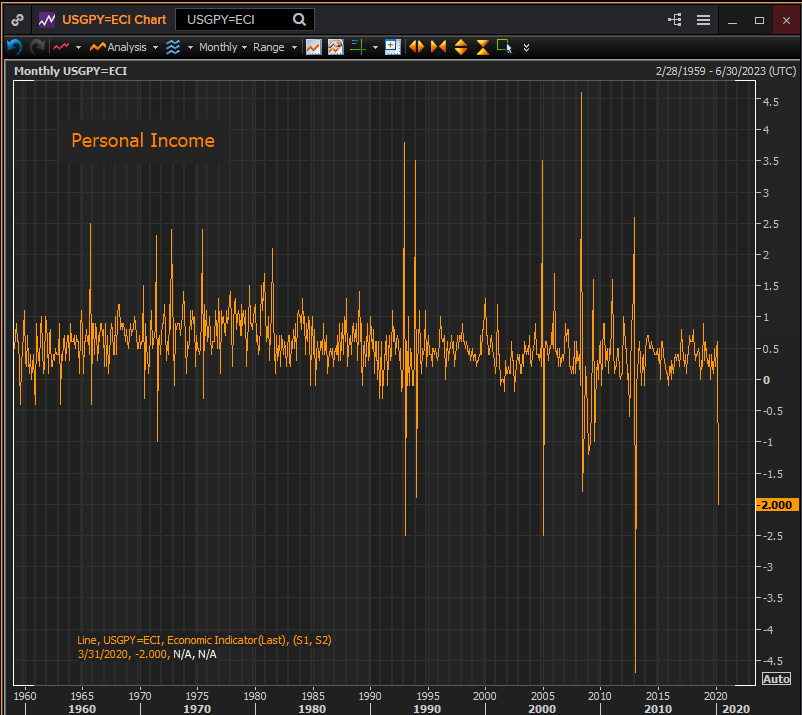

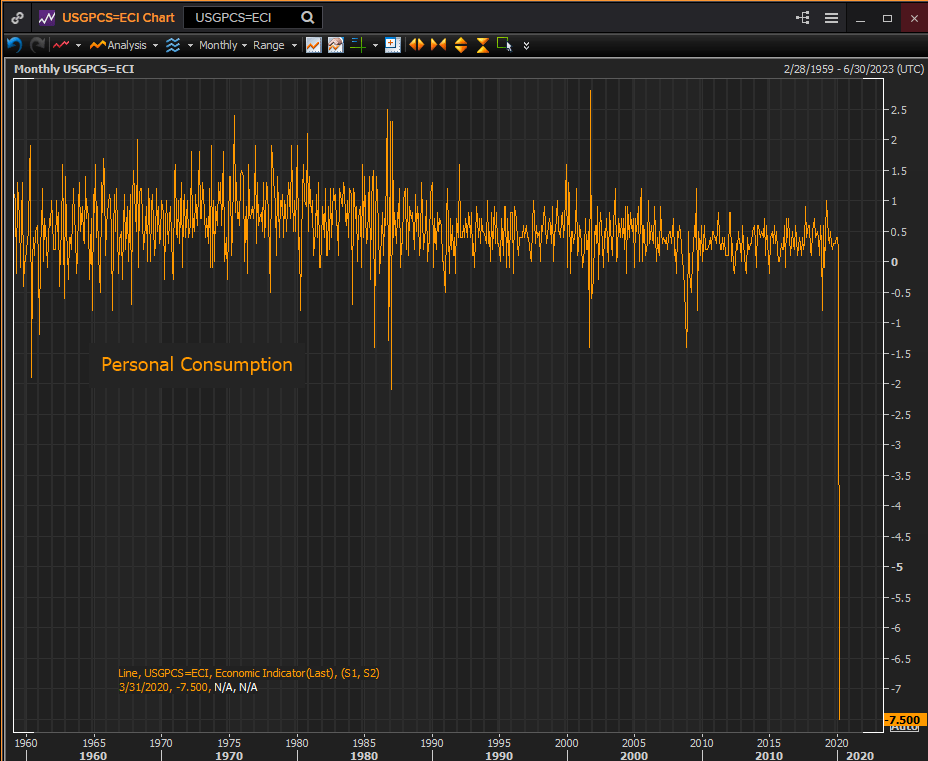

Personal income and spending

Personal income, a wider definition of household and individual earnings that includes investment, pension and other non-wage funds, is forecast to drop 6.5% in April in the largest drop since the series began in February 1959. The prior record was -4.7% in January 2013. The ranges of estimates for April in the Reuters survey is -21.5% to 10.6%.

Reuters

Personal spending is predicted to tumble 12.6% in April after the March 7.5% decline, both by far the largest decreases since inception in February 1959. The range of estimates is from -22% to -5%.

Reuters

Impact of the labor market collapse

The vast increase in unemployment since the middle of March has ramified across the US economy. Even if there were no ordered shuttering of much of the retail establishment on the US economy the sudden firing of 25% of the workforce is a blow to consumption of unprecedented proportions.

In line with the historical debacle in the labor market, wages, income, spending and prices are all falling in tandem. Where the wage earner leads the consumer must follow.

Market response

A curious fact has emerged from the initial unemployment claims in March. The numbers were so large and so out of proportion to anything that had gone before, even comparisons to the financial crisis and the Depression proved inadequate, they have inoculated markets to the steady progression of new low records in payrolls, retail sales, durable goods orders, personal income and spending.

After the claims numbers there are, it seems, few surprises left.

Fed policy

The Fed policy response to the unrolling, if hopefully temporary, economic debacle was set in the first two weeks of March before the surprise of the initial claims numbers confirmed the enormity of the disaster, when it cut the fed funds target by 1.5% in two emergency meetings.

Central bank policies have widened and augmented those initial rate and liquidity provisions with loan programs and Chairman Powell has promised to keep the measures in place until the economy is well and truly on the way to recovery.

The PCE price figures and income and spending results for April, while historically interesting, will add nothing to the Fed’s understanding of the depth of the economic black hole. Its policy response was presciently set more than two months ago.

Conclusion: Markets look ahead

The dramatic new lows that have been set in a slew of US economic statistics from March and April have had only minor impact on the markets over the last month. Instead of elucidating an unknown situation they have only served to define the assumed catastrophe.

Because the economic collapse is expected to be temporary, even if the speed and degree of the recovery is undetermined, equity and currency markets have been pricing the situation two and three months out. The anticipated records in April PCE prices, personal spending and income are already past history.

*A one month decline of 0.6% in September 2001 was part of a statistical adjustment that saw prices rise 0.7% the following month.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.