An amusing look at Brexit scare stories vs what actually happened

Apart from a short-lived disruption of trade flows Brexit has been a macroeconomic non-event.

So Much for the Brexit Scare Stories

Contrary to widespread fearmongering, the UK did not fall to pieces as a result of Brexit.

Wolfgang Münchau, the avid pro-remain, pro-Europe founder of Eurointelligence writes So Much for the Brexit Scare Stories.

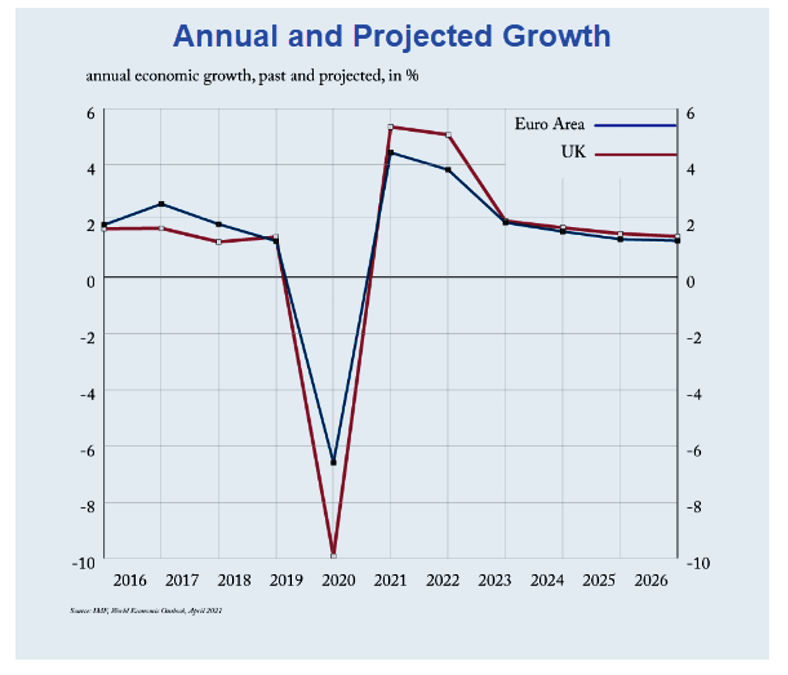

The collapse in UK-EU trade after January 1 was widely reported. What has not been reported nearly as much is that UK exports have fully recovered. They were up 46.6% in February after falling by 42% in January. Imports are not there yet. They were up 7.3% in February after a fall of 29.7% in January. The one prediction I am happy to make is that they will recover too. What these and other numbers are telling us is that even this bit of the Brexit scare stories will not come true. If you look at the latest IMF data and projections in the graphic above, you don't find a discernible macroeconomic effect of Brexit in the first ten years after the referendum. UK growth fell by more last year than eurozone growth, but this will be offset by higher growth this year. The future prosperity of the UK will depend to a large extent on the future policies of the UK government - Brexit or no Brexit.

I am not sure Münchau has the recovery side correct just yet. After a 42% plunge it takes a 72.4% gain to get back to even.

After a 29.7% decline it takes 42.2% gain to get back to even.

Yet, Münchau has the right idea.

And my position all along was that both sides would suffer but ultimately the EU more. So far I believe I am on target.

OK, I did not foresee that the initial collapse in UK exports would be greater than the UK's collapse in imports (with the EU the biggest contributor).

But some of that collapse was the EU purposely making things difficult.

Meanwhile, EU exports to the UK have a much further way to go.

Why the Bad Estimates?

Münchau discusses three reasons.

- The first is political capture by official forecasters. The UK Treasury and the Bank of England were, of course, not neutral players.

- A second group got it wrong because they allowed their political preferences to take over their economic judgments.

- A third group, largely economists, got it wrong because they relied on bad models. There was an overlap of that group with the first and second group, but this one is worth identifying separately. I am talking about models based on long-term trade flows. As Brexit introduces a small degree of friction into physical goods trade, and quite a lot more friction into financial services and agricultural trade, these models predicted a long-term welfare loss. But these models are one-eyed. They only saw what might be lost.

Regarding point 3, Münchau notes events and technologies intrude.

"In the future, we will not only be trading different products, but an increasing proportion of trade will come in the form of data. This is an area in which the UK could benefit from regulatory divergence from the EU."

Who Is Winning the AI Race: China, the EU, or the United States?

A report from the Centre for Data Innovation looking at qualitative criteria shows that the dynamics favour the US in particular. The US is leading on all the key criteria - talent, research, development, hardware, adoption and data - followed by China. The EU had some successes when it comes to the publication of academic papers, but is lagging behind both the US and China in all the other categories. The report concluded that Brexit would diminish the EU’s AI capability further.

Alas, Münchau sticks with his pro-EU stance

I am not making the argument that Brexit will be an economic success. I don't think it will. The best economic argument against Brexit is the one that was never made: that a UK government under either Labour or the Conservatives is unlikely to make best out of the opportunities for regulatory divergence.

Nonetheless, his conclusion is accurate.

The forecasts of unmitigated gloom, however, have been wrong and deceitful. When economists failed to predict the global financial crisis, they did not so out of malice or political bias. But their Brexit forecasts were not an innocent mistake - nor will they be remembered as such.

I strongly disagree with the pro-Europe rah-rah take from Eurointelligence.

However, when it comes to actual discussion of what's going on (vs what they want to happen), the publication generally provides very practical and honest insights.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc

Mike “Mish” Shedlock is a registered investment advisor for SitkaPacific Capital Management.