A Late Credit Cycle for the Nonfinancial Corporate Sector

The economic expansion has continued to age, but expectations for growth and higher rates have risen. How will these new expectations mix with the credit cycle for corporations?

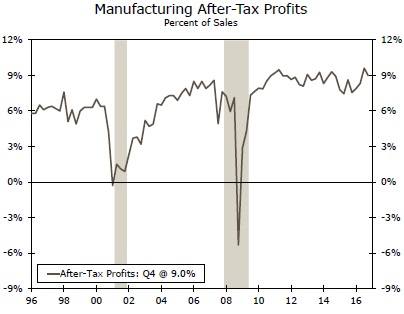

Profit Margins Steady for Manufacturing

Manufacturing after-tax profits, as a percentage of sales, have remained remarkably steady over the past three years (top graph). This pattern helps explain the sustained gains in overall profits, especially for durable manufacturing. Interestingly, the profit margins have been maintained at a higher level than in the prior two economic expansions.

These margins provide a solid basis for jobs/business investment going forward if expectations for final sales were to increase. In the past four months, these expectations appear to have shifted upward. With the addition of actual follow-through on deregulation/tax cuts/trade policy initiatives, this would signal faster growth ahead.

Domestic financing could be supplemented by foreign capital inflows if foreign investors anticipate policy changes will drive more rapid final sales growth ahead. Yet, it remains to be seen if proposed policy initiatives will be put in place in a timely fashion.

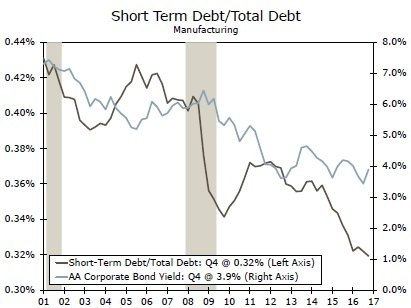

Shorter Debt Maturities Consistent with Lower

Rates Since 2001, short-term debt has declined as a share of total debt as corporate bond rates have declined (middle graph). With sustained profit margins and elevated holdings of corporate cash, this is another factor supporting economic growth going forward in an environment of rising interest rates.

Recent FOMC comments have supported the expectations that interest rates will be rising, on trend, over the next two years. Over the past few years, bond issuance of corporate debt has been met with increased demand for such assets as investors seek yield in what has been a low interest rate, low inflation economic environment. The spread between investment grade corporate debt and U.S. Treasuries has declined since early 2016. This pattern has given the credit system an element of resiliency to deal with the upward movement of interest rates over the next two years.

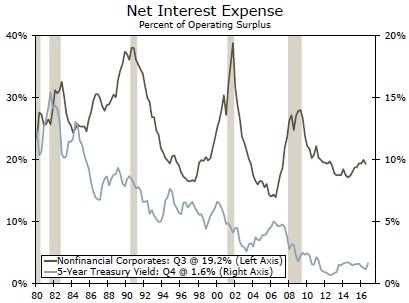

Credit Cycle Turning

Finally, a third element in the credit cycle helping the economy cope with a rising interest rate environment is the current position of net interest expense. This measurement of credit stress has, as a percentage of operating surplus, steadily declined as is typical as the economic expansion ages (bottom graph). The peaks in each cycle are associated with a recession when operating surpluses collapse.

This reinforces the observation that the pattern of interest rates is not the primary driver of the net interest ratio. Instead, the cyclical pattern of net interest expense tends to follow the pattern of growth. Therefore, a gradual increase in short-term rates as envisioned by the FOMC in its latest statements should not represent a near-term challenge to credit markets.

Author

Wells Fargo Research Team

Wells Fargo