A Dove in Hawks clothing [Video]

![A Dove in Hawks clothing [Video]](https://editorial.fxstreet.com/images/Macroeconomics/Events/ElectionUK/Brexit_scrabble_XtraLarge.jpg)

The Day So Far…

GBP remains the currency of choice this morning. Following the hawkish minutes from the Bank of England yesterday the latest move higher has been underpinned by a distinct change of tone from the well-known dove Gertjan Vlieghe. The British-Belgian economist and MPC member surprised markets by stating that interest rates may need to rise “as early as the coming months”, this in essence putting him broadly inline with the majority of his colleagues who see scope for a reduction to stimulus in the period ahead. From a technical point of view the rise in inflation earlier this week, coupled with this growing consensus for impending action in the near-future, has meant GBP futures now trade to levels not seen since the night of the EU referendum itself. As such, expectations of a rate hike before year-end has become a distinct possibility with Deutsche Bank updating their official BoE call to a November hike. Moving forward it seems one half of the argument has been resolved but for the doves to be truly convinced into taking action there remains the contentious debate over soft wage data and political uncertainty over Brexit negotiations.

By this time next week we maybe armed with some degree of clarity on the latter point given UK PM Theresa May will be delivering her key note speech in Florence before then heading to the Conservative Party conference the weekend after. Given the choice of City, an historical trading partner to Britain, the location of May’s speech is telling and if she can achieve a repeat of her 12-principles of Brexit delivered back on the 17th January this year then odds of a rate hike will likely increase further.

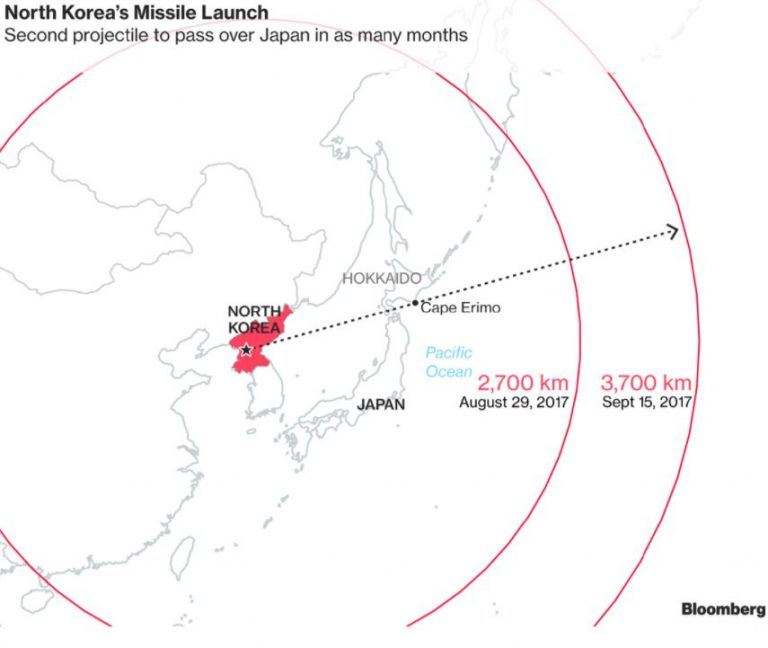

In other news there has been a suspected terrorist incident on an underground train carriage in Parsons Green, London. Reports suggest several people have been injured but there has been no response in the market place and it appears to be an isolated event at this time. Secondly, overnight North Korea test fired another missile over the Northern Island of Hakkaido, Japan. However, reaction to this provocation was decidedly short-lived given movements seen North of the border in recent days and one feels that unless the projectile hits landfall then markets will continue to remain unperturbed. Interestingly, one statistical point to note was that the missile flew approximately 3700km, a distance which puts the Island of US controlled Guam well within range.

The Day Ahead…

Moving forward the schedule looks interesting for this afternoon with US Retail Sales and the preliminary reading of University of Michigan Sentiment due. Despite the impact of Hurricane Harvey in the latter part of the month of August analysts still expect positive readings today and in context of yesterday’s US inflation readings a December rate hike from the Fed is now priced at 51%. Meanwhile, I would still be watching GBP closely as given the breach of key technical levels already there is not much in the way of resistance so a continuation of the trend higher into the weekend looks plausible especially if the US Retail Sales report disappoints. Enjoy the rest of the session and have a great weekend!

Author

Amplify Trading Team

Amplify

Amplify Trading is a proprietary trading company specialising in the development of new trading talent offering direct experience in financial markets.