A 6.9% GDP is not screaming growth, it's screeching brakes

Summary

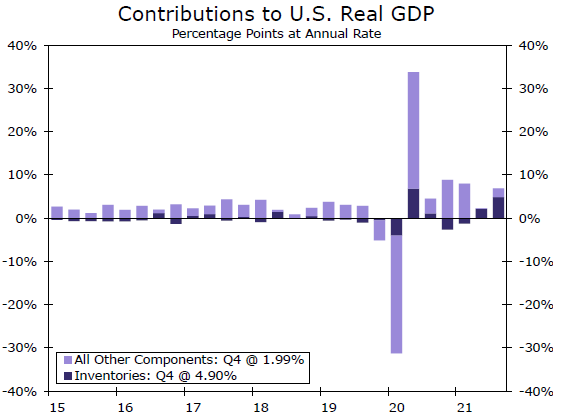

The economy grew at a 6.9% annualized rate in the fourth quarter. Savor the flavor because it will not last; the details behind the better-than-expected headline point to a slowing in spending and a back-up in inventories. Without the boost from inventories, GDP would have been just 2.0% in Q4.

Source: U.S. Department of Commerce and Wells Fargo Economics

A very upbeat signal of a slowdown

It is tempting to celebrate a better-than-expected outturn with 6.9% GDP growth in the fourth quarter (chart), but due to a confluence of factors, we will not likely see that sort of growth again for some time. While to some extent the year-end surge was a function of steady consumer and business spending, both petered out at the end of the year as Omicron cases climbed and hospitalizations followed.

Not knowing what was coming in terms of the pandemic, many retailers stocked up in anticipation of strong holiday sales and businesses continued to pull out all the stops to source much-needed inventories. But after a strong October and decent November, retail sales ended the year with a flop in December. Meanwhile, the challenge businesses have already faced finding workers was exacerbated by increased absenteeism due to illness related to the new variant. Against that backdrop, inventories started stacking up. The result of this stockpiling was a 4.9 percentage point boost to headline growth from inventories (chart). We had anticipated a build, but this was even larger than we had penciled in. That makes it difficult for inventories to provide a lift in the first quarter. In the absence of that boost, our already modest expectation for 2.8% GDP growth in Q1 may get revised even lower.

Advance trade figures for December released yesterday showed a significant widening in the country trade deficit. On that basis, we had been poised for a drag from net exports for the fourth quarter; and trade was perfectly neutral in terms of its contribution to headline growth (even taken out to two decimal points; it was 0.00). We look for trade to be a consistent drag on headline GDP growth throughout 2022, but here too, we worry the surprisingly neutral influence in Q4 will either be revised lower or come at the expense of an even larger drag on first-quarter growth. The trade deficit doesn't widen without weighing on growth at some point.

Author

Wells Fargo Research Team

Wells Fargo