2022 holiday sales: The last hurrah

Summary With a recession on the horizon and inflation crimping holiday budgets, you might be surprised to hear that our forecast puts holiday sales on track for a 6% annual increase, well north of the long-run average of 4.6%. This report makes the case for why this holiday shopping season will represent the Last Hurrah for this economic cycle.

-

Despite the pandemic, holiday sales have grown at a historic pace for the 2020 and 2021 holiday seasons. This year, with pandemic fears now largely in the rearview mirror, consumers are looking forward to a more typical holiday shopping season.

-

We expect real holiday sales will rise about 2%, but thanks to prices, the gain will appear three times as large. In keeping with our long-standing tradition of forecasting the nominal increase, our holiday sales forecast is 6%, though admittedly that says more about prices than it does about increased holiday spending.

-

The staying power of the consumer has proved to be robust throughout this cycle, but we view this holiday shopping season as a Last Hurrah for the consumer in light of our recession call for next year.

-

Cash reserves that households built up during the previous two years have begun to decline, a sign that could indicate consumer staying power is starting to wane. Household finances have taken a hit with a lower saving rate and declining real wages, posing a possible downside risk to holiday sales activity in the coming months.

-

Consumers in the 2020 and 2021 shopping seasons faced limited competition for their dollar with dining out and other services spending largely off the table. This coming season, however, these same consumers look to resume holiday travel and other services spending amid a period of historically high inflation.

-

In our view, the price-taking consumer from the past two seasons will give way to the deal-hunting consumer, a sentiment that could be at odds with retailer plans that look to pare back the blockbuster Black Friday deals of years past.

The last hurrah

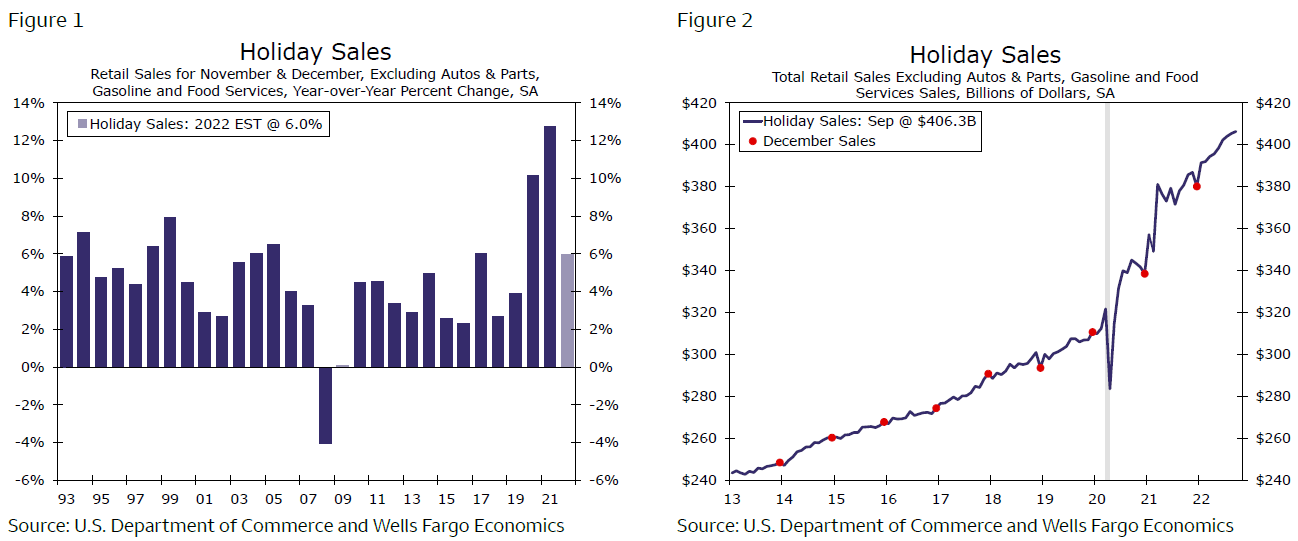

There hasn’t been a “normal” holiday shopping season since 2019 and make no mistake, retailers wouldn’t have it any other way. Despite all the challenges of securing inventory amid supply-chain congestion and finding staff despite a tight labor market, stores have been raking it in the past couple of years. In fact, looking back over the past 28 years, the two biggest annual increases in holiday sales have occurred in each of the past two years.1 But surely this year amid soaring inflation and deflated consumer sentiment the good times for holiday sales are over, right?

Not according to Santa’s watch; our forecast anticipates holiday sales will increase 6% this year, which if realized would be above the long-run average of 4.6% (Figure 1). That may be an unexpectedly upbeat forecast from the same people who are calling for a recession to take hold in 2023, but our holiday sales call says as much about what has already occurred this year as it does about what is ahead in the remaining months of it. The fact is: the uncanny staying power of the consumer in the first nine months of the year puts us on track for a solid outturn even if sales finish the year with a thud as they did last year with a very disappointing December (Figure 2). Our 6% annual forecast implies just that; below-average sales growth in October and November followed by a weak December. Make no mistake, we still anticipate that consumer staying power will run out by early next year and that retrenchment in consumer spending will play a key role in the broader recession we expect to take hold. This report makes the case for why this holiday shopping season will represent the Last Hurrah for this economic cycle.

Author

Wells Fargo Research Team

Wells Fargo