Why surprisingly low Hungarian inflation could be a game changer

Inflation in Hungary came in unexpectedly low in May, which could alter the scope for action previously anticipated by the National Bank of Hungary. The question has shifted – it's no longer whether there will be a rate cut, but how far rates will be cut in the next meeting.

Inflation fell, but will start growing again

Contrary to all expectations, the latest data released by the Hungarian Central Statistical Office (HCSO) shows that inflation slowed in May 2026. Consumer prices remained flat on a monthly basis, which was not anticipated during a period marked by an energy crisis. Given this, it is hardly surprising that the year-on-year index slowed by 0.3ppt to 1.8% in May. As no analyst had anticipated a slowdown in inflation, the latest data release could be described as the ultimate surprise.

Given that the war in Iran has now been ongoing for three months and the Strait of Hormuz has essentially been blockaded for the same amount of time, the Hungarian data trend – with a touch of exaggeration – defies all known economic correlations to date. Let's take a closer look at the reasons behind this resilience.

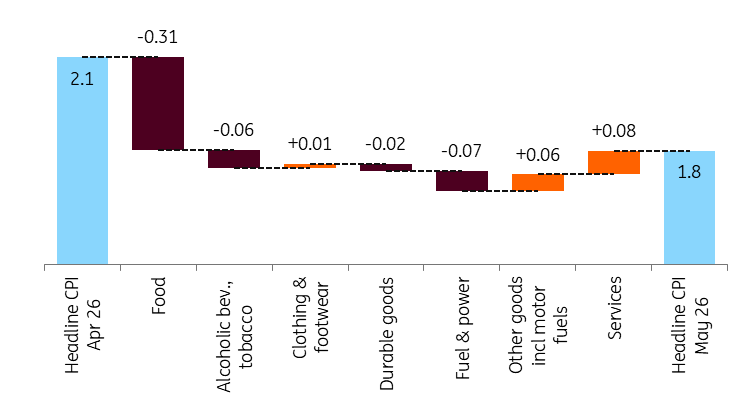

Main drivers of the change in headline CPI (%)

The details

- Year-on-year food inflation has slowed significantly, particularly when restaurant meal prices are excluded. Without this, both unprocessed and processed food prices showed deflation of over 2% on a yearly basis. This clearly demonstrates the impact of the strengthening of the Hungarian forint.

- Speaking of the forint, it has also helped to keep price increases moderate for other import-sensitive items in the consumer basket, such as clothing and durable goods. However, the latter still shows above-average yearly price increases, mainly due to rising jewellery and vehicle prices.

- Household energy prices have fallen significantly for the second consecutive month, primarily due to a weather-related decline in energy consumption.

- Inflation in the services sector remains the main contributor to overall price pressure, with the rate of price increases creeping up to 4.3%. Rising labour costs, particularly in labour-intensive sectors, are likely to be the main driver of price adjustments. Conversely, the sharp drop in transport service prices is also a significant development. It seems that the strengthening of the forint has offset the impact of rising global energy prices. This is evident in the price of airline tickets

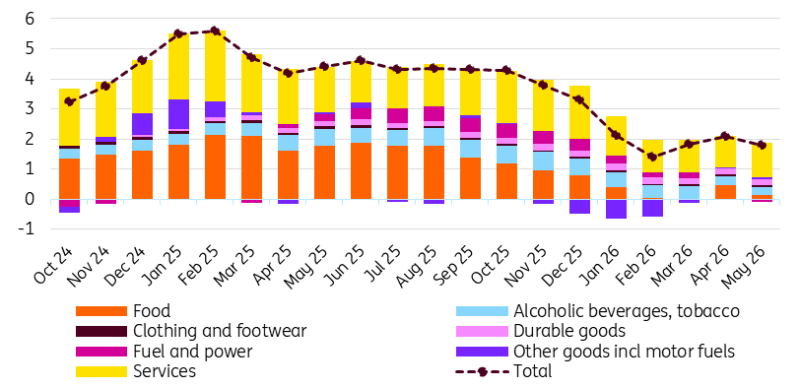

The composition of headline inflation (ppt)

Core inflation slows, but risks are growing

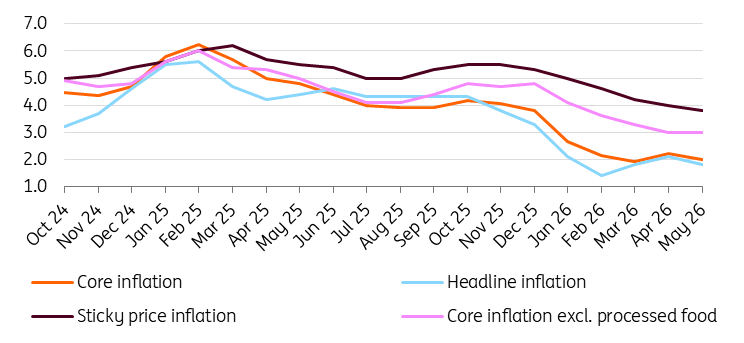

The core inflation rate, which is adjusted for volatile items including changes in fuel prices, also slowed down. Based on our detailed analysis, which showed that it was not just non-core items that kept inflation in check, it is hardly surprising that the average price of the core basket remained unchanged while the year-on-year rate dropped to 2.0%. This suggests favourable effects also appeared in core inflation, with no evidence of second-round effects from a global energy price shock. However, the risk of these effects showing up sooner or later is growing with each passing day that the imported trade corridor remains under blockade. The longer the blockade continues, the greater the likelihood of a major price shock due to non-linearities.

Headline and underlying inflation measures (% YoY)

The outlook for inflation has just improved again

In light of the latest inflation figures, it is now clear that this year's inflation rate will be considerably lower than the trajectory projected by the National Bank of Hungary in March. The May figure is not only lower than the NBH’s point estimate of 3.0%, but also lower than the lower end of the forecast's uncertainty range of 2.3%.

Clearly, the global energy price shock will be noticeable, and the momentum behind the strengthening of the forint will not last forever. This is partly because the exchange rate against the euro has stabilised at around 355 over the past month. Nevertheless, we should expect the various price shield measures to remain in place permanently, given that the decree has become law and the official phase-out date has been removed. Based on this, the central bank will need to significantly revise its inflation trajectory in the Inflation Report due in June.

According to our latest flash estimate, the inflation trajectory is looking more favourable than it was a week ago. While we will have to wait until autumn for inflation to accelerate to around 3%, the rate may peak at only around 4% by the end of the year. Consequently, we are now projecting an average inflation rate of just 2.6% for this year. At the same time, average inflation could exceed 4% in 2027. However, by the end of next year, price pressures could approach the 3% level consistent with price stability.

A rate cut is written on the wall, the question how big it will be

In our view, today's inflation data clearly gives the NBH the green light to cut interest rates on 23 June. The key question now is whether the Monetary Council will cut rates by 25bp or 50bp. FX swaps and retail government bond yields have also recently been lowered by 50-50bp. The forint has strengthened by 10% since March, and the long end of the yield curve has fallen by 200bp.

However, there is a great deal of uncertainty due to the domestic fiscal outlook, the transformation of economic policy and geopolitical shocks, which could cause the favourable situation to collapse at any moment. Therefore, it would be understandable if the decision-makers remained cautious and opted for regular-sized easing. However, given the extremely favourable alignment of markets and macro, the NBH may now act more opportunistically, seizing advantage of current conditions to cut the base rate by 50bp to 5.75% in two weeks' time. It would be difficult to label this a policy mistake at this stage, especially since it would allow for a more hawkish approach if inflationary pressures emerge.

Yet, based on the National Bank of Hungary's latest official communication, which dates back to the data release, our base case scenario continues to anticipate the safer move of a smaller rate cut. Still, the likelihood of a more opportunistic move is increasing, and the Monetary Council members have sufficient time to reconsider and signal whether they are willing to take a bold approach.

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.