Wall Street just made its biggest earnings upgrade since 2021

For all the noise about inflation and rate uncertainty this year, the numbers coming out of Wall Street’s research desks tell a different story than the one dominating headlines. Heading into the Q2 2026 earnings season, analysts haven’t been trimming their forecasts to hedge against a slowdown. They’ve been raising them — aggressively, and in a pattern that hasn’t been seen in five years.

The biggest upgrade since 2021

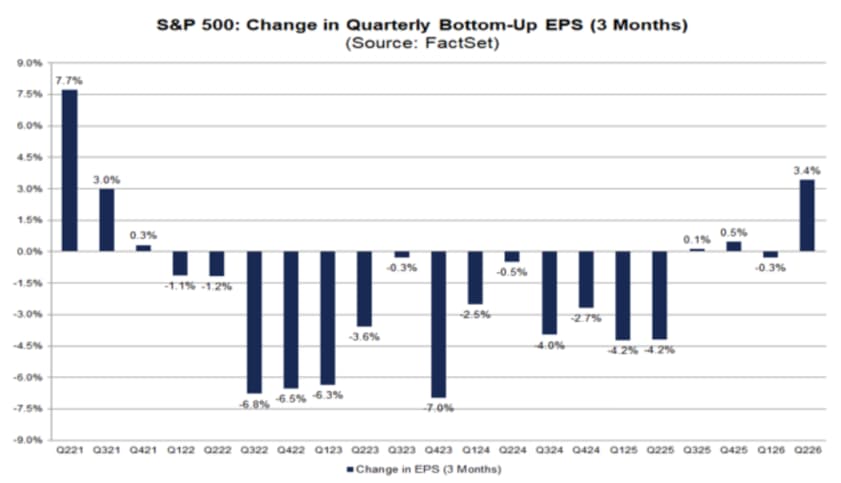

Between March 31 and June 30, the bottom-up EPS estimate for the S&P 500 — essentially the aggregated median forecast across all 500 companies — climbed 3.4%, from $78.84 to $81.54. That might sound modest, but it runs directly against the grain of how earnings season typically unfolds. In a normal quarter, analysts cut their numbers as the quarter progresses, not raise them.

Over the past five years, the average decline during the quarter has been 2.0%. Stretch that back ten years and it’s 2.7%; twenty years, and it’s a 4.2% average cut. This quarter didn’t just avoid that pattern — it reversed it outright, marking the largest increase to a quarterly bottom-up EPS estimate since Q2 2021, when estimates jumped 7.7% during the post-pandemic recovery surge.

It’s not just Q2 either. Full-year 2026 estimates got the same treatment, rising 6.3% over the same three-month window, from $320.39 to $340.52 per share.

Where the optimism is (and isn’t)

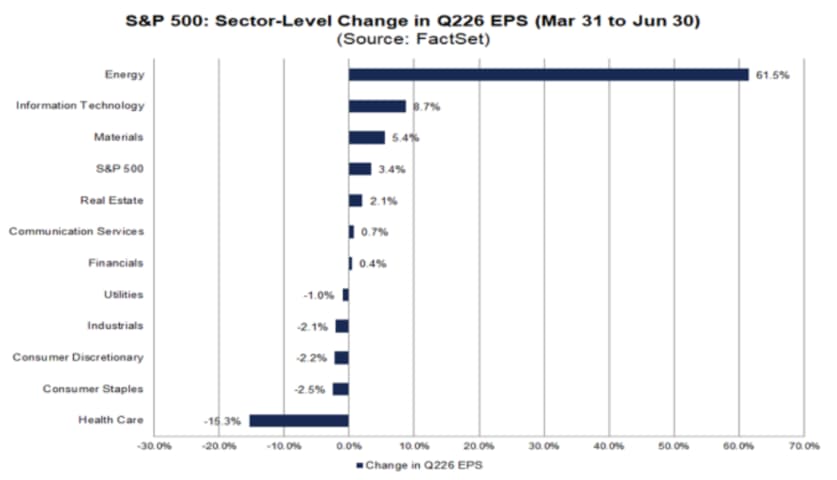

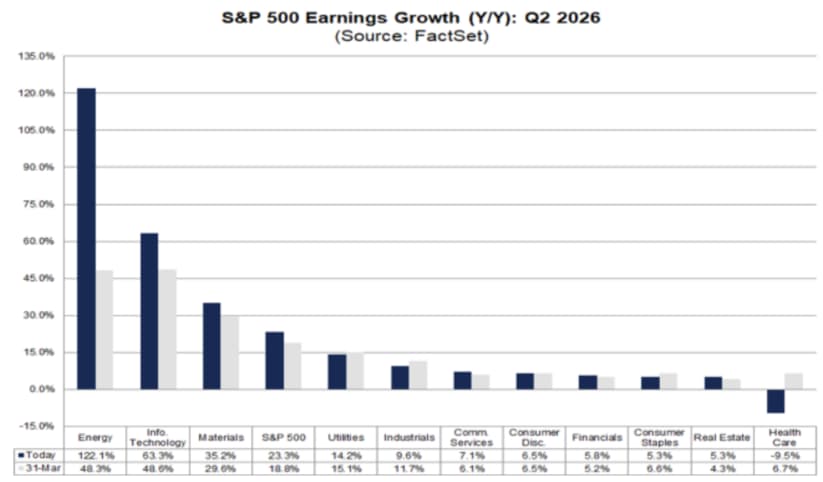

This is maybe the part that matters most for stock selection: the upgrade cycle is not broad-based. Six of eleven sectors saw their Q2 estimates rise during the quarter, but the gains are heavily concentrated in two places.

Energy led by a wide margin, with estimates up 61.5% — largely a function of how depressed the sector’s prior-quarter comparisons were. Information Technology came in second at 8.7%, which is a far more organic and telling number given the size and weight of the sector in the index.

On the other side of the ledger, Health Care saw the steepest cut of any sector, down 15.3% for the quarter, and remains the only sector expected to post a year-over-year earnings decline for Q2.

Guidance is confirming the trend, not just estimates

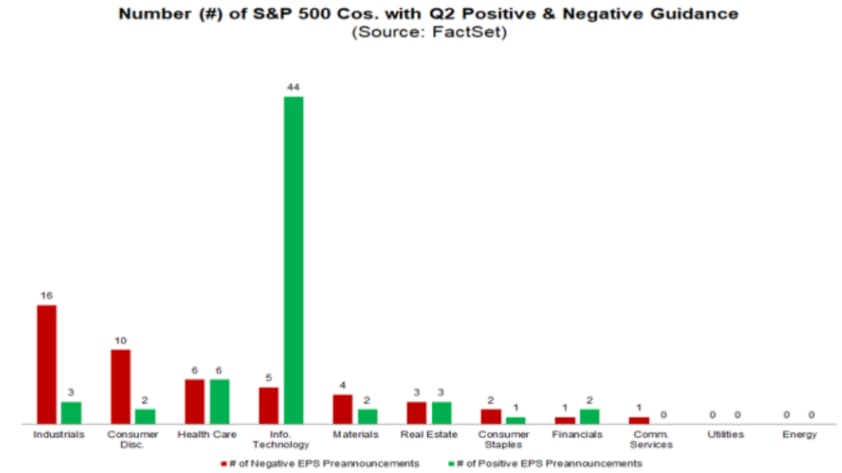

Analyst forecasts are one thing; what companies themselves are signaling is another…but here the alignment is unusually clean. Out of 111 S&P 500 companies providing Q2 EPS guidance, 57% (63 companies) issued positive forecasts. This positive rate significantly outpaces both the 5-year and 10-year historical averages of 41%, marking the highest optimism seen since Q3 2021. Conversely, bearish outlooks are declining; the 48 companies issuing negative guidance represent the lowest total since Q3 2021’s low of 40.

Technology is again the standout. Of all eleven sectors, Information Technology has produced 44 companies issuing positive guidance — a record for the sector since 2006, surpassing the prior high of 36 set in Q3 2025. Within Tech, semiconductor and software names are driving most of that: Semiconductors & Semiconductor Equipment logged 13 positive guidance issuances, and Software another 12.

Put together with the sector’s 8.7% estimate increase, it’s a rare case of guidance and analyst forecasts reinforcing each other rather than working at cross purposes — and it sets up Information Technology to report the second-highest earnings growth rate of any sector this quarter, at 63.3%.

The growth numbers traders are pricing in

With upgrades running this hot, the index-level growth expectations have moved accordingly. The S&P 500 is now projected to post year-over-year earnings growth of 23.3% for Q2 2026, up from an 18.8% estimate as of March 31. If that holds, it would mark the second straight quarter of earnings growth above 20%, and the seventh consecutive quarter of double-digit growth — a streak that’s now stretched long enough to stop being an anomaly and start being a trend line.

Revenue forecasts reflect a similarly bullish trend, with expected year-over-year growth rising to 12.2% from March’s 9.5% projection. Achieving this would mark the strongest top-line expansion since Q2 2022 (13.9%) and secure a second consecutive quarter of double-digit growth. Across the market, all eleven sectors are projected to increase revenue, while ten of eleven will grow earnings—with Health Care serving as the sole detractor on the earnings front.

Bottom line

The upward revisions aren’t isolated to this quarter. Analysts are currently modeling 26.8% growth for Q3 and 24.4% for Q4, putting full-year 2026 earnings growth at 24.1%. That’s an aggressive glide path, and it’s arriving at a moment when the market has already been setting records on its own.

The Dow closed the first half of 2026 up 8.9%, marking its best first-half performance since 2021, while the S&P 500 gained roughly 9.6% and the Nasdaq climbed nearly 12.8% over the same stretch. The Dow has since pushed past 53,000 for the first time, and the S&P 500 touched a fresh all-time high in early July before slipping back. Traders are now watching whether the index can extend an unusual 11-year streak of positive Julys into a twelfth straight year — a run that has survived bear markets before, but is being tested this year by stretched valuations.

That valuation backdrop is the tension worth sitting with. The S&P 500’s forward P/E sits at 20.4, above its 10-year average of 19.0, meaning the market has already been paying up in anticipation of exactly the kind of earnings strength analysts are now forecasting. Rather than earnings surprises driving the rally from here, the rally has partly been the one pulling estimates up to meet it — a dynamic that raises the bar for what "beating expectations" will actually mean as the year progresses.

It’s also worth noting the record-setting has been narrow. Big Tech names carried much of the first-half gains, but the so-called Magnificent Seven lost roughly $2.3 trillion in combined market value in June alone amid questions over whether AI spending will translate into profits — even as Wall Street rotated toward AI suppliers like memory and semiconductor names instead.

That’s the same concentration story showing up in the earnings data: Tech is doing the heavy lifting on both the estimate-revision side and the market-cap side, which means the sector’s Q2 results carry outsized weight for whether this record-setting run has room to keep going or whether it’s already priced for perfection. For traders, a strong Q2 print may already be baked into both the earnings estimates and the index level itself, which puts more emphasis on guidance and forward commentary than on the headline beat.

Stay up to date with what's moving and shaking on the world's markets and never miss another important headline again! Check ActivTrades daily news and analyses here.

Author

Carolane de Palmas

ActivTrades

Carolane graduated with a Masters in Corporate Finance & Financial Markets and got the AMF Certification (Financial Markets Regulator in France). Afterward, she became an independent trader, investing mostly in European and American stocks/indices.