The hand-to-mouth stock market rally

A rotation is going on in US stocks right now, the weakest performing companies on the S&P 500 include those most closely linked to AI, including Palantir and Oracle, which are down 18% and 16% respectively this week. There are also chunky losses for some of the Magnificent 7, including Microsoft, Alphabet, Apple and Nvidia. The move away from tech heavy AI names is allowing value stocks to shine. The top performing sectors in the US this week include industrials, real estate, consumer discretionary, energy and healthcare, which is the top performing sector and is higher by more than 4%.

The hand to mouth tech rally has come to an abrupt halt at the end of the week. After Thursday’s recovery rally on the back of Micron results, which caused the stock price to soar by 15%, a dearth of good news is weighing on the sector and the entire AI narrative. Micron’s stock price is down 4% in the pre-market, other memory chip stocks are also sinking, and SanDisk is down 5%. Nvidia is also lower by 1%, which could drag US stock indices lower if Nvidia’s losses persist as we move through Friday.

Tech sector loses momentum

We had noted that the tech stock rally is losing momentum. Over June, we have seen momentum slow down, which has allowed small cap stocks to become the main driver of US markets this week. This matters for investors, and it suggests that the AI theme is no longer acting like a rising tide. Investors are taking their time and picking winners in the AI trade, while discarding others. For example, take the opposing fortunes of Alphabet and SanDisk this week. Neither reported earnings, but SanDisk was boosted by demand for memory chips, its stock price is higher by 14% so far this week, even though it is expected to fall sharply later today. In contrast, Google’s share price is down 6% so far this week, as the market falls out of love with hyperscalers, especially ones who are tapping bond and equity markets to raise cash.

IPOs on hold

The AI trade is suffering from a lack of good news, which is holding back tech on Friday. News that OpenAI would delay its IPO until next year, over fears it would not attract enough interest to give it a $1 trillion listing has also weighed on the market mood on Friday, and European tech stocks are also lower. Alternatives, including listing at a lower price, were apparently ruled out by CEO Sam Altman, according to reports. It appears that lessons may have been learned from the SpaceX IPO. Its share price has fallen 13% this week, and is expected to open down by another 1% on Friday.

While Sam Altman may have to delay his mega payday, if OpenAI does delay its IPO to 2027, this removes a major hurdle for financial markets. It was always going to be hard for OpenAI, Anthropic and SpaceX to list around the same time, with huge valuations. There were concerns that the market could not absorb this amount of equity issuance, and it could be a major trigger for market volatility. If OpenAI and Anthropic stagger their IPOs over the next 18 months or so, the market may be better placed to absorb these new listings.

The risk of government intervention

There is an added risk for OpenAI and Anthropic: US government intervention. The US government has directly intervened in both Anthropic and OpenAI’s business plans in recent weeks. Firstly, the White House banned Anthropic from allowing foreigners to access its powerful Mythos model, which resulted in Mythos getting switched off altogether, since Anthropic could not isolate access to only American nationals. This week, the US government has asked OpenAI to release its latest ChatGPT model for security testing.

Government meddling/ intervention is a major risk for these AI companies and could dent their valuations. Thus, we may see Anthropic follow OpenAI and delay IPO plans. A more prudent approach could be to delay IPOs until there is an agreed global regulatory framework, until then, the risk of government intervention remains high.

Why the outlook is bright for the UK

Looking ahead, the focus will be on where US markets close on Friday. While the longer-term trend remains bullish, the short-term risk is for further consolidation and more pullbacks. There is also a lot going on underneath the surface. The increase in oil supply from the Middle East is causing a mini supply glut, which is good news for non-tech sectors of the market. The oil price is lower by more than 3% on Friday for Brent crude, and the $70 per barrel level is now in sight. This is good news for consumer discretionary, luxury and industrials, and it explains why the Kospi is the worst major performing index this week, and why the FTSE 100 is one of just three positive major indices so far this week and is outperforming the S&P 500 and the Nasdaq.

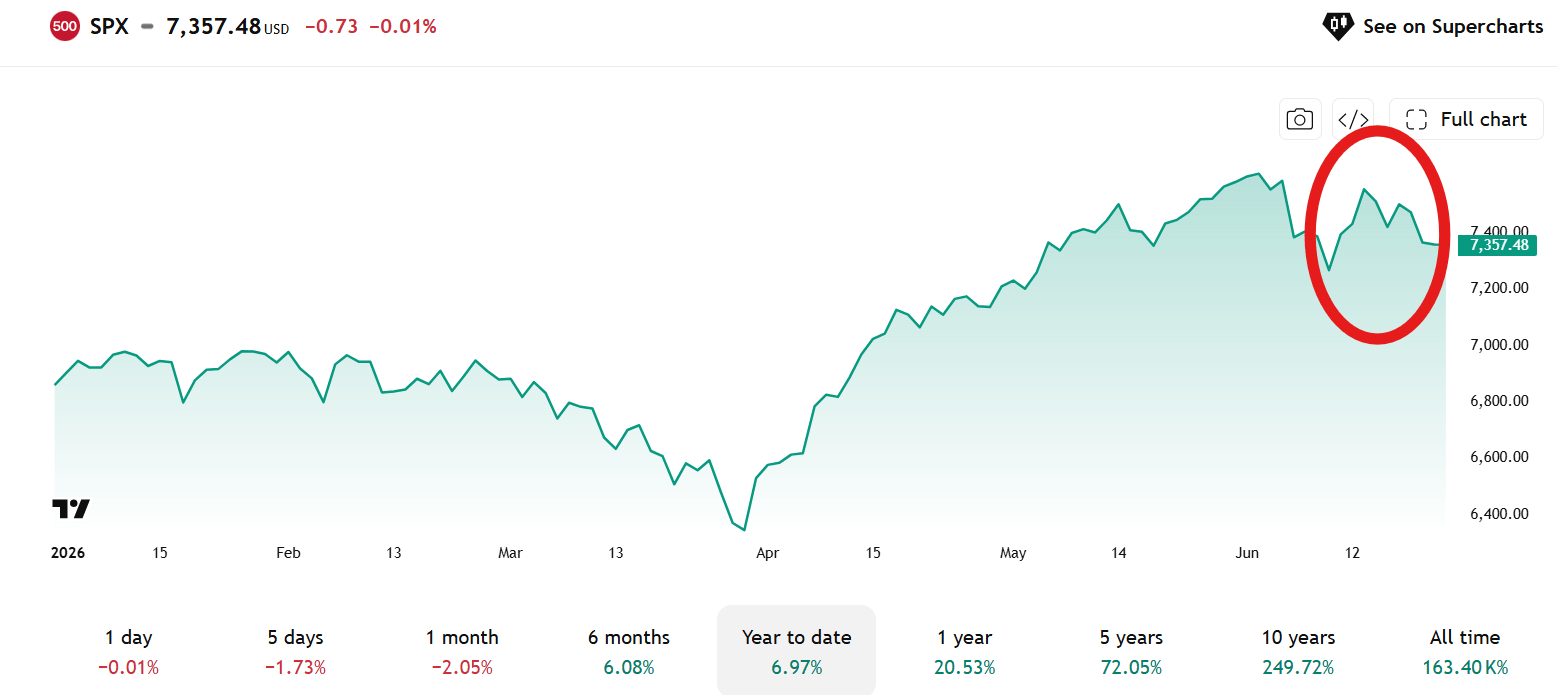

Chart 1: The S&P 500

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.