Required Minimum Distributions: Navigating through your IRA's required withdrawals

After a certain age, holders of retirement accounts such as Individual Retirement Accounts (IRAs) are required to start making mandatory withdrawals, known as Required Minimum Distributions (RMDs).

These withdrawals, imposed by the U.S. tax authorities, must be carefully anticipated to avoid heavy penalties and preserve the coherence of your retirement strategy.

Understanding how RMDs work

RMDs are minimum withdrawals imposed by the Internal Revenue Service (IRS) on funds held in certain retirement accounts, notably Traditional IRAs.

They are designed to ensure that savings accumulated tax-free over the years are actually subject to tax at retirement.

Since the SECURE 2.0 law came into force, the age at which these withdrawals are required has been raised. People born between 1951 and 1959 must start their RMDs at age 73, while those born in 1960 or later must wait until age 75.

Roth IRAs, on the other hand, are not subject to RMDs as long as the account holder is alive, making them a strategic long-term tool for certain people in retirement planning.

Calculation method

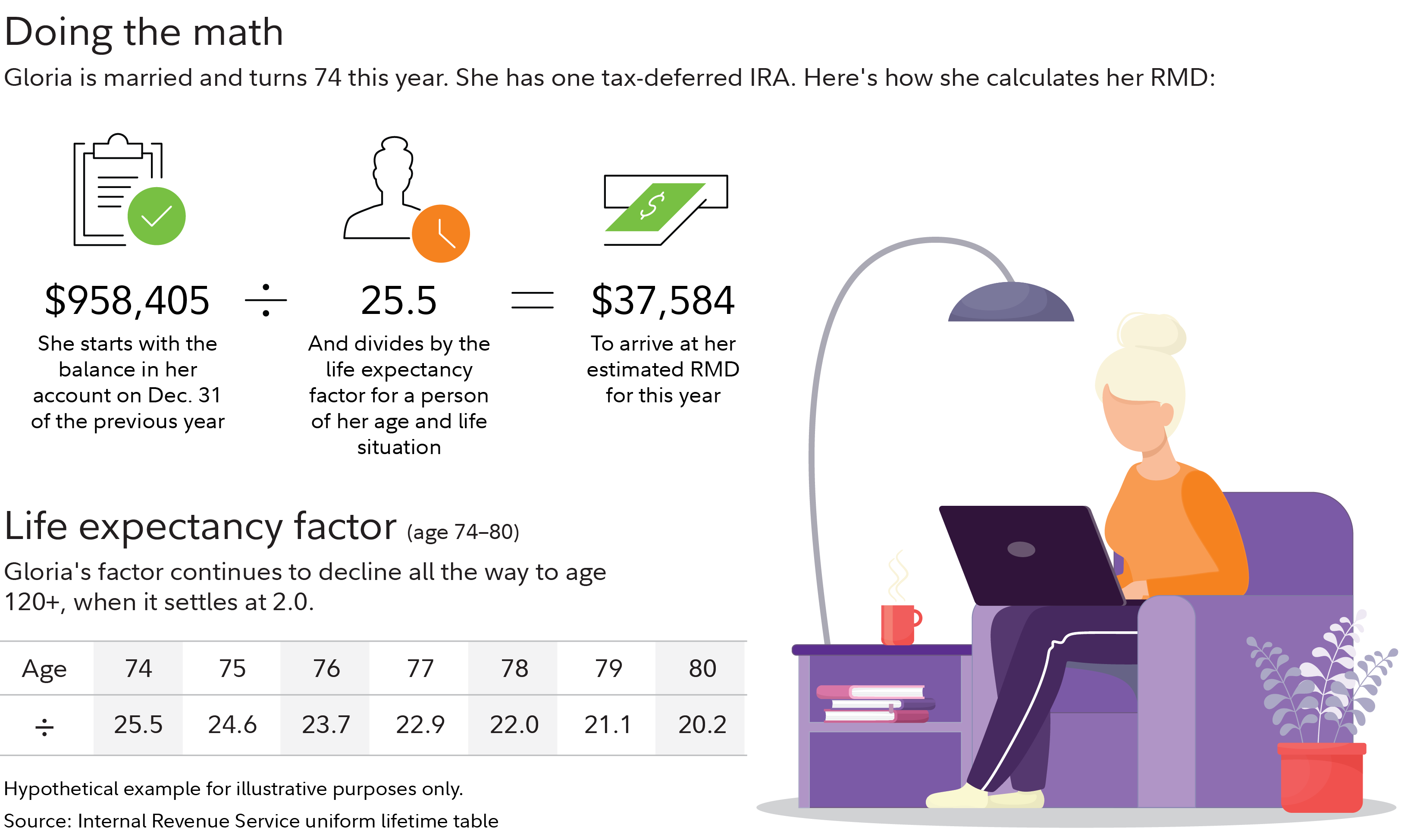

The annual RMD is calculated by dividing the account balance at December 31 of the previous year by a factor determined by the IRS, based on the account holder's life expectancy. This calculation is updated each year.

For example, if the IRA balance is $500,000 and the IRS factor is 25, the minimum amount to withdraw will be $20,000.

This amount is considered taxable income, and its omission can result in a penalty of up to 25% of the amount not withdrawn, reduced to 10% if the error is corrected promptly.

Interaction with Social Security benefits

RMDs are added to other sources of retirement income, notably Social Security benefits.

This combination can push the retiree over a higher tax threshold, resulting in increased taxation, including on a portion of social security benefits that would otherwise be partially or totally exempt.

It is therefore essential to integrate RMDs into a global approach to retirement planning, taking into account all available income and its tax impact.

Withdrawal schedule

The first RMD must be made no later than April 1 of the year following that in which the holder reaches the required age. For subsequent years, withdrawals must be made by December 31.

It is important to note, however, that postponing the first withdrawal until April 1 implies two withdrawals in the same tax year, which may result in a significant increase in taxable income.

Planning strategies

There are several strategies for limiting the tax impact of RMDs and integrating them optimally into a retirement strategy:

- Converting to a Roth IRA: Gradually transferring a portion of funds from a Traditional IRA to a Roth IRA eliminates future RMDs on converted amounts, while taking advantage of favorable tax treatment on withdrawals.

- Use RMDs to finance current expenses: Withdrawals can be used to cover day-to-day living expenses in retirement, limiting the need for other taxable sources of income.

- Qualified Charitable Distribution: All or part of the RMD can be transferred directly to a recognized charity. This donation, capped at $100,000 per year, is not included in taxable income.

- Spread withdrawals over the year: Withdrawing the required amounts in monthly or quarterly payments can optimize cash management and spread out tax charges.

Special case of multiple accounts

When a taxpayer holds several IRA accounts, he or she is allowed to calculate the total amount required for all accounts and make the withdrawal from just one of them.

However, this flexibility does not apply to 401(k) plans, for which each account is treated separately and requires its own RMD.

Long-term issues

RMDs should not be seen as a mere administrative formality, but as a central element of end-of-career financial planning.

Integrating them into a coherent retirement planning scheme optimizes overall taxation, preserves the value of remaining assets and coordinates withdrawals with Social Security benefits.

Anticipating these withdrawals well before the legal retirement age can limit their negative impact. The choices made by savers in their 50s and 60s have a decisive effect on the structure of their future income and their ability to cope with unforeseen events.

Anticipating RMDs

Required Minimum Distributions are an unavoidable regulatory constraint for holders of certain retirement accounts, but also an opportunity to efficiently structure their withdrawals and taxation.

By approaching them with rigor and anticipation, retirees can minimize their negative effects and preserve their long-term financial security objectives.

IRAs FAQs

An IRA (Individual Retirement Account) allows you to make tax-deferred investments to save money and provide financial security when you retire. There are different types of IRAs, the most common being a traditional one – in which contributions may be tax-deductible – and a Roth IRA, a personal savings plan where contributions are not tax deductible but earnings and withdrawals may be tax-free. When you add money to your IRA, this can be invested in a wide range of financial products, usually a portfolio based on bonds, stocks and mutual funds.

Yes. For conventional IRAs, one can get exposure to Gold by investing in Gold-focused securities, such as ETFs. In the case of a self-directed IRA (SDIRA), which offers the possibility of investing in alternative assets, Gold and precious metals are available. In such cases, the investment is based on holding physical Gold (or any other precious metals like Silver, Platinum or Palladium). When investing in a Gold IRA, you don’t keep the physical metal, but a custodian entity does.

They are different products, both designed to help individuals save for retirement. The 401(k) is sponsored by employers and is built by deducting contributions directly from the paycheck, which are usually matched by the employer. Decisions on investment are very limited. An IRA, meanwhile, is a plan that an individual opens with a financial institution and offers more investment options. Both systems are quite similar in terms of taxation as contributions are either made pre-tax or are tax-deductible. You don’t have to choose one or the other: even if you have a 401(k) plan, you may be able to put extra money aside in an IRA

The US Internal Revenue Service (IRS) doesn’t specifically give any requirements regarding minimum contributions to start and deposit in an IRA (it does, however, for conversions and withdrawals). Still, some brokers may require a minimum amount depending on the funds you would like to invest in. On the other hand, the IRS establishes a maximum amount that an individual can contribute to their IRA each year.

Investment volatility is an inherent risk to any portfolio, including an IRA. The more traditional IRAs – based on a portfolio made of stocks, bonds, or mutual funds – is subject to market fluctuations and can lead to potential losses over time. Having said that, IRAs are long-term investments (even over decades), and markets tend to rise beyond short-term corrections. Still, every investor should consider their risk tolerance and choose a portfolio that suits it. Stocks tend to be more volatile than bonds, and assets available in certain self-directed IRAs, such as precious metals or cryptocurrencies, can face extremely high volatility. Diversifying your IRA investments across asset classes, sectors and geographic regions is one way to protect it against market fluctuations that could threaten its health.

Author

Ghiles Guezout

FXStreet

Ghiles Guezout is a Market Analyst with a strong background in stock market investments, trading, and cryptocurrencies. He combines fundamental and technical analysis skills to identify market opportunities.