Constellation Energy Stock analysis: Is CEG a strong AI data centre power demand trade idea?

Constellation Energy Corporation, ticker CEG, has become one of the most closely watched stocks linked to the artificial intelligence power demand theme.

The logic is simple. AI needs data centres. Data centres need vast amounts of reliable electricity. Reliable, clean, around-the-clock electricity is becoming harder to secure. Constellation owns one of the most important nuclear power fleets in the United States.

That makes CEG more than a standard utility or power generation stock. It sits at the centre of several powerful market themes: artificial intelligence, data centre growth, nuclear power, grid reliability, clean energy policy and tightening US electricity markets.

The trade idea is interesting, but it is not risk-free. The long-term fundamentals support the AI power demand thesis. The company has already signed important long-term power agreements. Sentiment has cooled from the previous AI nuclear excitement. However, the technical chart remains weak, the valuation is not obviously cheap, and the market now wants proof rather than promises.

The key question is whether Constellation Energy is genuinely positioned to benefit from AI data centre power demand, or whether too much of the opportunity has already been priced into the stock.

Why Constellation Energy is being linked to AI power demand

AI is changing the electricity profile of the data centre industry.

Traditional cloud computing already required large amounts of power. AI workloads are even more demanding. They rely on high-performance chips, dense server racks, advanced cooling systems and continuous processing capacity. That means the next generation of data centres may consume far more electricity than older facilities.

This matters because data centre operators cannot rely only on intermittent energy sources. AI infrastructure needs power that is reliable, scalable and available when required. That creates demand for firm electricity supply, especially from sources that can operate around the clock.

Nuclear power fits that requirement well. It offers large-scale baseload generation with low direct carbon emissions. It is also difficult to replace quickly. New nuclear plants take years to approve and build. Existing nuclear assets therefore have scarcity value.

That is the core reason Constellation is being linked to AI data centre power demand. The company owns critical nuclear generation at a time when large technology companies are searching for reliable clean energy.

The thesis is not just that “AI needs power”. The stronger version is that AI needs dependable power, and dependable clean power is becoming strategically valuable.

Company overview

Constellation Energy is the largest nuclear operator in the United States and one of the most important competitive power producers in North America.

The company generates electricity through nuclear, natural gas, geothermal, hydro, wind and solar assets. Its profile expanded further after the Calpine acquisition, which increased its exposure to dispatchable natural gas generation and key US power markets.

Constellation also serves large commercial and industrial customers. This matters because the AI power demand opportunity is likely to be driven by major enterprise buyers, hyperscalers and data centre operators looking to secure long-term electricity supply.

The company’s nuclear fleet is central to the investment case. Nuclear assets are valuable because they provide large-scale, reliable output. They are also politically and economically difficult to replace. That gives Constellation a stronger strategic position than many conventional utilities or renewable-only producers.

Unlike a fully regulated utility, Constellation has meaningful exposure to competitive power markets. This gives the stock more upside if power prices, capacity values and long-term contracts improve. It also creates more earnings volatility if market conditions weaken.

That is important for traders. CEG is not just a defensive utility stock. It is a power market stock with a powerful thematic overlay.

Fundamental analysis

Constellation’s fundamentals are strong enough to support the AI power thesis, but they also require careful analysis.

The company has scale, cash generation, a valuable nuclear fleet and exposure to tightening electricity markets. Its reported 2025 revenue was around $25.5 billion, with operating income of around $3.1 billion. Operating cash flow was also strong, giving the company financial capacity to invest, return capital and manage long-term projects.

The Calpine acquisition changed the shape of the business. It added gas-fired generation, geothermal assets, more market exposure and stronger positioning in regions such as Texas. This could be valuable because data centre growth does not only need clean power. It also needs dispatchable power that can be delivered reliably and quickly.

The first quarter of 2026 showed the impact of Calpine. Revenue increased materially, and net income improved sharply compared with the same period in the prior year. This suggests the acquisition has already started to affect the financial profile of the business.

However, Calpine also brings more complexity. The balance sheet is heavier, debt has increased, and integration now becomes an important part of the investment case. Higher debt does not automatically make the business weak, but it means free cash flow, interest costs and capital discipline matter more.

Management has guided to strong medium-term earnings growth. That is encouraging. The market will now want to see that growth convert into durable cash flow, not just headline earnings.

Shareholder returns also support the story. Constellation has used buybacks and dividends as part of its capital return framework. That helps the equity case, especially if earnings growth remains strong.

The main fundamental strength is clear: Constellation owns scarce assets in a market where demand is rising.

The main fundamental concern is also clear: the market already understands that story, and the company must keep proving that the growth opportunity can translate into real earnings and cash flow.

Confirmed AI and data centre catalysts

The strongest part of the Constellation thesis is that it already has real commercial proof points.

The Microsoft agreement is the most important example. Constellation signed a 20-year power purchase agreement with Microsoft linked to restarting the Crane Clean Energy Center, formerly Three Mile Island Unit 1. This agreement is designed to support Microsoft’s clean energy needs in the PJM power market.

This is significant because it connects nuclear restart economics directly to data centre power demand. It shows that major technology companies are willing to use long-term contracts to secure clean, reliable electricity.

The Meta agreement adds further support. Constellation signed a 20-year nuclear energy deal with Meta linked to the Clinton Clean Energy Center in Illinois. This supports the continued operation of the plant and gives Meta access to long-term clean nuclear energy.

The Walmart agreement also matters, even though it is not purely an AI data centre catalyst. Walmart signed a 15-year nuclear power agreement with Constellation to supply a high-tech distribution facility in Illinois. This shows that demand for nuclear power is not limited to hyperscalers. Large industrial and commercial customers are also interested in long-term clean power.

Calpine brings another angle. Its Texas power arrangements with CyrusOne show direct exposure to data centre-related demand in ERCOT. This is important because Texas is one of the key markets for large-load growth.

These agreements make the thesis stronger because they prove there is real demand for the type of power Constellation can provide.

The next question is whether the company can keep signing similar agreements at attractive economics. One or two major contracts support the story. A wider pipeline of contracts would strengthen it materially.

Nuclear and power market context

The wider US power market supports the Constellation story.

For many years, US electricity demand was relatively stable. That is changing. Data centres, electrification, reshoring, industrial load growth and grid reliability needs are creating a more demanding power environment.

AI data centres are one of the most visible drivers. They need large amounts of power, and they often need it in specific locations where grid capacity is already tight. This creates pressure on power markets, transmission networks and interconnection queues.

PJM is especially important because it includes major data centre regions and has already faced reliability concerns. Tight capacity markets in PJM could support the value of reliable generation, including nuclear power.

ERCOT is also highly relevant. Texas continues to attract large-load demand, and Calpine gives Constellation stronger exposure to that market. Gas-fired generation may become strategically important because it can help meet demand faster than many other sources.

MISO matters as well, particularly because Constellation has important Illinois nuclear assets. If Midwest load growth continues, those assets may become more valuable.

Policy is broadly supportive of nuclear power. Governments increasingly recognise that nuclear energy can help with grid reliability, energy security and decarbonisation. Nuclear production tax credits and plant life extensions may provide additional support.

However, policy also creates risk. Rules around co-located data centres, grid upgrade costs, interconnection rights and capacity market treatment could affect the economics of future deals.

The macro power backdrop is favourable, but the details matter. Constellation benefits most if regulators allow nuclear and dispatchable generation to capture premium value from rising demand.

Peer comparison

Constellation is one of the clearest listed ways to express the AI power demand theme, but it is not alone.

Vistra is the closest peer. It also has merchant power exposure, nuclear assets and gas-fired generation. For investors looking at competitive power producers, Vistra is an important comparison.

NRG Energy has retail and generation exposure, but it is less nuclear-driven. It can benefit from power market strength, although it is not as pure a nuclear scarcity play.

NextEra Energy offers scale, renewables and regulated utility exposure. It is a high-quality power company, but its AI data centre exposure is less direct.

Duke Energy and Dominion Energy offer more regulated exposure. Dominion is particularly relevant because of its Virginia footprint, where data centre demand is highly important. However, the regulated utility model limits upside compared with a merchant power producer.

Public Service Enterprise Group has nuclear and regulated utility exposure, but it does not offer the same pure AI power narrative as Constellation.

Constellation deserves a premium if the market believes existing nuclear and dispatchable power assets will become increasingly scarce. It also deserves a premium if long-term power contracts can create better earnings visibility.

The risk is that premium assets often come with premium expectations. CEG is not an undiscovered stock. The market already recognises its strategic importance.

Sentiment analysis

Sentiment around Constellation has changed.

At the peak of the AI nuclear story, the stock was treated almost like an AI infrastructure beneficiary rather than a traditional power company. That helped drive a major re-rating.

That excitement has cooled. The stock has fallen heavily from its previous highs, and the technical chart now shows a clear loss of momentum. This does not destroy the long-term thesis, but it does show that sentiment is no longer euphoric.

That may be healthier for the medium-term setup. When a stock becomes too crowded, even good news can struggle to push it higher. A sentiment reset can create a better balance between price, expectations and fundamentals.

The market now appears more selective. Investors want evidence of new contracts, stronger earnings visibility and regulatory clarity. The AI power demand story alone is no longer enough.

Analyst sentiment remains broadly constructive, but less aggressively bullish than during the strongest part of the rally. Institutional interest remains high, which supports liquidity and attention, but it also means the stock can move sharply when positioning shifts.

Public sentiment is split. The bullish side sees Constellation as a rare owner of strategic nuclear assets at the start of a multi-year power demand cycle. The bearish side argues that valuation, debt, regulation and execution risks are still significant.

The current sentiment backdrop is cautious rather than euphoric. That is not bearish by itself, but it means the market wants more proof.

Technical analysis

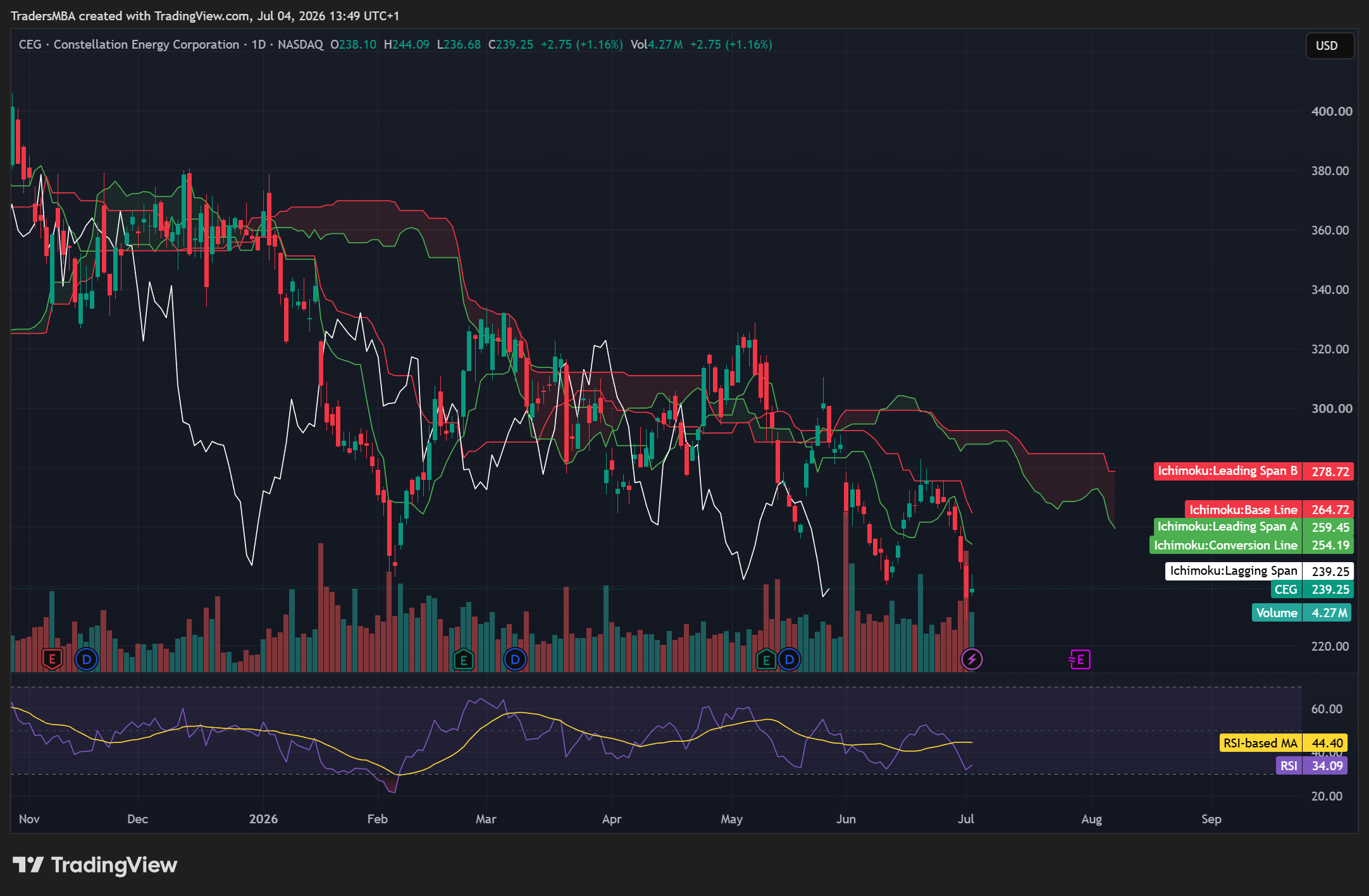

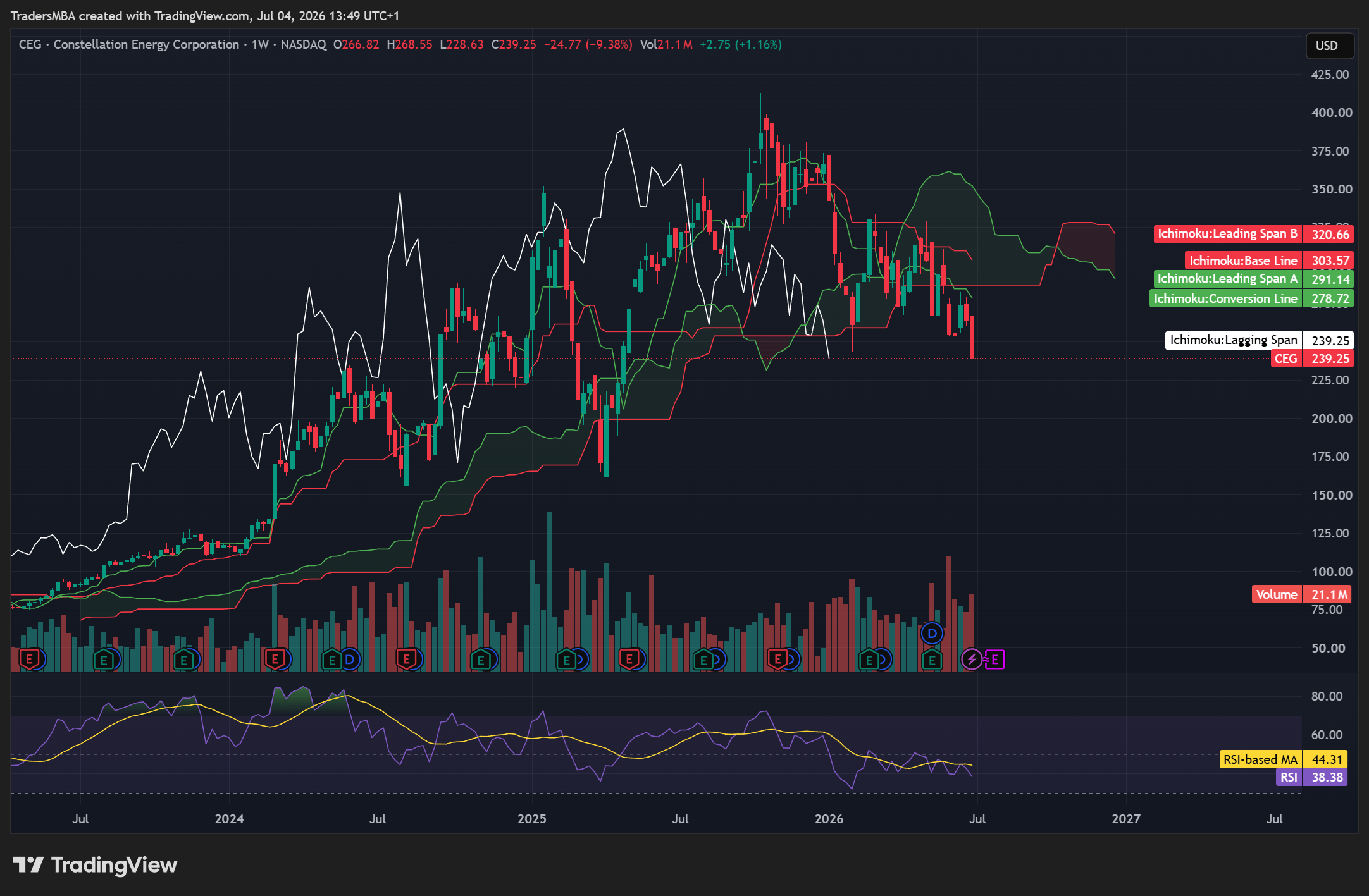

The attached daily and weekly TradingView charts show a weak technical setup.

CEG is trading around $239.25. On both the daily and weekly charts, price is below key Ichimoku levels. That is important because the Ichimoku structure has shifted from support to overhead resistance.

On the daily chart, price is below the Tenkan, Kijun and cloud. The visible daily Ichimoku levels show the Conversion Line around $254, Leading Span A near $259, the Base Line around $265 and Leading Span B near $279.

That structure is bearish. It means the short-term trend has broken down, and previous support has become resistance.

Daily RSI is around 34, below its RSI moving average near 44. Momentum is weak, although the stock is approaching an area where short-term bounces can occur.

The weekly chart is more important, and it also looks weak. The stock has printed a large bearish weekly candle. Price is below key weekly Ichimoku levels, including the Conversion Line near $279 and the Base Line above $303.

Weekly RSI is around 38 and remains below its moving average. That confirms the weakness is not just a short-term pullback.

Volume is also concerning. Recent selling has occurred on elevated volume, which suggests meaningful participation behind the decline.

The key support zone is around $236 to $228. A clean break below $228 would increase downside risk towards $220, then possibly $205 to $200.

The first important resistance zone sits around $254 to $265. Above that, $278 to $280 becomes important. A stronger recovery would need price to move back above the $291 to $305 weekly resistance area.

The technical conclusion is clear. The long-term AI power thesis may be attractive, but the chart does not yet confirm a fresh bullish setup.

Below $254 to $265, CEG remains technically bearish to neutral-bearish. Above $278 to $280, the technical picture would start to improve. Above $291 to $305, a stronger bullish recovery would become more credible.

Bull case

The bull case is built on scarcity.

Constellation owns assets the market cannot easily replace. Nuclear plants are difficult to build, difficult to approve and slow to bring online. Existing nuclear assets with strong operating performance therefore become more valuable as AI data centres compete for reliable clean electricity.

More hyperscaler agreements would strengthen this case. If Constellation signs further long-term PPAs with major technology companies, the market would have more evidence that the Microsoft and Meta agreements are part of a wider trend.

The Crane Clean Energy Center restart is another major catalyst. Progress on regulatory approval, refurbishment, staffing and timing could improve sentiment.

Calpine could also become more valuable than expected. Its gas-fired fleet gives Constellation dispatchable power in markets where data centre growth is strong. In some regions, speed to power may matter as much as clean-energy branding.

If PJM, ERCOT and MISO remain tight, Constellation could benefit from stronger power prices, higher capacity values and more long-term contracting demand.

In the bull case, CEG becomes a core AI infrastructure power stock. The market rewards it for nuclear scarcity, long-term contracts, stronger earnings visibility and strategic energy importance.

Bear case

The bear case is not that AI power demand is fake. It is that the stock may struggle even if the theme is real.

The first risk is valuation. CEG has already been recognised as an AI-adjacent power stock. Even after the correction, investors are not buying an ignored utility at a distressed valuation.

The second risk is timing. New power agreements can take time. Regulatory approvals can be slow. Large-load rules can change. Crane restart milestones may face delays, cost increases or operational challenges.

The third risk is the balance sheet. Calpine improves scale and market reach, but it also increases debt and complexity. If integration takes longer than expected or interest costs remain high, free cash flow could come under pressure.

The fourth risk is market structure. Merchant power exposure creates upside in tight markets, but it also creates earnings volatility. If power prices or capacity prices weaken, expectations could fall.

The fifth risk is technical. The chart remains weak. If CEG breaks below the $228 support area with strong volume, the stock could test lower levels before buyers return.

In the bear case, Constellation remains strategically important, but the stock stays under pressure because the market refuses to pay for long-term optionality without fresh evidence.

Base case

The base case is balanced.

Constellation is genuinely exposed to AI data centre power demand. The thesis is supported by real contracts, real power market tightness and real nuclear scarcity.

However, the next stage of upside needs more proof. The market now wants additional long-term contracts, clearer regulatory treatment, stronger cash flow visibility and successful Calpine integration.

That makes CEG more attractive as a medium- to long-term thematic opportunity than as a short-term momentum trade.

For now, it is a strong theme with a weak chart.

Key catalysts to watch

The most important catalyst would be another major hyperscaler power purchase agreement. A new Microsoft-style or Meta-style deal would reinforce the idea that Constellation can monetise its nuclear fleet at premium economics.

Crane Clean Energy Center milestones are also critical. Any progress on licensing, refurbishment, interconnection or restart timing could affect sentiment.

PJM capacity market results matter because PJM is central to the AI power demand debate. Strong capacity pricing would support the value of reliable generation.

Regulatory clarity around co-located load and large data centre demand is another key catalyst. The market needs to understand how generators, customers and grid operators will share costs and benefits.

ERCOT developments also matter. Texas is one of the most important large-load markets, and Calpine gives Constellation greater exposure there.

Other catalysts include MISO demand updates, Calpine integration progress, earnings guidance, analyst upgrades or downgrades, nuclear policy developments, power price trends and further licence extension activity.

Key risks

The biggest risks are valuation, execution and regulation.

CEG is not a simple low-risk utility stock. It has merchant power exposure, nuclear operating risk, major project execution risk, Calpine integration risk and sensitivity to energy and capacity prices.

There is also narrative risk. If investors decide the AI power theme is crowded, the stock could remain under pressure even if the long-term fundamentals are sound.

Crane restart risk should not be ignored. Restarting a nuclear asset requires capital, regulatory approval, technical execution and operational discipline.

Calpine integration is another important factor. The acquisition gives Constellation more scale and dispatchable generation, but it also adds debt and complexity.

Competition is also relevant. Renewables, batteries, gas generation, demand response and other power providers will all compete for AI-related load. Nuclear has strong advantages, but it is not the only solution.

Finally, the technical chart remains a risk. A fundamentally attractive stock can still fall further when momentum remains weak.

Trade idea scorecard

Category | Score / 10 | View |

Fundamental strength | 8 | Strong asset base, scale and earnings growth potential |

AI power demand exposure | 8 | Real contracts and clear exposure to data centre demand |

Nuclear scarcity value | 9 | Existing nuclear fleet is difficult to replicate |

Earnings quality | 7 | Strong potential, but merchant exposure adds volatility |

Balance sheet quality | 6 | Solid overall, but debt is higher after Calpine |

Valuation attractiveness | 6 | Cheaper than the peak, but not obviously cheap |

Sentiment support | 6 | No longer euphoric, but still cautious |

Technical setup | 4 | Daily and weekly charts remain weak |

Catalyst strength | 8 | New PPAs, Crane progress and power market tightness could matter |

Risk/reward profile | 7 | Attractive medium-term theme, weaker short-term timing |

Overall trade quality | 7 | Strong thematic stock, but not a clean bullish setup yet |

Final conclusion

Constellation Energy is one of the more credible public market beneficiaries of AI data centre power demand.

The reason is straightforward. AI data centres need reliable electricity, and Constellation owns scarce reliable electricity assets. Its nuclear fleet, long-term contracting ability, Calpine acquisition and exposure to tightening US power markets make it a serious player in the AI infrastructure power cycle.

This is not a purely narrative-driven trade idea. The Microsoft, Meta, Walmart and CyrusOne-linked agreements show real demand for long-term clean and dispatchable power. The broader electricity demand backdrop also supports the thesis.

However, CEG is not a clean short-term bullish technical trade today.

The chart is weak. Price is below key daily and weekly Ichimoku levels. Momentum remains bearish. Recent selling has occurred on elevated volume. Until the stock reclaims important resistance levels, the technical setup argues for caution.

The best interpretation is that Constellation is a high-quality thematic stock with a damaged chart.

For long-term thematic analysis, CEG deserves close attention as one of the clearest AI power demand names in the market. For short-term traders, the setup still needs confirmation. The stock needs stabilisation, stronger momentum and ideally a fresh catalyst before the chart fully supports the fundamental story.

The thesis is fundamentally supported, but the market now needs proof. More AI-linked power agreements, clearer regulatory treatment, better free cash flow visibility and progress at Crane would strengthen the case. A failure to secure new contracts, delays at Crane, weaker power markets or further technical breakdown would weaken it.

Overall, Constellation Energy looks like a strong medium- to long-term AI data centre power demand candidate, but not a clean short-term momentum trade at this stage.

Author

Sachin Kotecha

International Trading Institute (ITI)

Sachin Kotecha is a multi-asset trader, Professor at the International Trading Institute, and creator of institutional trading frameworks, macroeconomic intelligence platforms, and professional trading education programmes.