AUD/USD slips as strong US PMI data offsets fiscal jitters

- AUD/USD slips near 0.6415 as upbeat US data supports the Greenback.

- Jobless claims and PMI beat expectations, reinforcing a resilient US economy.

- Trump’s tax bill revives fiscal concerns, capping broader USD gains despite strong data.

The Australian Dollar (AUD) came under renewed pressure on Thursday as the US Dollar (USD) found its footing, with risk appetite fading and broader markets tilting defensively. A firm bounce in the US Dollar Index (DXY) weighed on the AUD, pushing AUD/USD down to 0.6415, a key support level that has acted as a floor in recent sessions. At the time of writing, the pair is trading around 0.6418, hovering just above intraday lows as sellers test the resolve of near-term support.

The US Dollar is supported by strong data, but longer-term risks loom

The Aussie’s pullback reflects diverging policy trajectories and economic signals. With no significant Australian data released Thursday, sentiment remains shaped by the Reserve Bank of Australia’s (RBA) recent 25 basis point rate cut, which lowered the cash rate to 3.85%. Governor Michele Bullock has maintained a cautious tone, citing slowing inflation and global trade uncertainty.

In contrast, the US Dollar found support after a string of upbeat data releases. Initial Jobless Claims for the week ending May 18 came in at 227,000, below the 230,000 consensus, reinforcing a still-resilient labor market. Meanwhile, both the S&P Global US Manufacturing PMI (May, Preliminary) and Services PMI (May, Preliminary) printed at 52.3, comfortably above the 50-mark that separates contraction from expansion. The data surprised to the upside, indicating a pickup in both factory and service sector activity.

However, sentiment around the Greenback remains mixed due to broader fiscal concerns. Investors are still digesting President Donald Trump’s “One Big Beautiful Bill”, which passed the House earlier this week. The bill proposes extending the 2017 tax cuts while reducing spending on key welfare programs. Though some see near-term stimulus potential, the legislation is expected to add over $3.8 trillion to the federal deficit in the coming decade. This has intensified concerns around US debt sustainability and credit quality, especially following recent rating downgrades. These structural concerns are limiting the Dollar’s upside, even in the face of positive near-term data.

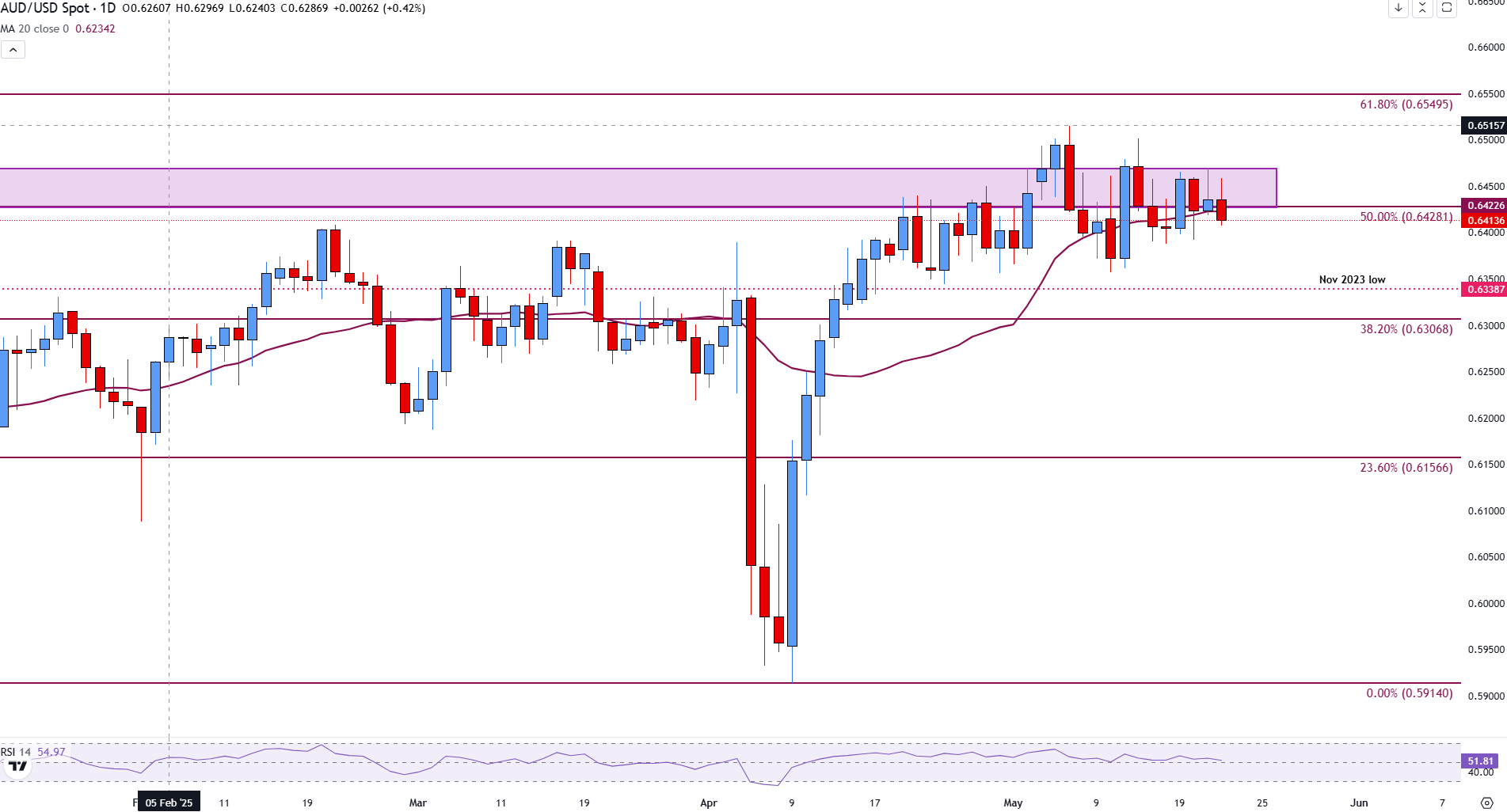

AUD/USD stalls under resistance, eyes a breakdown below 0.6415

Technically, AUD/USD is clinging to a fragile support zone near 0.6415, with recent price action showing a clear lack of conviction from bulls.

The pair has been unable to break convincingly above the 0.6420–0.6450 range, which aligns with both the 20-day Simple Moving Average (SMA) and the mid-point of the September to April decline near 0.6428.

If sellers manage to press below 0.6415, it could open the door toward the November low at 0.6338, and potentially the 0.6307 level, which marks the 38.2% Fib retracement of the October–April rally.

The Relative Strength Index (RSI) is hovering around 51.77, slightly above the neutral level of 50.

AUD/USD daily chart

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

Author

Tammy Da Costa, CFTe®

FXStreet

Tammy is an economist and market analyst with a deep passion for financial markets, particularly commodities and geopolitics.