WTI returns to logistics pricing as markets reassess demand

Key takeaways

WTI enters the second half of the week after one of the sharpest geopolitical repricing events of the year, with crude losing more than 10% over the past five sessions as immediate fears surrounding the Strait of Hormuz eased.

The market is shifting away from disruption scenarios and back toward logistics, physical flows and demand expectations as the primary pricing mechanisms.

Shipping indicators continue showing elevated stress despite the collapse in crude's geopolitical premium, highlighting a divergence between oil pricing and logistics conditions.

The current structure suggests oil is entering a new phase where access, routing and demand assumptions may become more important than headline-driven geopolitical risk.

The geopolitical premium has largely disappeared

Oil markets have undergone a remarkable transformation in less than a week.

Only days ago, traders were focused on the possibility of severe disruption across one of the world's most important energy corridors. The Strait of Hormuz dominated discussions across commodities, shipping and energy markets.

Today the conversation looks very different.

WTI has retreated sharply, Brent has moved back toward the mid-70s, and markets are increasingly behaving as though the most severe disruption scenarios have become less likely.

That does not mean geopolitical risks have vanished.

It means that markets have already repriced a large portion of those risks.

The focus is shifting elsewhere.

As geopolitical premiums decline, investors are once again evaluating the physical foundations of the oil market.

Demand expectations.

Shipping conditions.

Refining activity.

Transportation capacity.

Inventory behavior.

Those factors increasingly determine price formation once the initial shock has passed.

Logistics is becoming the dominant transmission layer again

WTI performs best analytically when viewed as a logistics system rather than simply an energy commodity.

The latest market behavior reinforces that perspective.

Several shipping indicators continue showing elevated stress conditions even as oil prices move lower. Shipping intelligence systems remain in an EXTREME STRESS regime, while tanker activity, fleet developments and routing adjustments continue attracting attention across maritime markets.

That divergence matters.

Oil prices are no longer pricing a worst-case disruption scenario.

Shipping markets, however, continue evaluating operational risk, alternative routing requirements and transportation efficiency.

The difference between those two realities creates an important analytical framework.

Physical energy systems do not immediately return to normal conditions simply because prices fall.

Flows must still move.

Cargoes must still be delivered.

Routing decisions must still be optimized.

Insurance, freight and access conditions continue influencing operational behavior across the broader energy chain.

This is why logistics often becomes the dominant transmission mechanism after geopolitical shocks begin to fade.

Demand expectations are returning to the center of the discussion

As the geopolitical layer loses influence, demand becomes more visible.

This transition is occurring at a time when markets are also evaluating the broader macroeconomic environment.

Tomorrow's US Core PCE release and final GDP figures represent important inputs for oil traders.

The reason is straightforward.

Growth expectations influence transportation demand.

Transportation demand influences fuel consumption.

Fuel consumption influences crude demand assumptions.

That transmission chain becomes increasingly important once geopolitical pricing loses momentum.

Markets are therefore entering a phase where macroeconomic data may carry more influence than geopolitical headlines.

The focus is shifting from disruption probability toward consumption sustainability.

That change often produces a very different market dynamic.

Price becomes less sensitive to isolated headlines and more sensitive to evidence regarding actual economic activity.

Tankers and freight continue sending important signals

Shipping data continues offering valuable insight into the health of the physical system.

Several crude tanker operators have recently outperformed the broader energy complex, while freight-related indicators remain constructive despite weakness in crude itself.

Dry bulk proxies have also remained relatively resilient, suggesting that transportation activity continues functioning despite elevated volatility.

Meanwhile, shipping intelligence continues highlighting tanker orders, fleet developments and routing adjustments across global energy markets.

These developments reinforce an important point.

The market is no longer asking whether oil flows will stop.

The market is asking how efficiently those flows will continue moving.

That distinction is subtle.

It is also critical.

Price formation increasingly depends on access conditions and transportation efficiency rather than outright disruption fears.

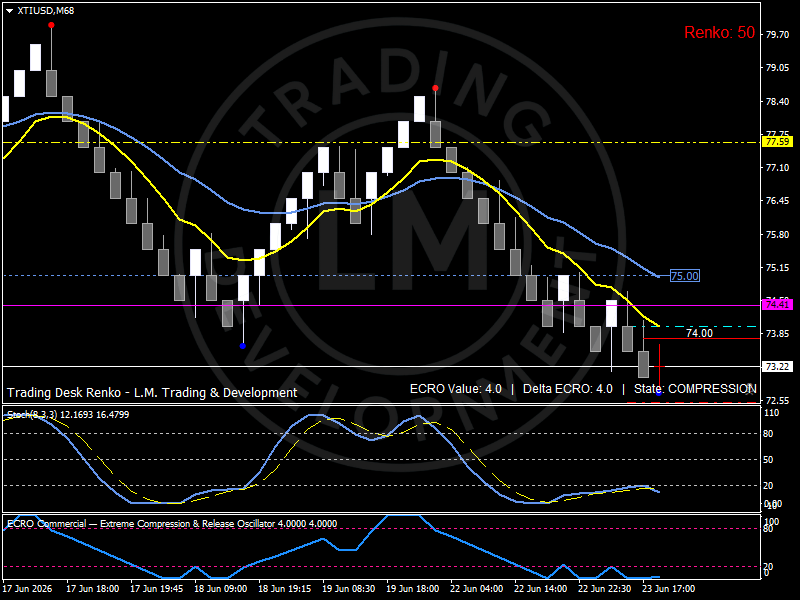

Technical structure: WTI enters a compression regime

The technical structure reflects a market transitioning from rapid repricing toward consolidation.

The recent decline pushed WTI sharply lower from the upper-70s region into the low-70s, removing much of the geopolitical premium accumulated during the previous rally.

The Renko framework now shows a market operating inside a clear compression environment.

The ECRO indicator has fallen to extremely low levels near 4, while the system remains in a COMPRESSION state. Such conditions typically reflect reduced directional conviction following a major repricing event.

Momentum remains subdued.

Participation remains limited.

Price continues trading below both short-term moving-average layers, reinforcing the idea that sellers maintain control of the broader structure.

At the same time, downside momentum has slowed considerably.

Resistance is concentrated near the 74.4 participation corridor, while the broader recovery framework extends toward 75.0.

Support remains anchored near 73.2, with the current structure suggesting balance rather than acceleration.

The overall configuration resembles a market searching for a new catalyst after exhausting the previous narrative.

Bird's eye view

WTI currently operates inside a logistics-driven market where demand expectations, transportation efficiency and physical flows are gradually replacing geopolitical fears as the dominant pricing drivers.

The sharp decline of the past week has largely removed the immediate disruption premium from crude markets, while shipping indicators continue reflecting elevated operational stress across global transportation networks.

Structurally, the market remains below the 74.4 resistance corridor, while 73.2 continues acting as the primary support level inside a broader compression regime.

The dominant variables remain freight conditions, tanker activity, routing efficiency and demand expectations linked to upcoming US macroeconomic data.

Outlook

WTI enters the remainder of the week facing a very different environment from the one that dominated headlines only days ago.

The geopolitical layer has not disappeared, but its influence on price formation has diminished substantially.

Markets are returning to the fundamentals of the physical oil system.

That means demand expectations, transportation efficiency, routing conditions and freight dynamics are likely to play a larger role in determining the next directional phase.

The interaction between logistics conditions and macroeconomic demand signals will ultimately determine whether oil stabilizes within the current range or begins developing a new trend.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.