WTI and Gold spike on US missile attack at Baghdad airport

With Japan still on holiday and no major economic data scheduled in Asia, it looked like we were on track for another quiet session. President Trump had other plans.

Reports of a missile attack at a Baghdad airport hit the screens, with reports that seven pro-Iranian security officials had been killed. An Iraqi militia spokesman confirmed that Iranian Major-General Qassem Soleimani and Iraqi militia commander Abu Mahdi al-Muhandis and then claimed that “Americans and Israelis” were behind the attacks.

US officials and the Pentagon confirmed the US was responsible for the attack, whilst reports surfaced that US Navy Seals had also captured pro-Iran militia commanders in Iraq. And, if that were not enough confirmation, Trump tweeted a picture of the American flag.

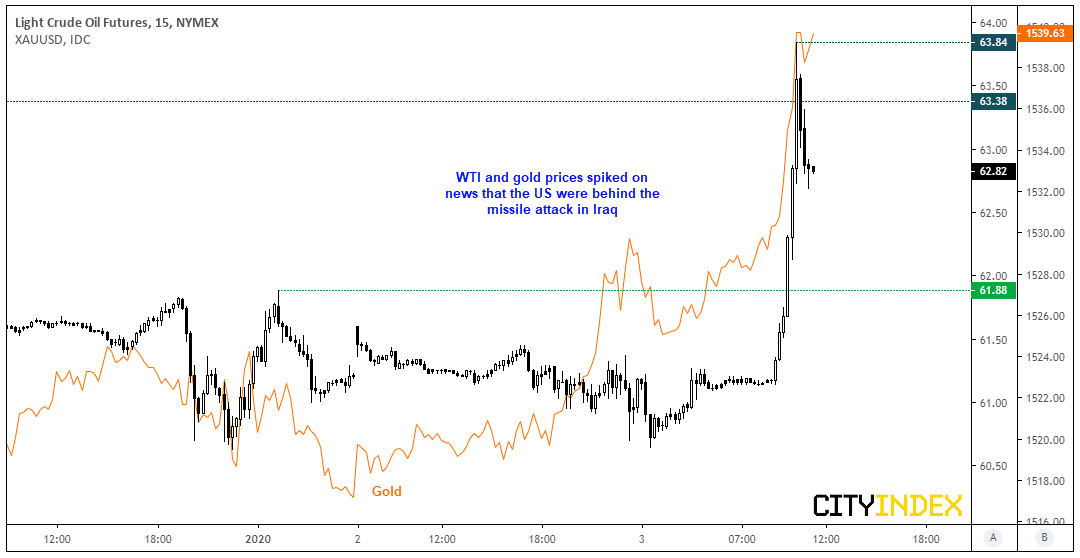

As you’d expect, oil prices spiked on supply concerns and at its high had rallied over 4%. Gold also followed suit and hit its highest level since September.

The repercussions from today’s events are yet to be seen but, given the seniority of the leaders killed and detailed, they’re not likely to be small. One pundit was quoted saying “I’m not sure Donald Trump realises what he’s unleashed”, which could be putting it mildly. It’s around 7am in Iran at the time of writing. This leaves plenty of time for developments through the Asia session and beyond, so everyone is being kept on their toes for developments.

Today’s spike has taken WTI break out of its bullish channel and print an intraday high above $64. Yet with prices having retreated below 63.38 resistance, more information may need to come to light before to help decide which side of this key level WTI closes on. If tensions escalate and it appears there will be a squeeze on the oil supply, then we could find prices rebound back above $64 with relative ease. Yet if the response is somehow muted (unlikely at this stage) we could be looking a sharp reversal and for WTI to leave bearish hammer in its wake.

-

A break above 64 brings the 66.60 high into focus

-

A daily close <= 62 would leave a bearish hammer and signal a bull-trap, and take it back within the 50 – 64 range it was remained within since May

Author

Matt Simpson, CFTe, MSTA

CityIndex

Matt Simpson is a certified technical analyst who combines charts and fundamentals to generate trading themes.